Grading Powell with the Wrong Ruler

The Romers’ retrospective on the Powell Fed is comprehensive. Re-grade the same eight years by nominal spending and the verdicts change, in both directions.

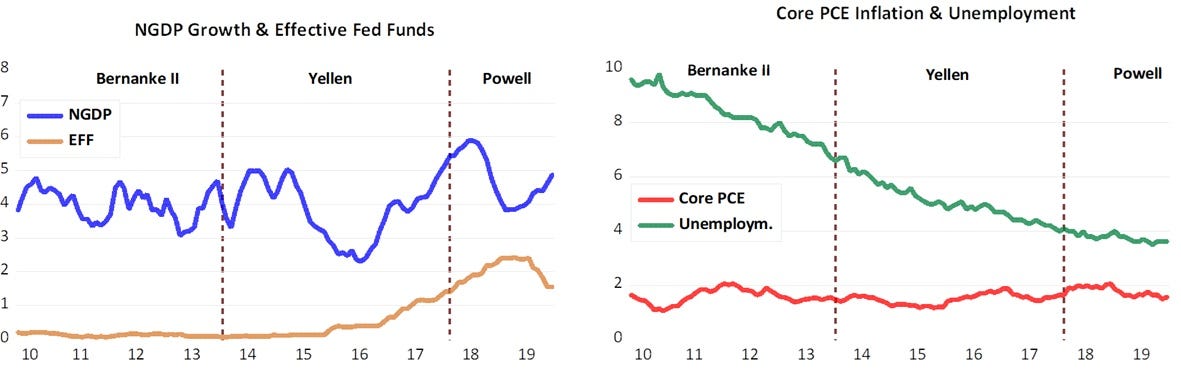

Christina and David Romer have written what will likely become the standard early reference on the Powell Fed. The narrative method is their trademark: read the FOMC Minutes in sequence, reconstruct what policymakers believed and why, then ask whether the decisions were reasonable given what was known at the time.

The chronology is meticulous. The tone is appropriate — Powell is “a hero” facing “enormous challenges with skill, integrity, and quiet determination,” and the 2021 inflation forbearance is still judged unreasonable. The six lessons at the end are sensible. On Fed independence, the paper is at its best.

And yet the entire evaluating process runs on a single gauge: the federal funds rate relative to the FOMC’s estimate of neutral, checked against forecasts of inflation and unemployment — a qualitative, forward-looking Taylor rule.

Every scatterplot in the paper has the rate gap on one axis. Every verdict of “reasonable” or “not reasonable” is a statement about where the funds rate sat relative to neutral.

Nowhere in that evaluation is there a nominal aggregate. Not money. Not total spending. In a fourty-page retrospective of monetary policy, the thing monetary policy most directly governs — the flow of nominal expenditure — never enters the apparatus that does the grading.

This is not a small omission. It is the difference between right and wrong verdicts on at least three of the six episodes.

The oldest lesson in monetary economics

Milton Friedman spent a career warning that interest rates are a misleading indicator of the stance of policy. Low rates are more often a sign that money has been tight — the economy weak, inflation low — than that policy is easy. High rates typically signal the opposite. The fallacy of reading the stance off the rate is old enough to have a name, and central banks fall into it anyway, generation after generation.

The Romers know this literature as well as anyone alive. Their own classic work helped establish that you cannot infer the stance of policy from the instrument alone — that is the whole point of their narrative method. Yet the retrospective’s formal apparatus does exactly that: it reads “tight” and “loose” off the gap between the funds rate and an unobservable, drifting, FOMC-estimated neutral rate.

