The stages of the pandemic-induced crisis

The stages of the pandemic-induced crisis

The Fed´s monetary policy plays the "star role"

Jeanna Smialek´s NYT piece from 3 weeks ago is representative of a widely shared view:

Some Federal Reserve officials have begun to acknowledge that they were too slow to respond to rapid inflation last year, a delay that is forcing them to constrain the economy more abruptly now — and one that could hold lessons for the policy path ahead.

As we´ll see, the Fed was not “slow” at all but purposely acted - even if it was unaware - to bring about the “rapid inflation” observed after mid-21!

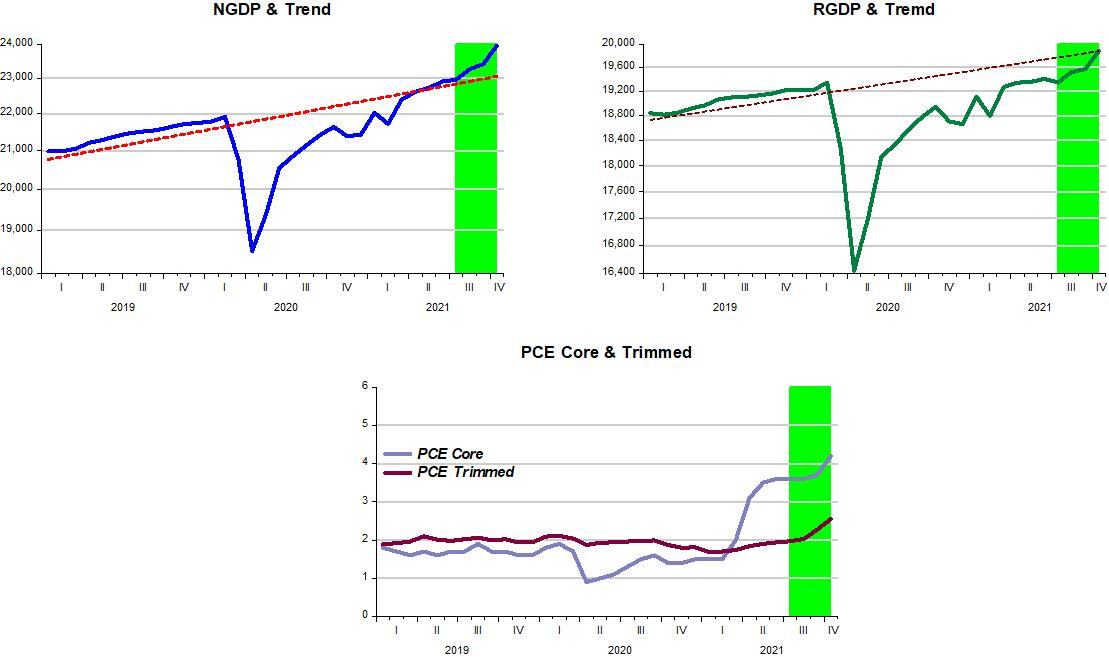

The easiest and clearest way to analyze the process is to set it up through “stages”. The “stages” are defined by the behavior of monetary policy.

