The Scapegoat Barrel

Oil Gets the Blame, the Fed Pulls the Trigger, and We Are About to Make the Same Mistake Again

There is a story about oil and inflation that every economics textbook tells, that every central banker of a certain generation internalized, and that has shaped monetary policy in moments of crisis for over half a century.

The story goes like this: oil shocks cause inflation. OPEC cuts production, the price of crude spikes, energy costs transmit through the economy, and inflation follows as night follows day. The Fed’s job, in this story, is to respond — either by tightening to crush the inflationary impulse, or by accommodating it and risking expectations becoming unanchored.

It is a tidy story. It also has the causality largely backwards — at least for the first and most consequential oil shock in modern history. And the consequences of getting the causality wrong have been enormous: a decade of stagflation in the 1970s that need not have been so severe, a recession in 2008 that was significantly deeper than it needed to be, and now, with American bombs falling on Iran and oil prices moving again, the risk of repeating the error a third time.

Part I: The Long Stability and Its Erosion, 1950–1972

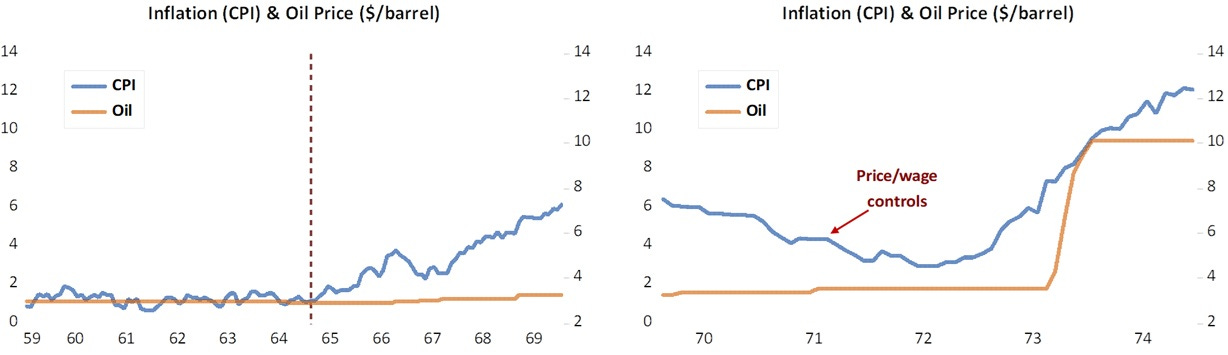

To understand why 1973 happened, you have to understand what preceded it. From the end of the Second World War through the early 1970s, oil prices were remarkably stable in nominal terms — and in real, inflation-adjusted terms, they were actually declining.

Oil prices (WTI), traded on average a bit below $3 per barrel through most of the 1950s and into the 1960s and mid 1973.

The world was awash in cheap Gulf oil, the international oil companies — the “Seven Sisters” — dominated production and pricing through long-term concessionary arrangements with producing nations, and OPEC, founded in 1960 by Saudi Arabia, Iran, Iraq, Kuwait and Venezuela, was a diplomatic talking shop rather than a functioning cartel. It had never successfully coordinated a production cut.

What changed was not OPEC. What changed was the dollar.

The postwar Bretton Woods system had pegged the world’s major currencies to the dollar at fixed exchange rates, and the dollar itself was pegged to gold at $35 per ounce.

Oil was priced in dollars. As long as the dollar was stable — as long as American monetary policy was disciplined enough to sustain the gold peg — oil producers received a predictable return on their most valuable asset. The system worked because it imposed a constraint: the United States could not inflate its way out of obligations without breaking the peg.

The constraint began to fracture in the mid-1960s. President Johnson’s decision to finance both the Great Society and the Vietnam War without raising taxes — guns and butter, as the shorthand had it — required monetary accommodation.

The Federal Reserve, under Chairman William McChesney Martin and then Arthur Burns, allowed money supply growth to accelerate. Inflation, which had been barely perceptible through the early 1960s, began climbing: 3% by 1967, 5% by 1969, refusing to come down even as Nixon applied modest fiscal and monetary restraint in 1969-70.

