Monetary Policy Rules

Taylor-type rules, or instrument rules, should be discarded in favor of Target Rules Among those, NGDP Level Target Rules show the most promise

It is understandable that economists would like things that bear their name to survive. Examples are “Beveridge Curve” and “Okun Law” among many others (“Nash Equilibrium”, for example).

So it´s not surprising to see John Taylor try hard to ‘enshrine’ his namesake rule, The “Taylor-Rule”, for setting interest rates by the Fed. In a recent post for Project Syndicate “The Fed´s State of Exception” Taylor writes:

Despite the recent surge of inflation in the United States, the Federal Reserve is keeping the federal funds rate in a range far below what its own monetary-policy rules would prescribe. But since history shows that this deviation cannot last indefinitely, it would be better to normalize sooner rather than later.

…Despite a sharp increase in the rate of money growth, the central bank is still engaged in a large-scale asset-purchase program (to the tune of $120 billion per month), and it has kept the federal funds rate in the range of 0.05-0.1%.

That rate is exceptionally low compared to similar periods in recent history. To understand why it is exceptional, one need look no further than the Fed’s own July 9, 2021, Monetary Policy Report, which includes long-studied policy rules that would prescribe a policy rate higher than the current actual rate. One of these is the “Taylor rule,” which holds that the Fed should set its target federal funds rate according to the gap between actual and targeted inflation.

In his 1993 paper, where he proposed the rule that later bore his name, Taylor did not seem to believe that his rule should be more than a general guideline. In fact, he took pains to point out that a simple mechanical rule could not take into account the many factors that policymakers must consider in practice.

In the years that followed, though, Taylor has taken a much more prescriptive view, essentially arguing that policy should hew closely to the Taylor rule (or a similar rule) virtually all the time, and that even relatively small deviations from the rule can have significant costs.

For example, Taylor has argued that:

The Fed decided to hold the interest rate very low during 2003-2005, thereby deviating from the rules-based policy that worked well during the Great Moderation.

You do not need policy rules to see the change: With the inflation rate around 2%, the federal funds rate was only 1% in 2003, compared with 5.5% in 1997 when the inflation rate was also about 2%. The results were not good.

In my view this policy change brought on a search for yield, excesses in the housing market, and, along with a regulatory process which broke rules for safety and soundness, was a key factor in the financial crisis and the Great Recession.

There´s not much that is “mechanical” about the Taylor Rule. It´s formulation requires knowledge of “unknowns” such as the level (or growth rate) of “potential” output and the level of the the “neutral” rate. To this last, Taylor “fixes” its value at 2%.

In 2001, Gregory Mankiw wrote “Monetary Policy during the 90s”:

This paper discusses the conduct and performance of U.S. monetary policy during the 1990s, comparing it to policy during the previous several decades.

At the end of the paper he estimates an equation for the Fed Funds rate and finds that the resulting Fed Funds rate closely tracks the actual Fed Funds rate. That result is obtained using only observable variables, the difference between the year-on-year Core PCE inflation rate and the unemployment rate and does not assume an “inflation targeting” central bank.

In what follows, therefore, I´ll make use of the “Mankiw Rule” instead of the “Taylor Rule” in my illustrations. As the first chart I put up will show, they give results that are qualitatively (if not exactly quantitatively) similar. [Even today, with the Taylor Rule (with 2% for the neutral rate) prescribing an FF rate of 6%, the Mankiw Rule puts it at 6.5%, something not terribly different].

What if the central bank, instead of an “instrument rule” adopted a “target rule”? For concreteness, let´s assume the Fed had adopted (maybe implicitly) a NGDP level target as it´s rule for monetary policy.

The charts compare and contrast the interest rate “policy rule” and the NGDP level target rule (where the “target (trend) level” is the “Great Moderation” (1987-05) trend). In this comparison, the actual setting of the Federal Funds (FF) rate is “right or wrong” depending on, not if it agrees with the setting “suggested” by the instrument rule, but if it is the rate that keeps NGDP close to the target path; and in case there is a deviation from the path, if the (re)setting drives NGDP back to the target.