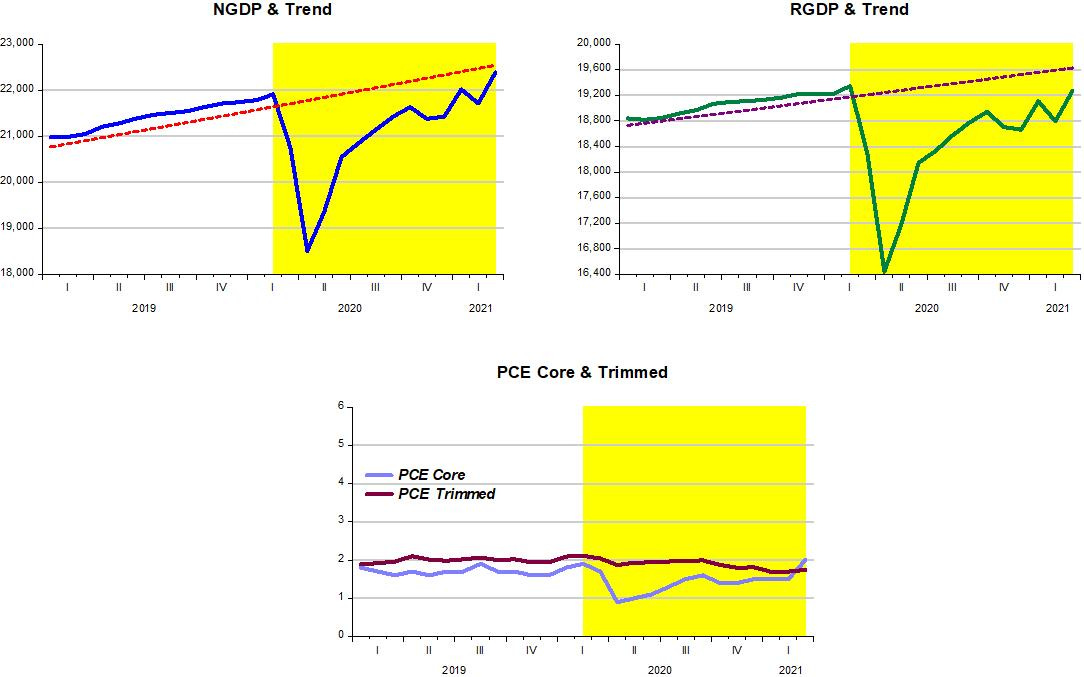

In “stage 1”, demarcated by the yellow band, we observe the pandemic, through both supply and demand effects (with demand effects working through a massive drop in velocity), led to a large drop in nominal spending (NGDP). Real output also dropped far below the level associated with just the supply constraints from lockdowns and supply chain disruptions.

The Fed, however, was quick to react, and soon both NGDP & RGDP were climbing back to the post GR trend path. Some measures of inflation dropped, while less volatile measures did not even have time to react! Thirteen months after the peak, aggregate nominal spending was back on the trend path, real output was lower than before the pandemic, constrained by the supply shocks, and inflation was hovering at the 2% target rate.

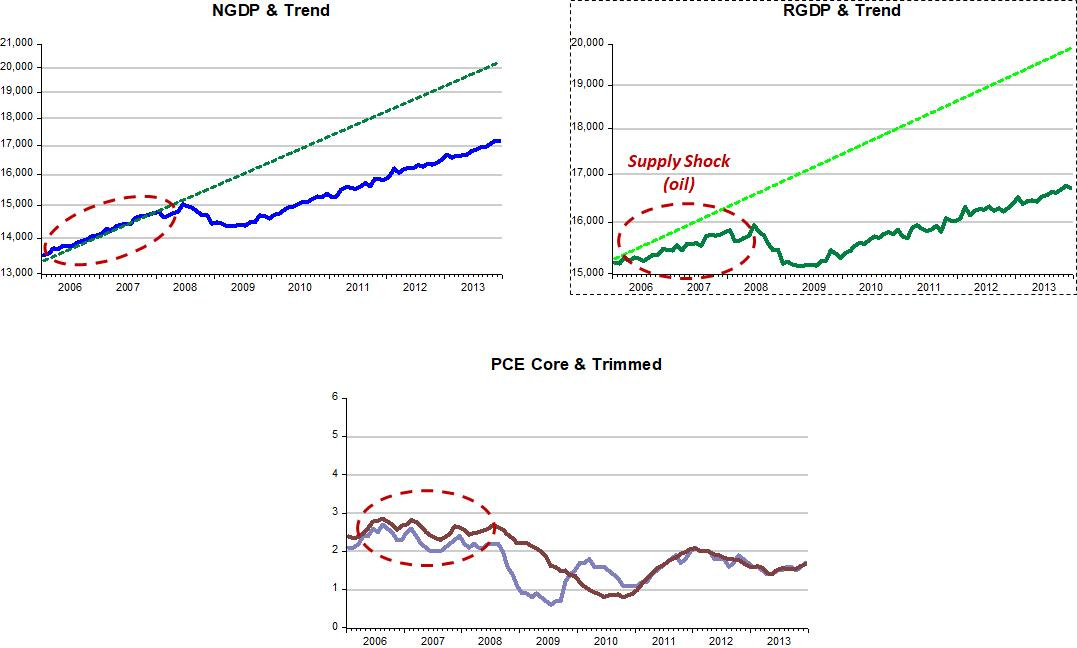

It´s illustrative to compare the Fed´s reaction to the pandemic with what the Fed did leading to the Great Recession.

As soon as Bernanke takes the Fed´s helm, the economy is buffeted by oil shocks. Initially, BB conducts monetary policy so as to keep NGDP sliding along the trend path. Inflation (even of the core variety) goes up a bit and, as predicted by the Dynamic AS/AD model, RGDP recoils somewhat. In mid-08, however, the Fed botches its job, allowing NGDP to tank.