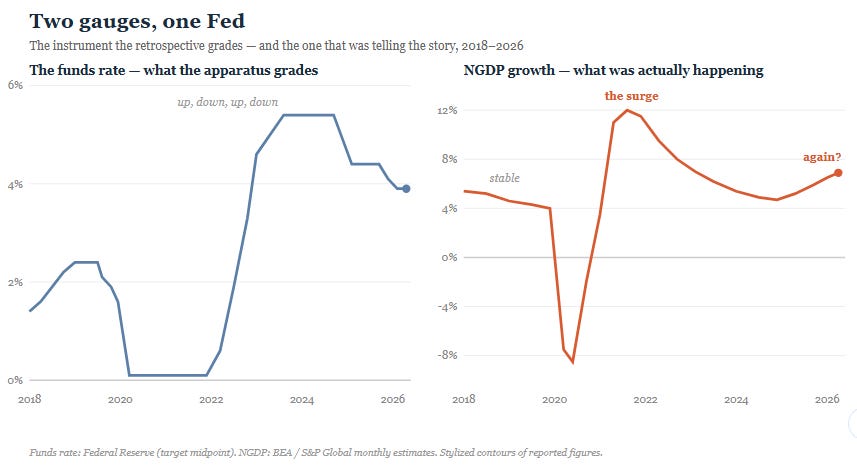

There is a better gauge, and it requires no estimate of anything unobservable: the growth of nominal GDP — total spending in dollars. When nominal spending grows on a stable path consistent with the inflation target, policy is well calibrated, whatever the rate is doing. When spending accelerates well above that path, policy is loose, whatever the rate is doing.

The rate is the steering wheel; nominal spending is the speedometer. The Romers have written a retrospective about eight years of driving that discusses only the steering wheel.

Run the same episodes past the speedometer and watch the grades move.

2018–2019: the reversal that wasn’t

The Romers are ambivalent about 2019. The Fed raised rates four times in 2018, then cut three times in 2019, and they find the case for the cuts “far from obvious” — unemployment was at historic lows, the outlook still positive. They suspect the FOMC was drifting toward fashionable theories about flat Phillips curves and the social benefits of hot labor markets.

Now look at the speedometer. From the end of the Great Recession through 2019, NGDP growth was remarkably stable — fluctuating around 4 to 5 percent, year after year, through “zero” rates, rate hikes and rate cuts alike. The funds rate went from zero to 2.5 percent and partway back down; nominal spending barely registered the trip. Inflation, meanwhile, kept undershooting 2 percent.

By the nominal ruler, there was no “reversal” in 2019 at all. The stance of policy — measured by what it was delivering — scarcely changed. The 2019 cuts kept nominal spending on the same path it had been on, with inflation still below target. Far from being the episode’s weak point, the cuts look like good stabilization: the rate moved so that spending didn’t have to.

Here the NGDP lens is more forgiving than the Romers. Hold that thought, because the lens is about to become much harsher — which is how you know it is a different instrument and not a different mood.

2021: you didn’t need a forecast

On the 2021 forbearance, the Romers’ verdict is right: not reasonable. But their indictment understates the crime, because their method needs forecasts to convict, and the forecasts were broken.

Their case runs through the Taylor rule: by late 2021, forecast inflation exceeded target and forecast unemployment sat below the natural rate, so the rule said raise rates, and the FOMC didn’t. True. But they must also concede that the Survey of Professional Forecasters (SPF) never forecast four-quarter inflation above 2.6 percent through mid-2022 — everyone’s crystal ball failed — which lets the episode read partly as forecast bad luck.

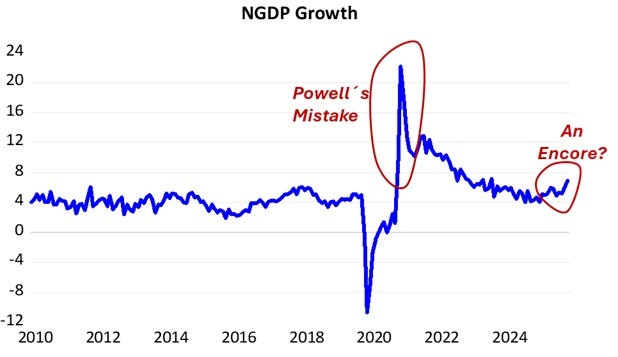

The nominal ruler requires no crystal ball. By mid-2021, actual, already-published nominal spending was growing at double-digit rates — the fastest sustained pace in decades — and the level of NGDP was racing back to, then through, its pre-pandemic trend. You did not need to predict anything. You needed only to read the speedometer that quarter and notice the needle was pinned.

That is the deepest problem with rate-and-forecast evaluation: it makes the 2021 failure look like a forecasting error, when it was a monitoring error. The data that condemned the stance were in hand, in real time, every quarter (even every month). The FOMC — and, with respect, the retrospective grading it — was simply looking at a different dial.

