When Supply Chains Break, the Fed Should Lean In — Not Back Off

A new NBER paper quietly dismantles the conventional wisdom on monetary policy and supply shocks — and the punchline is almost funny.

There’s a view that has dominated central banking since at least the stagflation of the 1970s: when a negative supply shock hits — an oil embargo, a pandemic, a war disrupting shipping lanes — monetary policy should tread carefully.

Tighten too hard and you compound the damage, crushing output on top of an already-contracting supply. The inflation is “cost-push,” the story goes, and fighting it with interest rates means paying an output price that isn’t worth it. Better to look through it and wait for the shock to pass.

A new working paper by Bai, Fernández-Villaverde, Li, and Zanetti — State Dependence of Monetary Policy During Global Supply Chain Disruptions (NBER Working Paper 35209, May 2026), building on their earlier study of how supply chain disruptions move output and prices — suggests this conventional wisdom, under certain circumstances, may be precisely backwards.

The geometry of a disrupted supply chain

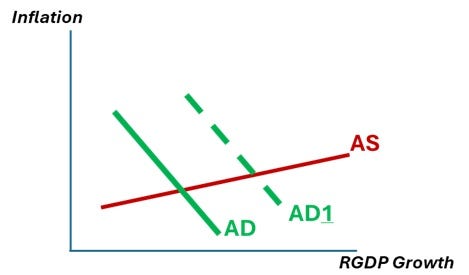

The core insight is deceptively simple. When global supply chains function normally, the aggregate supply curve is relatively flat. A shift in demand — whether from monetary or fiscal expansion — gets split between prices and output in roughly the proportions a standard macro model would predict: some price adjustment, meaningful output movement. The chart illustrates.

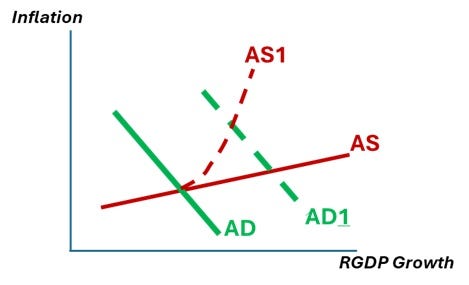

But when supply chains are severely disrupted — port congestion spiking, transportation costs surging, the mismatch between what retailers need and what producers can deliver widening — the aggregate supply curve steepens.

The mechanism runs through search frictions and rigid shipping contracts, and the paper’s framing is precise: upstream slack coexisting with downstream shortages.

When transportation costs are high and volatile, the density of viable producer-retailer matches at the margin collapses. Extending the cutoff of profitable matches requires a disproportionately large price premium but adds very little additional volume. The curve becomes steep, and locally convex.

Once you’re on the steep part of that curve, everything changes. A given shift in aggregate demand now moves prices a lot and output much less.

The empirical estimates are striking: in the authors’ threshold-VAR model, the impact decline in goods prices from a monetary contraction nearly doubles during disruptions — from roughly 0.1% to 0.2% — and grows markedly more persistent, stretching from about six months to over a year, while the output response stays muted.

Their framing is that monetary policy is more effective at taming inflation after a supply chain shock than in ordinary times.

This is, in a sense, a very old idea wearing new clothes. The authors reach for Keynes’s 1940 argument about how to pay for the war: when output is constrained — by shipping bottlenecks in our case, by wartime resource mobilization in his — the authorities can compress demand aggressively without much fear of crushing production.

The constraint that makes the situation feel dangerous is the very thing that makes demand management cheap.

Below the payall I discuss:

Why the same geometry that makes tightening cheap makes fiscal stimulus unusually dangerous — and what it says about the trillions poured into a bottlenecked economy in 2021.

The case that Larry Summers diagnosed the disease correctly and then misdiagnosed the cure — committing the same conceptual error in both directions.

Why the “immaculate disinflation” that baffled forecasters may have a clean explanation — and why I don’t think that explanation fully holds up.

The reading of the 2022 hiking cycle that widens the indictment of the Fed well beyond 2021.

How the whole argument reframes around nominal GDP — and why “lean harder into supply shocks” turns out to be the wrong way to say it.

Why I now think my own earlier defense of Jay Powell needs tempering — and the irony in how Powell reached the same verdict the hard way, without the model in hand.