If the Fed reacted as it should, undoing its mistake, it would work to take NGDP back to the trend path it was on, just as it did following the pandemic. But then, the Fed would be explicitly acknowledging it had blundered, and that´s a “no no” in Fed culture going back at least to 1937! Instead, it kept NGDP evolving along a lower trend path and said “it was doing all it could”!

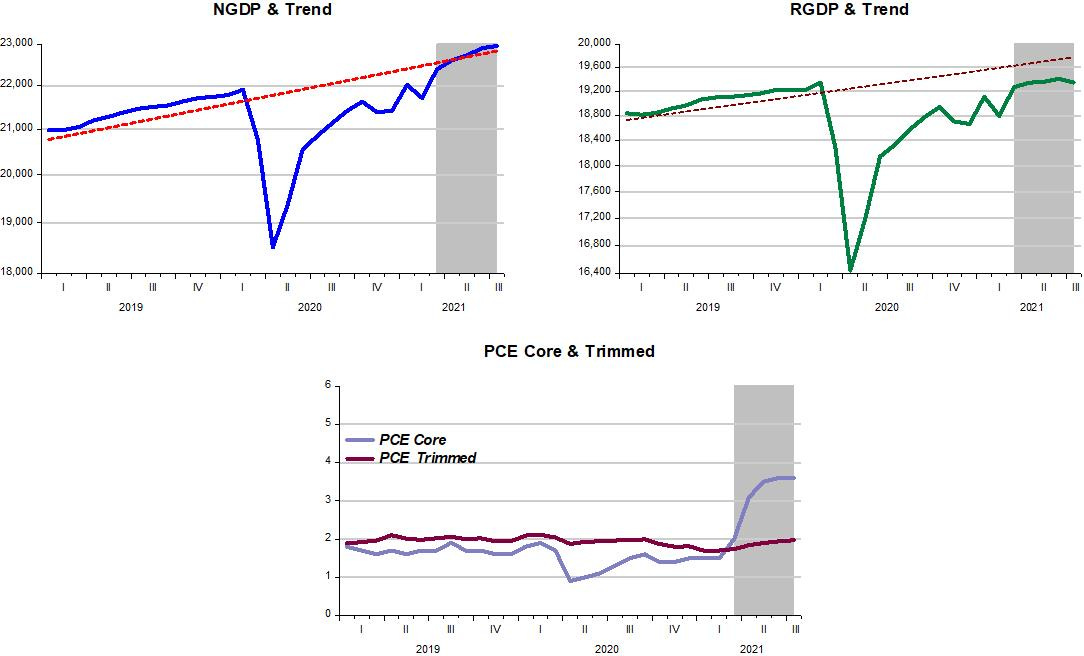

During Stage 2, the Fed continues its “stellar” monetary policy. Having brought NGDP back to trend, it keeps it there. All the inflation experienced during those months are exclusively due to supply constraints, that became binding at that point with real output remaining flat despite NGDP rising “on trend”.

The Fed should have continued to calibrate monetary policy in order to keep NGDP evolving along the trend path. Core PCE quickly stopped rising while the “super core” measure given by the trimmed PCE remained stable and close to the 2% target rate.

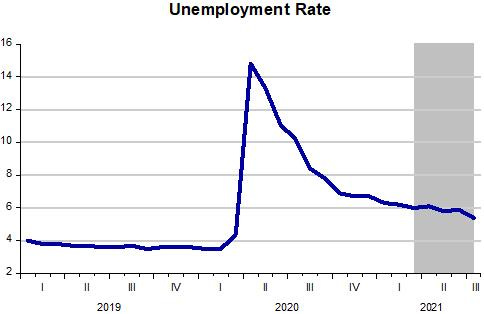

Maybe not satisfied with the unemployment rate remaining close to 6%, the Fed made its first mistake since the start of the pandemic and allowed NGDP to go “overboard” leading to Stage 3.

