There are no lags in effect of monetary policy

There are no lags in effect of monetary policy

That becomes clear when you consider both money supply & money demand

In 1961, Friedman highlighted the idea that the impact of monetary policy on the economy could be subject to significant delays and uncertain timeframes. This means that changes in the money supply and interest rates might take a long time to influence economic variables, such as output, employment, and inflation, and the timing and magnitude of these effects could vary.

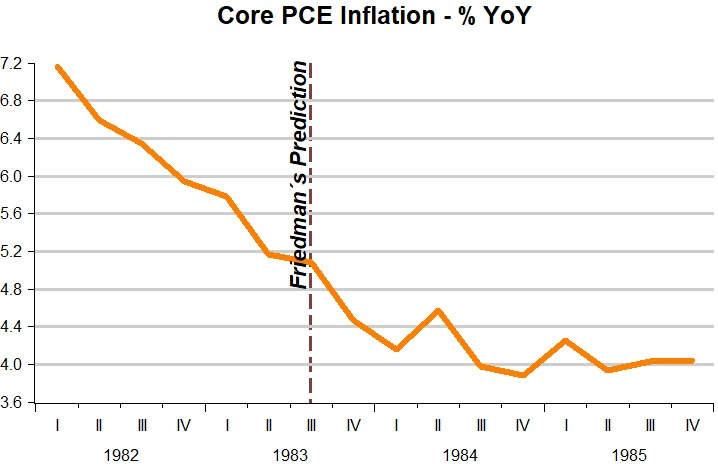

On September 26, 1983, Milton Friedman in his Newsweek column, based on his view of lags in effect of monetary policy, made a bad prediction:

…The monetary explosion did produce vigorous growth. Unfortunately it did continue…Interest rates have already risen sharply. Inflation has not yet accelerated. That will come next year, since it generally takes up to two years for monetary acceleration to work its way through to inflation”.

Inflation, however continued to fall for the next two years!

Jumping to the present, back in April 2020 monetarists were already making predictions about a future increase in inflation due to the “monetary explosion” that was taking place!

An example is Tim Congdon´s “Get Ready for the Return of Inflation” - Fed actions have increased the quantity of money in the US economy at a blistering rate. According to Congdon:

…the Federal Reserve in recent weeks has poured money into the economy at the fastest rate in the past 200 years. Unfortunately, this overreaction could turn out just as poorly; history suggests the US will soon see an inflation boom.

The figures below provide a good example of “lags”. In just a few months after C-19 hit, money supply growth shot up from close to 7% YoY to close to 32% YoY (“the fastest rate in the past 200 years”). During those months, inflation dropped to near 0% YoY. During the next several months, money growth remained very high, and inflation barely rose.

Suddenly, just as money supply gowth began to fall, inflation took off. That would be due to the “lag” in effect of monetary policy, just as inflation turned down after money supply growth had been falling for 16 months!

From that picture, you could easily be convinced that there really are “long and variable lags” in the effect of monetary policy! Furthermore, since for the past few months money growth has been negative (a fall in the money stock), the same monetarists that with a “lag” predicted the inflation boom, now predict that although inflation will keep falling, a recession is in the cards!

Just by introducing a new “actor” into the “play”, lags dissapear! That new “actor” is money demand (or Velocity, its inverse). It stands to reason that an increase in money supply growth will only bring inflation if it exceeds money demand growth. So, if money supply grows but money demand grows even more (velocity falls by more), inflation will fall (and without any “lag”)"!

The next figure adds velocity growth to the money supply growth chart. We immediately observe that the monetary “explosion” was “required” given that large increase in money demand growth (big fall in velocity growth). Initially money supply growth was less than necessary to satisfy the large increase in money demand, so inflation drops.

Inflation takes off at the exact moment that the increase in velocity (fall in money demand) is greater than the fall in money supply growth! Thereafter, inflation remains on the rise as money supply growth remains positive while money demand growth falls (velocity growth positive).

Inflation only reverses when money supply growth falls (and then turns negative) by more than velocity increases (money demand falls). In other words, when the excess supply of money is being worked off.

The upshot is that inflation will remain on a downtrend as long as money supply gowth more than offsets the growth in velocity (fall in money demand growth). If that requires a negative growth rate of the money supply, so be it. A recession will only happen when and if the Fed tightens excessively, i.e. allows an excess demand for money to take place!

Link: https://www.frbsf.org/economic-research/publications/economic-letter/2023/may/rise-and-fall-of-pandemic-excess-savings/

The conversion of time deposits, gated deposits, to demand deposits should slow the velocity of money by the 4th qtr. of 2023.

“aggregate excess savings would likely continue to support household spending at least into the fourth quarter of 2023.”

Y-o-y comparisons aren't valid measures.

And income velocity is a contrivance. You see Milton Friedman was "one dimensionally" confused:

re: ” as income velocity that cannot but impress anyone who works extensively with monetary data” (Friedman, 1956, p. 21).

George Gavey was right.