By 1971, the arithmetic had become untenable. Foreign central banks, accumulating dollar reserves they increasingly suspected were overvalued, were presenting them for gold conversion at the fixed $35 rate. The United States was hemorrhaging gold.

On August 15, 1971, Nixon closed the gold window — suspending convertibility unilaterally, in what French Finance Minister Valéry Giscard d’Estaing had years earlier called the “exorbitant privilege” of the reserve currency issuer turned into an exorbitant burden it was no longer willing to bear.

The dollar promptly fell. By the time the Smithsonian Agreement of December 1971 attempted a managed realignment, the dollar had been devalued roughly 8% against gold. It was not enough. By early 1973, the Bretton Woods system was functionally dead, floating exchange rates arrived, and the dollar fell further — perhaps 20% in trade-weighted terms from its 1971 peak by the time the dust settled.

Now consider what this meant for oil producers. Their asset — crude oil in the ground — was priced in a currency that was losing value in real terms. Every barrel they pumped and sold for dollars bought fewer German machine tools, fewer Japanese cars, fewer French luxury goods than it had five years earlier. The real price of oil, from the producer’s perspective, was being eroded not by any decision they had made but by American monetary policy and the collapse of the dollar’s purchasing power.

This is the context in which the 1973 oil shock must be understood. OPEC did not cause the inflation of the 1970s. The inflation of the 1960s and early 1970s — created in Washington, monetized by the Federal Reserve, and transmitted globally through the reserve currency — created the conditions that made OPEC’s 1973 action both possible and, from the producers’ perspective, rational. The Yom Kippur War provided the political trigger and the cover. But the economic logic had been building for almost a decade.

The tail did not wag the dog. The dog had been running in circles for years before the tail finally moved.

Illustrations:

Part II: 1973 and Its Aftermath — Misreading the Cause, Compounding the Error

When OPEC imposed its oil embargo in October 1973 and production quotas cut supply sharply, the price of oil jumped from around $3 per barrel in August 1973 to $10 by January1974 — a more than threefold increase in a matter of months. Inflation, already running above 6% in the United States, accelerated further. The conventional diagnosis was immediate and almost universally accepted: the oil shock had caused the inflation surge.

The Federal Reserve, under Arthur Burns, responded with what can only be described as paralysis dressed as pragmatism. Burns was convinced — or convinced himself — that oil-driven inflation was different in kind from monetary inflation, that raising interest rates to crush an oil shock would impose unnecessary recession without addressing the supply-side cause.

He allowed money supply growth to remain loose. The consequence was that what could have been a temporary price level adjustment — oil goes up, other prices adjust, real incomes take a one-time hit, and inflation returns to its prior trend — became instead an embedded inflationary psychology. Wage demands rose to compensate for oil-driven price increases. The Fed accommodated the wage settlements with further money creation. Expectations became unanchored.

The second oil shock of 1979 compounded the error but through a different mechanism. By then, inflation had never been properly purged from the system. It had settled into a stubborn 6%-8% range since 1976 — high enough to be painful.

