The pathway for Powell & the FOMC to gain confidence

The pathway for Powell & the FOMC to gain confidence

stop babling about interest rates

My fellow MM traveller Alex Schibuola sent me this comment on my previous post:

Interesting post, Marcus. The core HCPI series does raise my eyebrows. But, I have difficulty squaring it with NGDP growth being in the 5-6% range. My priors lead me to see 4% as the desirable pace. Any thoughts on why I should favor HCPI over NGDP as an indicator at this moment?

To which I responded:

You shouldn´t favor HCPI over NGDP. I feel very strongly that "on target inflation", as measured by the HCPI reflects the fact that NGDP growth is not far from "ideal"! Probably will use the latest issue of SP Global monthly data that came out yesterday this weekend.

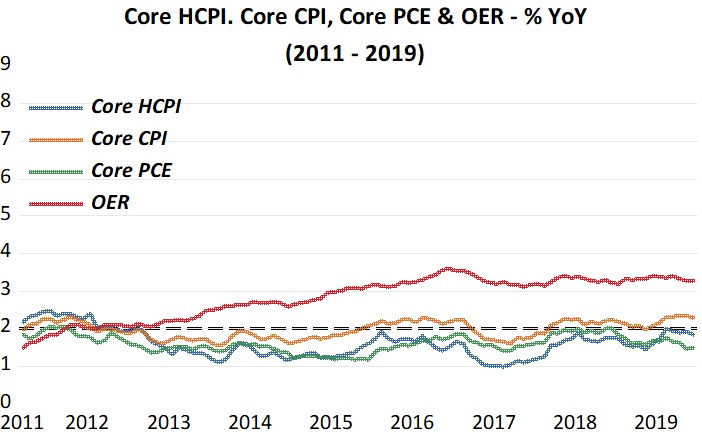

So here I am and will try to show that inflation, as measured by the harmonized CPI, is a plausible indicator that NGDP growth is close to “ideal”.

The basic property of an “ideal” NGDP growth is that it is stable (the level trend path along which this happens is important but I will not be concerned with that here).

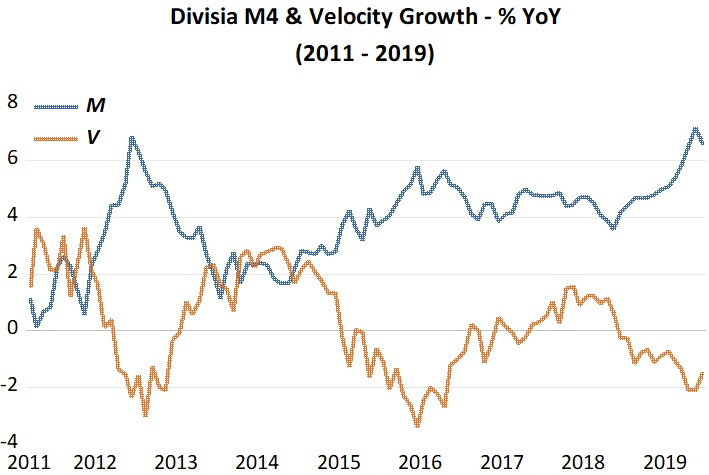

From the equation of exchange in growth form (m+v=p+y) a stable NGDP (p+y) growth rate will happen if money supply growth (m) “adequately” offsets changes in velocity (v) growth. So, for example, if v falls (money demand rises), if m does not rise to offset the fall in v, NGDP growth will fall. Conversely, if v rises and m does not fall to off set that change, NGDP growth will rise.