The steep part of the curve

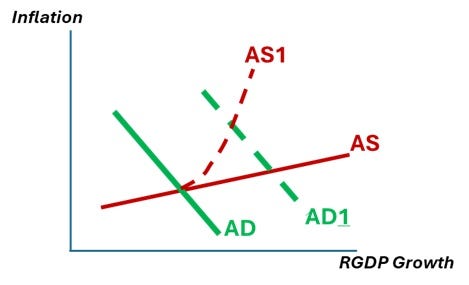

There is a second reason 2021–22 was worse than the Taylor-rule reading suggests, and it comes from the supply side. I wrote recently about new work formalizing what that period taught: when supply chains break and capacity binds, the aggregate supply curve doesn’t just shift — it steepens. It becomes convex. Each increment of nominal spending buys less output and more inflation than the last.

That convexity cuts twice against the 2021 stance. First, it means the double-digit nominal spending growth was landing on the steep portion of the curve, converting into prices nearly one-for-one — the worst possible moment for an overshoot.

Second — and this is the part the new research makes precise — a steep supply curve improves the trade-off facing a central bank that leans against the wind: restraint gives up little output and buys a lot of disinflation precisely when the curve is steep.

So in 2021 the Fed had both the strongest signal to tighten (the nominal speedometer pinned) and the cheapest opportunity to do so (the steep curve). It did neither. The Romers call this unreasonable on forecast grounds. On nominal-spending-plus-supply-curve grounds, it is something closer to the single largest unforced error in the period.

The “puzzle” that isn’t

Which brings us to the most revealing sentence in the paper. Discussing the 2022–23 disinflation — PCE inflation falling from 7 percent to under 3 with unemployment rising only a few tenths — the Romers write that “why inflation finally fell when it did is puzzling,” noting that standard models say tightening of that size shouldn’t have disinflated so much so cheaply, and that perhaps it was partly luck.

When your model calls the period’s most important outcome a puzzle, the difficulty usually lies in the model.

Through the nominal-spending lens, with the convex supply curve in hand, there is no puzzle at all. The disinflation happened because NGDP growth decelerated sharply — from double digits back toward a normal range — at the same time as supply capacity recovered and the economy slid back down off the steep portion of the curve.

Coming down a steep, convex supply curve is the mirror image of going up it: large price deceleration, small output cost. The “immaculate disinflation” is exactly what that geometry predicts. No luck required, and no mystery — just the right two variables, which are the two the retrospective’s apparatus does not contain.

This matters beyond scorekeeping. A framework that treats the disinflation as a fortunate accident cannot tell future policymakers how to repeat it. A framework in which it is the predictable consequence of restoring nominal spending to path while supply recovers can.

2024–2026: the gauge is flashing again

On the recent cuts, the Romers are uneasy in the right direction but, again, on the wrong instrument. Their complaint is about pledges and reputations: the Fed vowed to hold until inflation’s return to 2 percent was compelling, inflation never compellingly returned, and the Fed cut anyway — five years above target, a price level up more than 20 percent.

The nominal ruler turns that unease into something sharper. Nominal spending growth has been reaccelerating since early 2025 and is now approaching 7 percent — the arithmetic of roughly 5 percent inflation at trend real growth, not 2.

Money growth has moved the same way. The speedometer is not whispering; it is flashing. By the rate-gap apparatus, the Fed has merely moved “toward neutral.” By the spending gauge, it is rerunning a milder version of 2021 in real time — easing into an acceleration.

The two rulers will not disagree forever. They never do. The question is only whether the Fed reads the right one before the price data force the issue.

A seventh lesson

The Romers’ first and best lesson is that policymakers need “a realistic model of how the economy operates.” Amen — and the lesson needs radicalizing, because a realistic model includes a reliable indicator of one’s own stance.

The Powell-era record, re-read: every episode the Romers grade as sound was one where nominal spending was on a stable path; every episode they grade as questionable was one where it wasn’t; and the one outcome their framework cannot explain is fully explained by it.

So add a seventh lesson, the one the paper circles without landing on: judge the stance of monetary policy by the path of nominal spending, not by the level of the interest rate. Rates rose and fell twice in the Powell era while telling you almost nothing. Nominal GDP told you everything, in real time, at every turn — including, right now, that the lesson has not yet been learned.

in 2019 not only was the price level still below what 2% would have required, but infaltion isweld was below 2%

You are correct to callout any instrument rate metric. The correct ruler, however, is the modeled minimum inflation rate that woud have maintained full emploument of resources. (Or if you prefer, the mimimum NGDP rate).