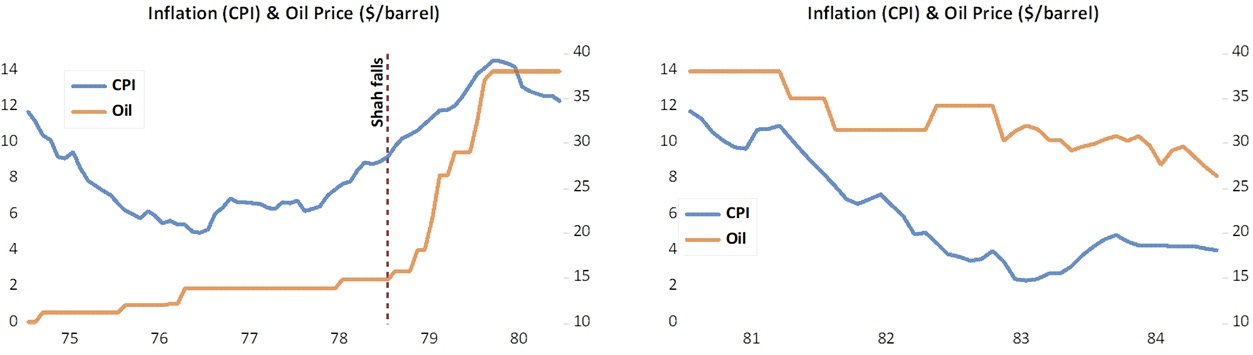

The trigger this time was not a dollar devaluation but a genuine supply disruption: the Iranian Revolution of 1979 removed Iran — then the world’s second-largest oil exporter — from the market. The Shah fell in January, Iranian oil workers went on strike, production collapsed from 5.5 million barrels per day to less than 1 million. The price of crude more than doubled between 1979 and 1980, from around $15 to $38 per barrel.

The 1979 shock was, more than 1973, a genuine supply shock — caused by political revolution rather than monetary grievance. But it landed on an economy whose inflation psychology had already been corrupted by a decade of accommodation.

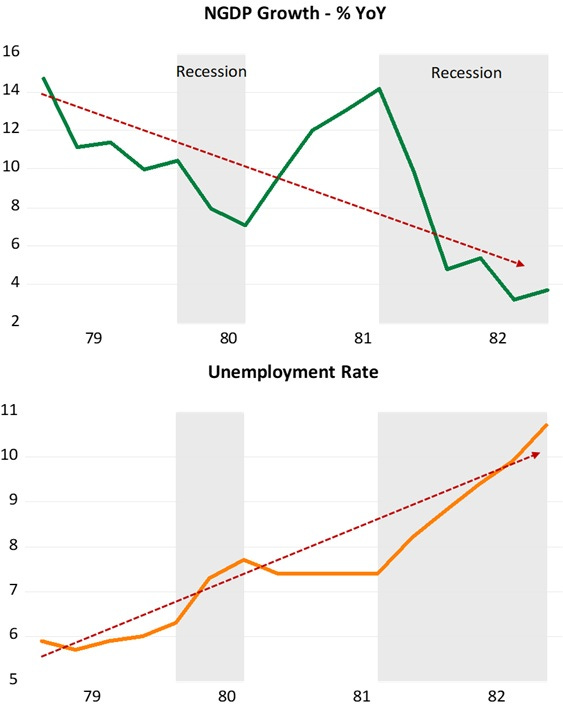

The Fed’s response, first under G. William Miller and then under Paul Volcker, determined the outcome. Volcker chose to break the cycle by any means necessary. He strongly constrained NGDP growth. Unemployment reached 10.8%. Two recessions followed in quick succession. It worked — inflation was crushed — but the cost was enormous, and much of it was attributable to the decade of accumulated error that preceded Volcker’s shock therapy which had taken NGDP growth to “wuthering heights”.

The story illustrated

Part IIA: The Gulf War Oil Shock and the Fed’s Monetary Mistake (1990–1991)

Among the clearest illustrations of how central bank misperception can translate an adverse supply shock into a fully-fledged recession is the episode surrounding Iraq’s invasion of Kuwait in August 1990. The episode is instructive not because the Federal Reserve acted with unusual recklessness, but precisely because its mistake was so conventional — a textbook case of allowing headline inflation to dictate monetary policy in circumstances that did not warrant tightening.

