Why Your Grocery Bill Feels Wrong

The Strange Math of Inflation Perception

Something odd is happening with inflation. The official numbers show it stubbornly stuck around 3%—the September 2025 reading came in at exactly 3%, up from 2.9% in August. The Federal Reserve remains cautious. Economists debate the next moves. Yet when you talk to actual people buying actual groceries, they remain furious.

This disconnect isn’t just political spin or economic illiteracy. It reveals something fundamental about how inflation actually works versus how we experience it.

Here’s the problem: inflation measures the rate of price increases, not price levels. When economists say inflation is “only 3%,” they mean prices are rising at 3% annually. But prices aren’t falling back to where they were. If eggs cost $3 in 2020, jumped to $6 in 2024, and now cost $6.18 in 2025, that’s technically just 3% inflation (from $6 to $6.18). But you’re still paying double what you paid five years ago.

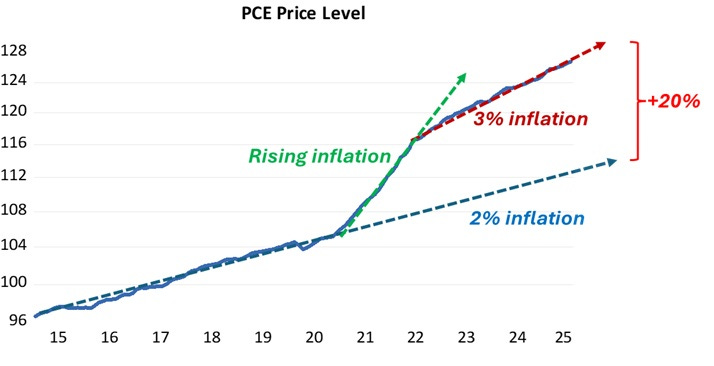

A chart helps to understand the process.

The chart below shows how the Personal Consumption Price Level evolved in the last ten years. Before the Covid-19 pandemic, prices were rising at a rate close to 2% on average, During the pandemic inflation increased (reaching 9% at the peak). From then on, inflation is rising closer to 3%.

The price level today is about 20% higher than it would be if there had been no “pandemic inflation”.

The 20% increase in the price level is an (weighted) average of all prices. Some price have risen much more (like groceries), while others have risen less and some prices have even fallen somewhat.

This matters enormously because different groups experience this mathematical reality differently. If your wages increased 20% between 2020 and 2025, you’ve roughly kept pace with overall price increases.

Many professionals, especially in tech and finance, saw exactly these gains. But if you’re a retiree on fixed income, or a worker whose wages rose only 10%, you’re genuinely poorer even though “inflation is only 3%.”

The grocery store makes this visceral. We don’t buy “the CPI basket of goods”. We buy specific items. We remember the prices of eggs, milk, bread, ground beef. These staples saw some of the sharpest increases.

Meanwhile, the items that got cheaper—like televisions and smartphones—aren’t things we buy daily or weekly. The emotional weight of a $6 carton of eggs vastly exceeds the mild satisfaction of a slightly cheaper laptop you purchase every three years.

This creates a political tinderbox. When the Biden administration pointed to declining inflation rates as economic success, voters heard: “Stop complaining about prices (that are higher).”

When Trump promised to bring prices down, he was pledging something nearly impossible without deflation (falling prices), which usually, but not always, accompanies severe recessions.

Neither message matched reality: prices went up dramatically, they’re staying elevated, and that genuinely hurts millions of people even though the rate of increase has slowed from its 2022 peak of 9%.

As the WAPO put it succintly in commenting on the Nov 4 election results:

‘It’s affordability, stupid’

Axios goes into greater detail:

The Fed now faces an uncomfortable dilemma. Inflation at 3% remains above their 2% target, yet the economy shows signs of softening. Do they keep rates high to squeeze out that last percentage point of inflation, risking recession? Or do they cut rates to support growth, accepting that 3% inflation might persist? Markets expect rate cuts, but the Fed’s hesitation reflects this genuine policy bind.

This creates the paradox we’re living through: by traditional metrics, the economy shows mixed signals. Unemployment remains relatively low, though rising slightly. Real GDP growth is positive but slowing. The stock market hit records but has become volatile.

Yet most Americans feel economically worse off because their lived experience focuses on prices, not rates of change. A person whose wages rose 15% while prices rose 20% is, mathematically, 5% poorer. Telling them “but inflation is down from 9% to 3%!” doesn’t help.

The political implications are profound. Incumbent parties get blamed for inflation regardless of cause.

Biden’s approval ratings tanked despite strong employment numbers. Trump won re-election partly by promising to fix prices, even though presidents have limited tools to do so. Voters understand their grocery bills better than economists’ charts, and they vote accordingly.

What could actually bring prices down? The options are grim:

Deflation—actually falling prices—sounds great until you remember it frequently accompanies severe recessions. When prices fall, businesses cut production and lay off workers. People delay purchases hoping for lower prices later, which reduces demand further, causing more price cuts and layoffs. It’s a doom loop. The last time the U.S. experienced sustained deflation was during the Great Depression.

Productivity increases could help. If we produce goods more efficiently, costs fall and prices can decrease without recession. But productivity gains happen gradually through technology and investment, not quickly through policy changes.

Removing tariffs would help modestly. Trump’s tariffs on Chinese goods and other imports raised prices for consumers. Eliminating them would reduce some costs, but the effect would be limited. Ironically, Trump has expanded rather than reduced tariffs in his second term, pushing prices higher.

Increasing supply in constrained sectors would help. Building more housing would reduce shelter costs. Expanding domestic energy production would lower fuel prices. Reducing regulatory barriers to agricultural production might ease food costs. But these changes take years to manifest.

The uncomfortable truth is that we’re probably stuck with elevated prices. Barring a major recession, egg prices will stay high. Ground beef will remain expensive. Rent won’t return to 2019 levels. The best realistic outcome is that wages gradually catch up, making these prices feel less painful over time. For many workers, this is already happening. For others, especially those on fixed incomes, it won’t.

The stubborn persistence of 3% inflation—above the Fed’s target but below crisis levels—represents an awkward middle ground. It’s high enough to hurt household budgets but not high enough to justify aggressive policy tightening that might trigger recession. This explains why policy debates have become so contentious. There are no good options, only trade-offs between different types of economic pain.

This also explains the persistent anger despite “improved” economic data. People aren’t confused or manipulated—they’re responding rationally to genuine financial strain. You can’t gaslight someone about their grocery bill. When economists and politicians insist the economy is doing reasonably well while families struggle to afford basics, the credibility gap widens.

The lesson is that economic statistics, however accurate, don’t capture lived experience. Inflation rates and price levels are different things. Growth averages obscure distribution. Unemployment rates ignore underemployment and wage stagnation. Good policy requires acknowledging these gaps rather than dismissing public frustration as ignorance.

We’re living through the aftermath of the sharpest inflation burst in forty years. The rate has come down from its 9% peak, but it remains stubbornly above target at 3%.

Price levels remain dramatically elevated from pre-pandemic baselines. Many households are genuinely worse off. And no amount of economic data showing “improvement” will change how that feels when you’re buying eggs at double their 2020 price.

Well, you could have a long discussion about normalizing any level of inflation. For this piece, let's just say that it would be nice to have a headline metric matching wage increases and government "living standard support payments" (Social Security, unemployment, SNAP, etc.) increases, compared to fiat currency devaluation over the period.