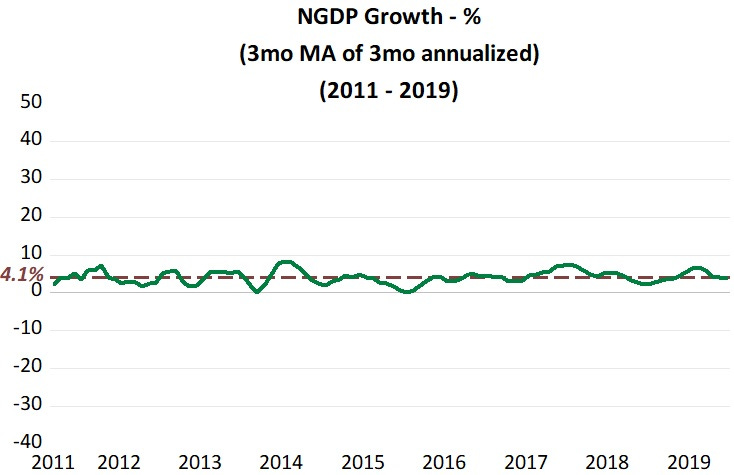

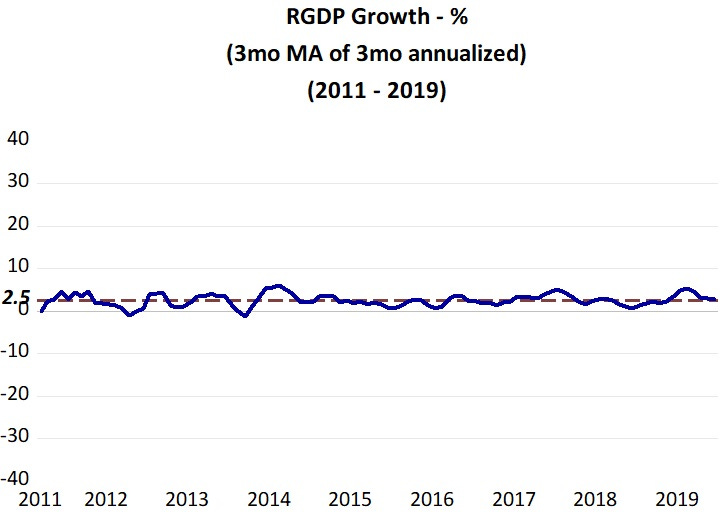

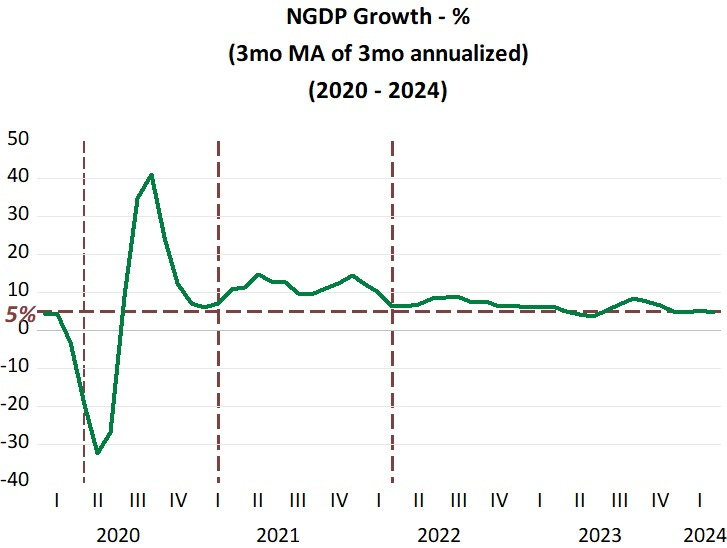

The 2010s provide a good visual of a stable NGDP growth (nominal stability) and the cause and consequences of that stability. The first chart illustrates the cause, showing that changes in m closely offsets changes in v so as to keep NGDP growing a little over 4%.

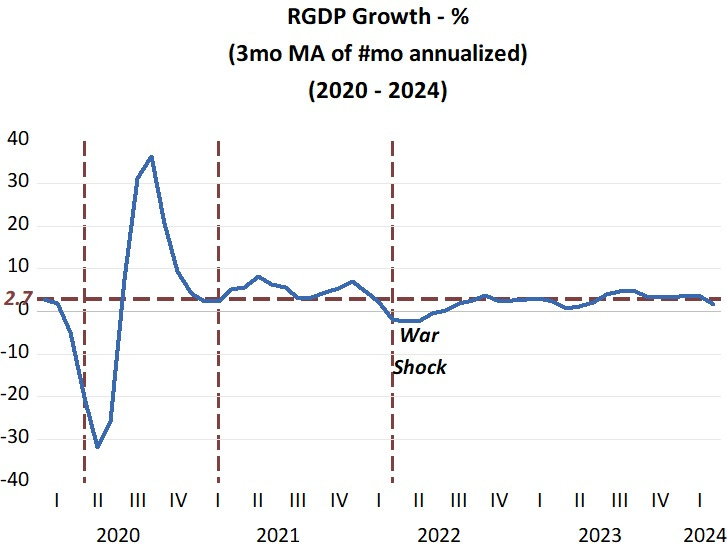

(Obs: With the exception of the Money - Velocity chart, all the others have the same scale for the 2 periods 2011-2019 & 2020-2024. Also, the NGDP & RGDP growth charts are smoothed to reduce noise).

The good implication is that a monetary policy that delivers nominal stability, also delivers real output stability and low and stable inflation!