The Oil Shock and the Inflation Signal

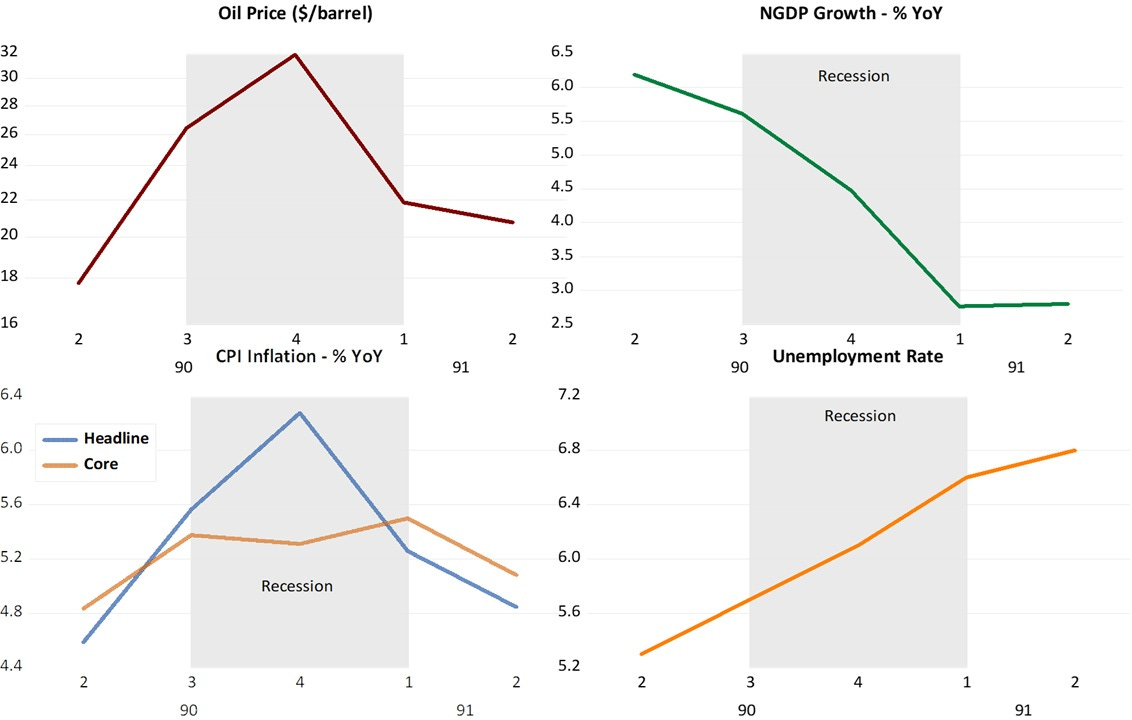

The invasion triggered an immediate spike in crude oil prices, which more than doubled between July and October 1990, rising from around $17 per barrel to a peak above $40.

Because energy costs feed directly into the consumer price index through petrol, heating fuel, and transport, measured headline CPI inflation rose sharply. By late 1990 headline inflation was running at an annualised rate that alarmed policymakers who had spent the better part of a decade rebuilding the Fed’s anti-inflationary credibility in the aftermath of the Volcker disinflation.

The critical analytical error lay in treating this rise in headline CPI as evidence of a generalised, demand-driven inflation that monetary restraint could and should suppress.

In fact, the price signal was almost entirely the product of a one-time, exogenous supply disruption concentrated in a single commodity market. Core inflation — stripping out energy and food — moved far less dramatically. The oil price rise did not reflect an overheated economy in which aggregate nominal spending was outpacing productive capacity; it reflected a geopolitical shock to a specific input price.

The Fed’s Response: Tightening into a Weakening Economy

Rather than accommodating the relative price shift while keeping nominal expenditure on a stable path, the FOMC responded by keeping monetary policy tight. Greenspan and the Committee were caught between the visible rise in headline prices on one side and growing signs of a softening economy on the other, and their hesitation proved costly.

The consequence was a contraction in nominal GDP growth. By tightening as private-sector demand weakened, the Fed allowed NGDP growth to fall well below its prior trend — from nearly 7 percent annually in the late 1980s to a sharp slowdown through 1990 and into 1991.

This was not merely a statistical artefact: it represented a genuine tightening of monetary conditions that bore down on businesses, households, and financial institutions already under stress.

The Resulting Recession

The United States entered recession in July 1990, with the downturn lasting until March 1991 — eight months per the NBER chronology. The recession was relatively brief and shallow compared with the contractions of 1973–75 and 1981–82, but it was nonetheless a policy-induced amplification of what need not have been more than a temporary drag on real incomes from higher energy costs.

Unemployment rose from around 5.2 percent in mid-1990 to a peak of 7.8 percent in mid-1992, continuing to deteriorate well after the technical end of the recession — a pattern consistent with a nominal demand shortfall that tight monetary policy produces.

The banking sector, already weakened by the savings and loan crisis and a declining commercial real estate market, was further squeezed by the contraction in nominal spending. Many institutions found that the nominal revenues of their borrowers were insufficient to service debts contracted in a higher-NGDP environment — a classic debt-deflation dynamic that tighter money had helped to produce.