During the 1987 - 1992 period analyzed in Taylor´s 1993 article, monetary policy was “quite good”, in the sense of keeping NGDP close to the “target path”. Actually, when the Fed reduced the FF rate at the time of the stock market crash, it turned monetary policy a bit too expansionary, given NGDP went a bit above trend.

The next period covers 1993 – 1997. This is the core period of the “Great Moderation”. At the end of 1992, the FF rate had been reduced to 3%, a level which was maintained throughout 1993. According to the “policy rule” this was “too low”. With respect to the “target rule”, the FF rate was “just right”.

All through those years, NGDP remained very close to the “target path”, although the FF rate at times differed significantly from the “policy rule”.

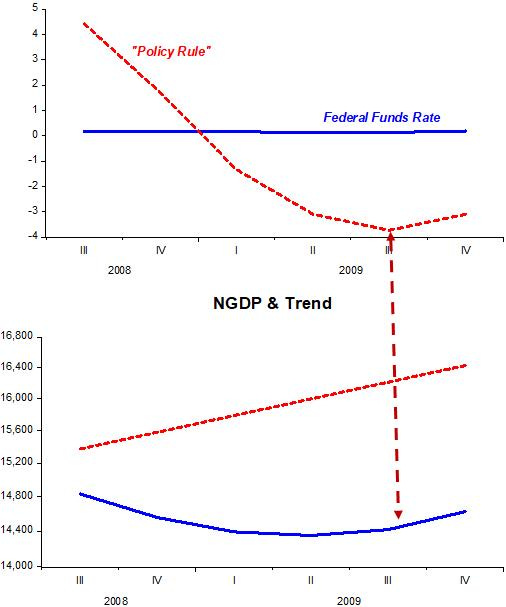

The next period, 1998 – 2003.II, is pretty damaging to the “policy rule” advocates. AS mentioned above, Taylor likes to say that the 2002 – 2005 period was one of “rates too low for too long” (having responsibility for the crash that came later).

What the chart tells us, however, is very different. The FF rate was too low in 1998 – 99. At this time, the Fed reacted to the Russia crisis (and the LTCM affair). Monetary policy loosened up at the same time that the economy was being buffeted by a positive productivity shock.

The monetary tightening that followed was a bit too strong because NGDP dropped below trend. The downward adjustment of the FF rate was correct in the sense that it stopped NGDP from falling lower, and by mid-2002 it began to recover. I wonder how much more grief the economy would have been subjected to if the “policy rule” had been followed.

The 2003.III – 2005 period is the second half of Taylor´s “too low for too long”. In the FOMC meeting of August 2003, the Fed adopted “forward guidance” (FG) (first it was “rates will remain low for a considerable period” followed by “will be patient to reduce accommodation, and finally “rates will rise at a measured pace”). The fact is that FG helped push NGDP back to trend. Maybe the “pace was too measured”, but the fact is that by the time he handed the Fed to Bernanke, NGDP was square back on trend.

If the “policy rule” had been closely adhered to, the “Great Recession” would likely have happened sooner!

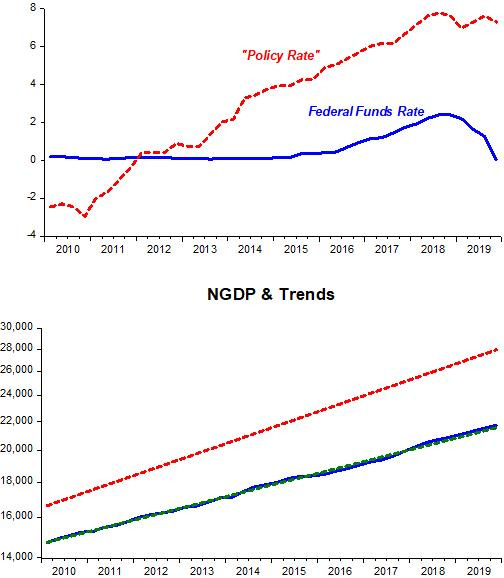

And now we come to see how the Fed botched monetary policy (likely due to Bernanke´s preferred inflation targeting monetary policy regime).

The FF rate remained at the high level it had reached at the end of the “measured pace story”. At the end of 2006, aggregate demand (NGDP) began to deviate, at first slowly, below the trend level. The FF rate remained put (notice that although too high, the “rule rate” changed direction). The FOMC was not comfortable with the “elevated” price of oil and kept hammering on the risks of inflation expectations becoming un-anchored (see the late 2007-08 FOMC transcripts).