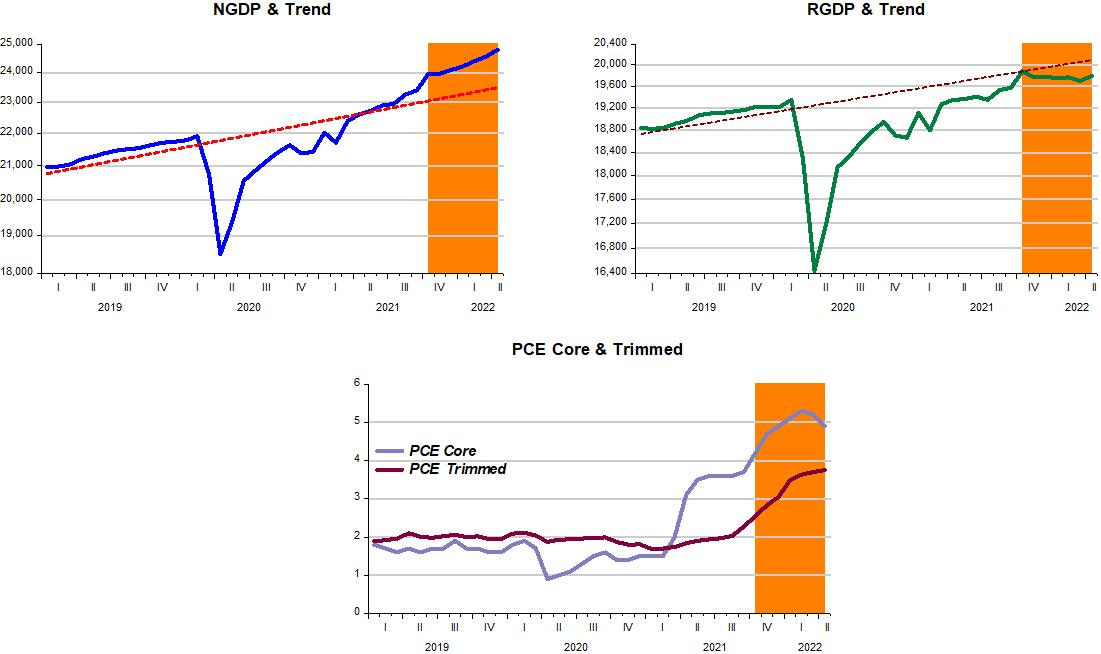

In Stage 3, NGDP goes above trend, pushing RGDP back to trend and thus “disrespecting” supply constraints. The consequence was a “generalized” increase in inflation, this time demand-induced.

In fall 21, the Fed changed tack, trying to restrain the path of NGDP. This marks the start of Stage 4. “Demand pressure” is somewhat reduced so that real output backs down, more in line with supply constraints. Inflation soon tapers of and more recently shows signs of reversing.

Inflation expectations (as gleaned from the 5yr-5yr forward inflation expectations) show a close relationship with the Stages of the crisis. When NGDP goes back to trend in March 21, supply constraints become binding and some measures of inflation increase. When monetary policy changes tack in the Fall of 21, inflation expectations trend down before going up again when Russia invades Ukraine. They have since come down to reflect the changed tack of monetary policy which remains in place.

To recapitulate: Until Spring 21, the Fed´s monetary policy was very appropriate. The “Summer heat” knocked it off the “good path”. In the Fall the Fed tried to regain “control”. Although it did to some extent, it still has work to do to get NGDP back on the “nominal stability path”.

How can it “best” accomplish that task. “Best” here is in the sense of “least traumatic”. Below I plot a “desired” Stage 5, where over the remaining months of the year, the level of NGDP smoothly falls toward the post Great Recession trend path.

The “mechanics” behind that NGDP path is closely related to the behavior of velocity. Velocity is still well below the pre pandemic level, but has been gradually rising. The chart below illustrates with three alternative paths for velocity going forward and the corresponding path of Divisia M4 money supply that offsets the change in velocity so as to keep NGDP on the “path to nirvana”!

If the “script” above is followed with some success, a recession is very unlikely (unless due to war, lingering effects of pandemic, or something “new” supply shocks are “beefed-up”). Inflation due to demand growth will come down, although the part of inflation due to supply shocks will remain “alive”. That, however, should not be a concern for the Fed, which will do its best if it keeps NGDP evolving along the trend level path.

This article by Steven Roach amused me greatly: “Jerome Powell’s Volcker Deficit”

If the US Federal Reserve wishes to avoid a return to stagflation, it must recognize the huge gulf between the level of real interest rates under former Fed Chair Paul Volcker and the current incumbent. It is delusional to think that today’s wildly accommodative monetary policy can solve the worst inflation problem in a generation.

Poor Jerome Powell. With US inflation close to a 40-year high, the Federal Reserve chair knows what he needs to do. He has professed great admiration for Paul Volcker, his 1980s-era predecessor, as a role model. But, to paraphrase US Senator Lloyd Bentsen’s famous 1988 quip about his vice-presidential rival, Senator Dan Quayle, I knew Paul Volcker very well, and Powell is no Paul Volcker.

Thank God for small blessings!