The Lesson: Supply Shocks and Nominal Demand

The Gulf War episode illustrates what market monetarists and NGDP-targeting advocates would later formalise: in most circumstances, the correct response to an adverse supply shock is to stabilise nominal spending, not to tighten in response to the resulting headline price increase.

When a supply shock raises the price level, some combination of lower real output and higher prices is inevitable in the short run. Monetary tightening does not undo the real cost of the shock; it merely adds a second layer of damage by also compressing nominal demand.

The 1990–1991 recession was not, in this reading, an inevitable consequence of the Gulf War. It was the avoidable product of a monetary framework that targeted observed inflation rather than the path of nominal expenditure — and that therefore responded to a supply shock in exactly the wrong direction.

It is a mistake the Fed would repeat, in structurally similar form, in 2008, and one that the history of monetary policy suggests central banks remain at chronic risk of repeating so long as headline inflation remains their primary guide.

The story illustrated

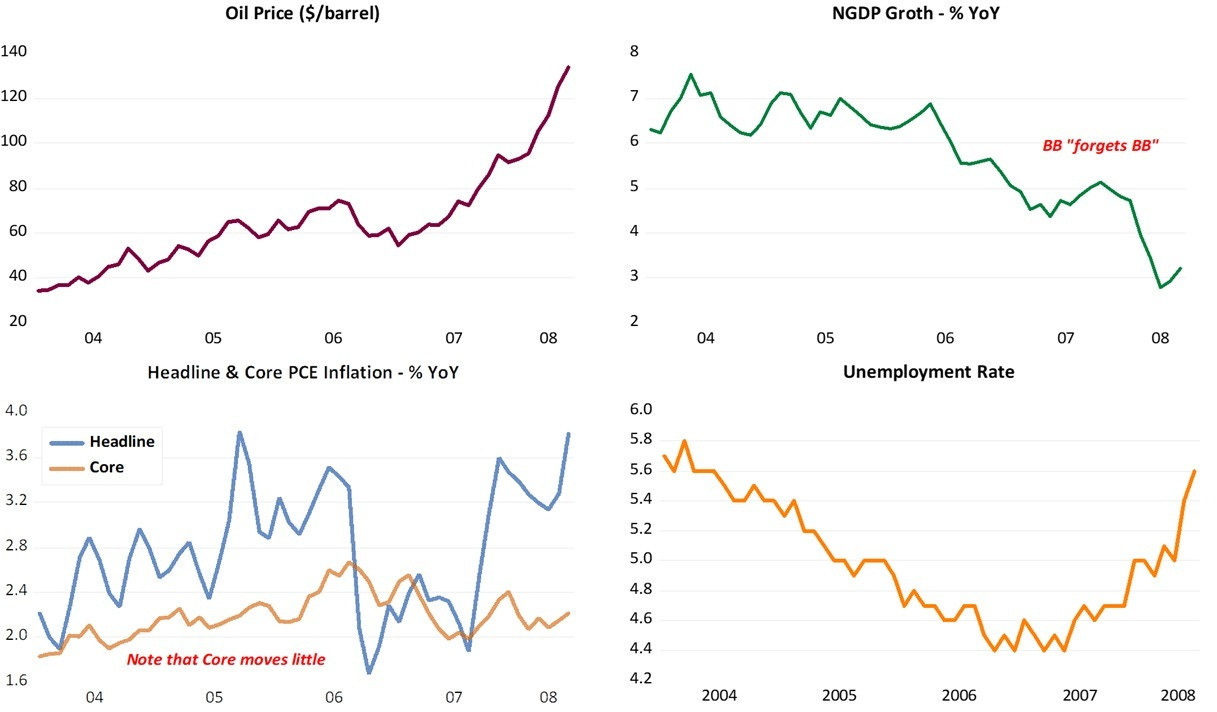

Part III: 2003–2008 — A Different Kind of Oil Shock

The oil price surge of the mid-2000s had a fundamentally different character from both 1973 and 1979. This was not an OPEC production cut, not a supply disruption caused by political upheaval, and not — at least initially — a monetary phenomenon. It was demand-driven, propelled by the extraordinary growth of China and its multiplier effects on the developing world.