Despite the reduction in the FF rate, monetary policy was being tightened! And the “Great Recession” was invited in! Maybe there would have been a “Second Great Depression” if the “policy rate” had been followed closely.

We notice that the “policy rule” is very “conservative”, remaining much of the time above the Federal Funds Rate. Diving into the Great Recession, however, the “policy rule” turns deeply negative! This is certainly signaling that, despite the “zero” Federal Funds Rate, monetary policy is extremely tight.

However, as soon as NGDP stops falling, the “policy rate” indicator reverses. That is suggesting that the Fed should not allow NGDP to go back to trend.

This becomes clear over the next decade, where NGDP remains far below the previous trend, but remains very stable along this lower trend level path. Quickly the “conservative” trait of the “policy rate” reasserts itself, indicating that monetary policy is “too loose”!

Writing in 2015, Taylor blames much of the disappointing recovery on the Fed’s deviations from the Taylor rule.

Regardless of what you think of the impact of QE, it was not rule-like or predictable, and my research shows that it was not effective. It did not deliver the economic growth that the Fed forecast and it did not lead to a good recovery. And yet another deviation from rules-based policy was the continuation of a near zero interest rate through the present, long after Great Moderation rules would have called for its end.

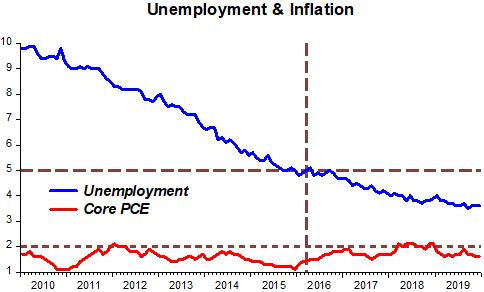

It´s hard to see where those ideas come from. With NGDP evolving smoothly along a (lower) trend level path, unemployment falls steadily and inflation remains for the most part below target. Note, however, that when unemployment breaches 5%, the Federal Funds Rate begins to rise! Phillips Curve thinking puts “fear” in monetary policy makers!

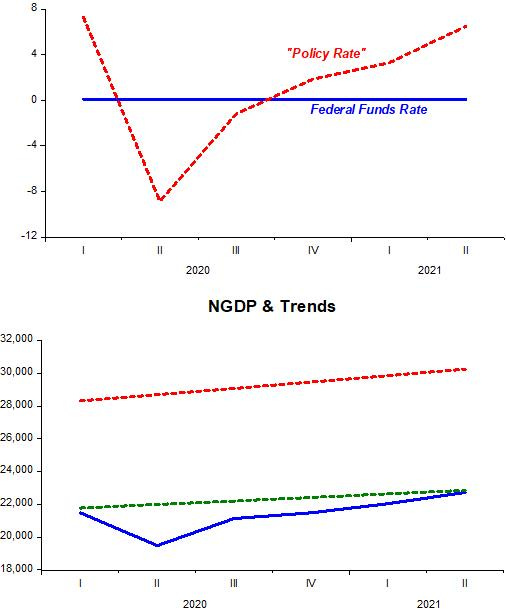

18 months into the pandemic, Taylor is again at it, calling on the Fed to raise rates that are far below those indicated by the “rule”.

The conclusion is clear. The “instrument rule” has never been satisfactory, most of the time indicating that the Fed was pursuing a “loose” monetary policy. We can only imagine the tragedy that would be the economy if the “instrument rule” had been closely followed!

Things went bad in 2008 when the Fed abandoned the de facto NGDP Level Target rule it had closely followed from 1987 until 2006.

If not the Fed Funds Rate, what will the Fed need to “calibrate” to satisfy the NGDP Level Target rule?

A: The “Thermostat”

What´s still to be “chosen” is the Level Path along which NGDP will evolve. It is clear that over the past decade the Fed has kept the economy at a “depressed” level.

PS On page 4 of his 1998 article, John Taylor makes the following consideration:

If only he had followed up on that…

Complete tripe. Interest is the price of credit, the price of money is the reciprocal of the price level.