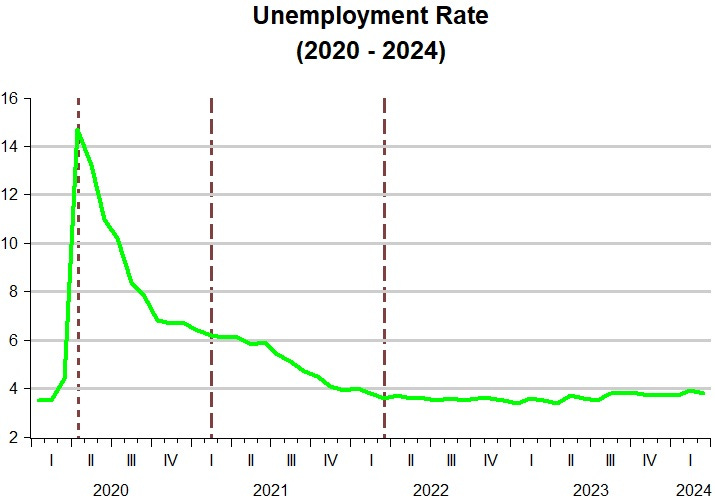

And a falling/low rate of unemployment

.The post 2020 world is much more “exciting” than the 2010s. That´s mostly due to C-19 that surprisingly came along to roughly jostle a “tranquil” world.

The immediate victim was nominal stability, that was lost due to the surprising big drop in velocity growth. The Fed, however, acted quickly and soon was more than offseting the change in velocity, pushing up NGDP growth.

(Note: the verical lines in the charts show “regions” and how they relate to changes in the interplay between money gowth and velocity. For instance, the first region shows all “consequences” of the sudden change in velocity. Region 2, between the first and second vertical lines, show all the consequences of a rising velocity not fully offset by a fall in money growth, and so forth for the other regions).

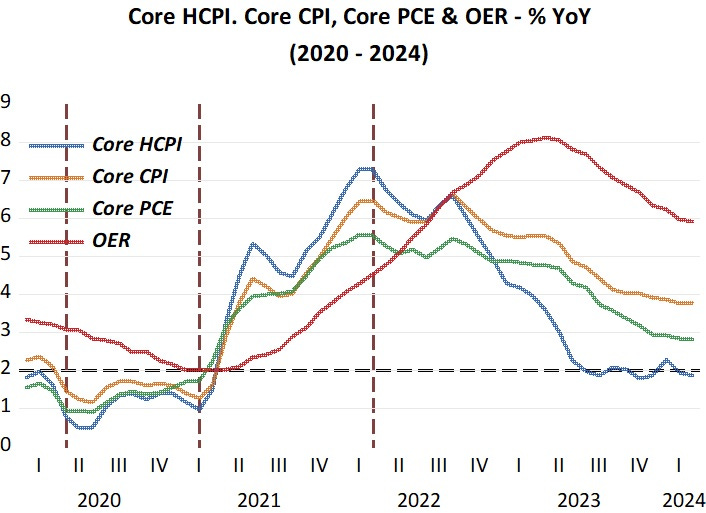

Note that with a one-month delay, smoothed NGDP growth strongly reacts to the the rise in velocity unaccompanied by a fall in money growth. Between the second and third vertical lines, money growth less than offsets the rise in velocity so NGDP growth chugs along at a high rate. As shown in the inflation chart below, during this time inflation is on a rising trend.

Real output growth mimics the moves in NGDP growth. The effects of the oil shock from the Russian invasion is evident, temporarily depressing RGDP growth.

After the third verical line, money growth begins to offset velocity changes so that NGDP growth comes down to a lower growth rate. Inflation follows suit.

The behavior of the unemployment rate is consistent with an economy enjoying the perspective of nominal stability.

With NGDP growth converging to a stable 5% growth rate, for almost two years now, harmonized CPI (which excludes the OER “straw man”) has been on target. If money growth (closely controlled by the Fed) manages to offset velocity so as to keep NGDP growth in the 4.5%-5% range going forward, the CPI and PCE will also converge to target.

On wednesday during his press conferencs following the FOMC Meeting, Powell said:

So far this year, the data have not given us that greater confidence inflation is heading down to 2%.

"It is likely that gaining that greater confidence will take longer than previously expected.

From my standpoint, his lack of “greater confidence” means that he´s not confident that the Fed will be able to adquately offset changes in velocity. But they´re certainly not thinking in those terms, which brings on an “upside-down” worldview by the “masses” such as this:

"The good implication is that a monetary policy that delivers nominal stability, also delivers real output stability and low and stable inflation!"

Is it not also true that policy that delivers low a stable inflation would deliver real an nominal GDP stability?

In your NGDP framework how is optimal NGDP growth estimated?

Thanks for sharing meaningful and valuable analysis.