China’s industrialization in the 2000s was the largest and fastest structural transformation of an economy in human history. Steel production, cement, automobiles, manufacturing exports — all surged simultaneously.

Chinese oil consumption roughly doubled between 2000 and 2008. The ripple effects spread through emerging markets: commodity exporters in Latin America, Africa and the Middle East experienced terms-of-trade windfalls that generated their own growth and demand.

Global oil consumption was rising faster than the industry’s capacity to expand supply. Oil, which had traded below $30 per barrel as late as 2003, reached almost $140 in July 2008.

This created an intellectually important distinction: a permanent upward shift in demand for a resource in temporarily inelastic supply produces a price spike that is, in principle, self-correcting over time as supply responds, alternatives develop, and demand adjusts at the margin. It is not, in the strict monetary sense, inflationary — it is a relative price change, a shift in the terms of trade between oil-importing and oil-exporting economies.

Ben Bernanke understood this distinction. Or rather, he had understood it. In a 1997 paper co-authored with Mark Gertler and Mark Watson Bernanke had argued that the recessionary consequences of oil shocks were not primarily caused by the oil shocks themselves.

They were caused by the Federal Reserve’s response to oil shocks. When oil prices rose and headline inflation ticked up, the Fed tightened. That tightening — not the oil price itself — was what crushed growth. The paper’s simulation evidence suggested that if monetary policy had held steady in response to oil shocks, much of the recessionary impact would have been avoided.

This was an important result. It meant that the standard narrative — oil shock causes inflation, Fed tightens, recession follows — was misattributing causation. The villain of the story was not OPEC. It was the Federal Open Market Committee.

Part IV: Bernanke Forgets Bernanke

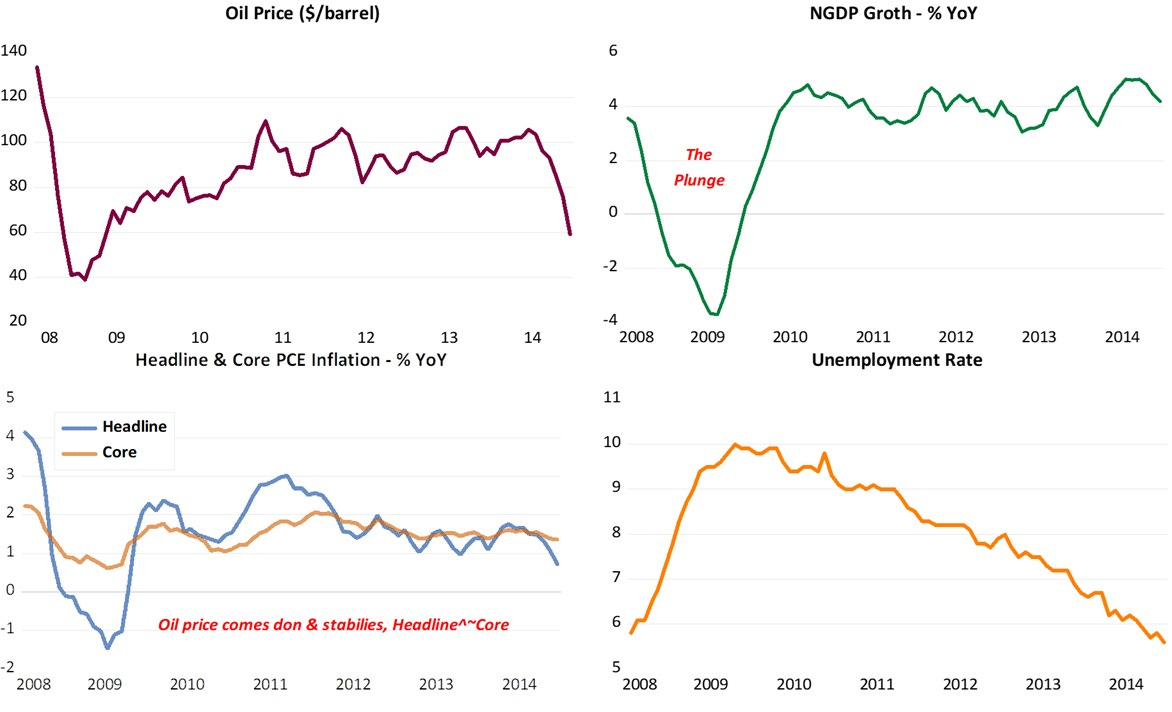

In 2008, Bernanke was no longer a Princeton professor. He was Chairman of the Federal Reserve, and he was watching oil prices approach $150 per barrel while headline CPI inflation rose above 5%. And he did precisely what his 1997 paper had warned against.

The FOMC held the federal funds rate at 2% through the first half of 2008, but — critically — it allowed nominal GDP growth to decelerate sharply. The economy had entered recession in December 2007, largely as a result of the housing and credit crisis that had been building since 2006.

The correct response to a simultaneous supply shock (oil) and demand collapse (housing, credit, consumer spending) was to maintain nominal spending growth — to prevent the contraction in nominal GDP that would transform a financial crisis into a depression.

Instead, the Fed’s implicit tightening bias in the face of headline inflation allowed nominal GDP growth to turn sharply negative in the third and fourth quarters of 2008, from an annualized rate of around 4% to negative 8% — one of the steepest NGDP collapses in postwar history.

What Bernanke had forgotten, or set aside in the heat of the moment, was the distinction between headline and core inflation — and between a relative price level shock and a sustained inflationary process.

Core inflation in 2008 remained relatively subdued. The 4% headline number was being driven almost entirely by energy and food. A central bank focused on core inflation, or better still on nominal GDP growth as its target, would have recognized that the appropriate response to an oil-driven headline spike in the middle of a demand collapse was accommodation, not restraint.

The consequences of that error were not modest. The Great Recession of 2008-2009 was the worst economic contraction since the 1930s. Unemployment reached 10%. Output fell 4.3% in real terms. The financial system was brought to the edge of collapse.

Much of this severity was attributable to the housing and credit crisis — but the Fed’s monetary policy error compounded it significantly, just as Bernanke’s own 1997 research had predicted it would.

It is one of the more painful ironies in the history of economic thought: the scholar who best diagnosed the mechanism by which monetary policy transforms oil shocks into recessions became, a decade later, the policymaker who repeated the error.

The story illustrated

The aftermath

Part V: Now — Iran, Oil, and the Fork in the Road

American strikes on Iran that began on February 28, 2026 have sent oil from $67 to above $114 per barrel (in Asia Monday morning) in the immediate term, with Goldman Sachs projecting $130 if the Strait of Hormuz — through which 20% of global oil supply transits — is disrupted or closed. The IRGC has threatened exactly that closure. Six major shipping companies have already halted Gulf transits.

The question for monetary policy is the one Bernanke’s 1997 paper addressed: how should the Fed respond?

The temptation will be to tighten. Headline inflation, already at 2.4% and only recently returned to near-target levels after the post-Covid surge, will rise with oil prices. The political pressure to demonstrate anti-inflationary resolve — already complicated by the administration’s simultaneous demands for rate cuts — will be intense. The ghosts of 1979, of Burns and accommodation and unanchored expectations, will haunt the FOMC meeting room.

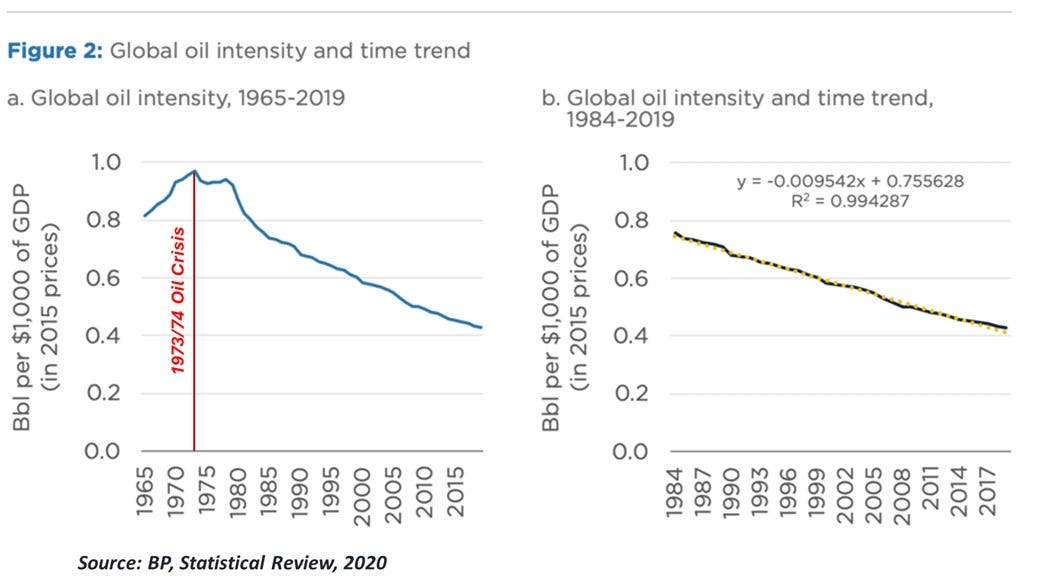

But the situation is importantly different from 1979 in ways that argue for a different response. The oil intensity of global GDP has fallen by more than 55% since 1973. The world now produces a dollar of output using less than half the oil it required at the peak. The direct transmission from oil prices to consumer prices is correspondingly weaker.

Services — which dominate modern economies and are less energy-intensive than manufacturing — constitute a far larger share of GDP. Core inflation, which strips out energy, remains the better measure of underlying inflationary pressure, and if it remains subdued in the coming months, the case for tightening is weak.

More importantly, the Bernanke-Gertler-Watson lesson holds: the critical variable is not the oil price but nominal GDP growth. If the Fed allows NGDP to contract in response to an oil shock — if it permits the monetary tightening that transforms a relative price adjustment into a demand collapse — it will have made the 2008 mistake again. The oil price, whatever it does, will have been the scapegoat for a monetary policy error.

The correct response is to look through the headline number, maintain nominal spending growth at a rate consistent with the 2% inflation target over the medium term, and allow the oil price shock to work itself through as the supply disruption it is rather than treating it as evidence of a sustained inflationary process requiring monetary correction.

This requires, however, something that is in increasingly short supply in Washington: institutional independence and analytical clarity.

A Fed under political pressure to cut rates for growth while simultaneously confronting oil-driven headline inflation is being pulled in two directions by one underlying shock. The discipline required is to ignore both pressures — the political demand for accommodation and the populist demand for toughness — and to focus on the one variable that actually matters: is nominal GDP growing at a rate consistent with the economy’s productive capacity?

Epilogue: The Same Mistake, the Same Story

From 1973 to 2026 is more than fifty years. Three generations of economists have been trained on the oil-shock-causes-inflation narrative. Central banks have built communication strategies, institutional mandates and decision frameworks around it. And the narrative is not entirely wrong — oil prices do affect inflation, especially in the short run, especially in economies with strong wage-price indexation.

But the deeper causal story runs the other way. Monetary disorder creates the conditions for oil shocks by eroding the real value of dollar-denominated oil revenues and destabilizing the international monetary arrangements on which stable commodity pricing depends. And monetary tightening in response to the resulting price spike is what converts a manageable supply disruption into a prolonged recession.

The barrel gets the blame. The Fed pulls the trigger.

We are at another such moment. The bombs have already fallen. The oil price is already moving. The Fed will face the same choice it has faced before: look through the headline number and protect nominal demand, or tighten in the face of the spike and risk compressing an economy already running on a narrow base of asset appreciation and AI investment.

Ben Bernanke, the scholar, knew the right answer in 1997. The question is whether the institution he once led — and the institution it has since become — remembers it.

.

This post should be required reading.

The Pentagon caused the dollar drain. The private sector remained in surplus. Then velocity accelerated faster than money because of the monetization of time deposits and the FEDs interest rate bracket racket.

Volcker caused 2 back-to-back recessions. He never tightened monetary policy. The Great Moderation was due to the DIDMCA of March 31st 1980 which curbed velocity.

Bernanke was just dumb as a rock decelerating N-gDp.