The ongoing inflation: Fiscal or Monetary?

The ongoing inflation: Fiscal or Monetary?

Is a FTPL revival justified?

In January 203, Princeton University Press will publish John Cochrane´s (of the Hoover Institution) book “The Fiscal Theory of the Price Level” - A comprehensive account of how government deficits and debt drive inflation.

A draft of the book is available here (678 pages).

For the past several months, Cochrane has been writing papers and essays that are “teasers” to the book. A non technical essay is “Fiscal Inflation”, where we read:

Inflation comes when government debt increases, relative to people’s expectations of what the government will repay.

For those interested, other papers and essays on his research can be found here.

Kevin Williamson of the National Review channels Cochrane with a punchy title: “Here Comes Fiscal Armageddon” (gated):

Fiscal Armageddon is coming — eventually. It is necessary not to be an alarmist about that, but equally necessary not to be naïve about it. Fiscal Armageddon is what will happen when the U.S. government’s debt load exceeds its ability to comfortably service that debt. The U.S. government will face a budgetary crisis, possibly a sudden one, and its response to that crisis will create ripples — or a tsunami — across the world economy. How bad it is and how Washington responds will determine the difference between a painful but manageable economic setback and a global catastrophe.

A bit of history is in order. The idea behind the FTPL was “born” a little over 40 years ago, in 1981, with the publication of Sargent & Wallace´s Some Unpleasant Monetarist Arithmetic.

The theme was that monetary and fiscal policy are interrelated and must necessarily be coordinated. The issue of coordination arises when one seeks to answer the question: Is it possible for monetary policy permanently to influence an economy´s inflation rate?

Three years later, Sargent wrote a nontechnical (and applied version) of Some Unpleasant Monetarist Arithmetic, entitled “Reaganomics and Credibility”, where he couches the coordination between monetary and fiscal policy in terms of a “game of chicken”.

My motivation for this post, however, was a recent piece by Robert Barro in Project Syndicate: “Understanding Recent US Inflation”:

Although US monetary policy was too aggressive for too long, the likely culprit behind the recent surge in consumer prices was an extraordinarily expansionary fiscal policy. After all, the Great Recession was also met with an aggressive monetary-policy response, but inflation barely budged for a decade.

Where he also writes:

To assess how inflation responded to this spending, I draw from the “fiscal theory of the price level,” which has been advanced in research by the Hoover Institution’s John H. Cochrane.

If I can convincingly show that Barro´s views on what he calls “aggressive monetary policy” after the Great Recession are wrong, I hope to put doubt into the whole edifice of the FTPL!

I start off with the equation of exchange, where:

MV=Py

with M=money supply (I use the broad measure of M, the M4 Divisia Monetary Index proposed by William A. Barnett), V=velocity of Divisia M4 circulation, P=Price level and y=real output.

Instead of the usual approach of turning the equation of exchange into the QTM (Quantity Theory Of Money) by the assumption that V is stable, and getting, in terms of growth rates, the result that

m-y=p (since v=0)

which leads to the meme that inflation follows from “too much much money chasing too few goods”, I prefer to look at the equation of exchange as an analog of a “thermostat”, where M (the “thermostat”) works to offset changes in the “outside temperature”, V, so as to keep the “inside temperature”, Py (or aggregate nominal spending, or NGDP), stable.

Here I want to contest Barro`s affirmation that:

After all, the Great Recession was also met with an aggressive monetary-policy response, but inflation barely budged for a decade.

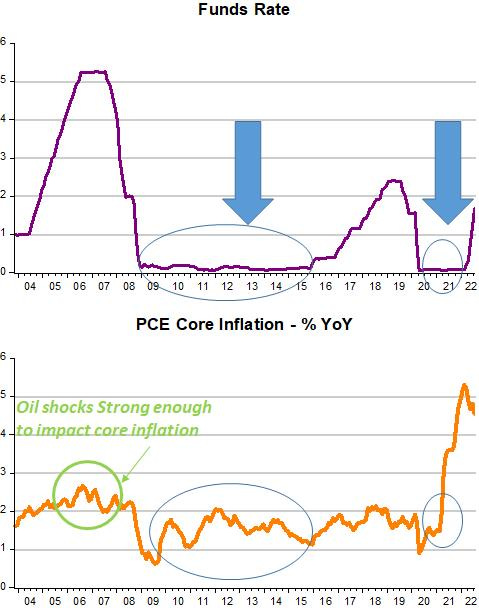

This “error” stems from the “popular” view that the stance of monetary policy is well defined by the level of the policy rate. As the chart below shows, the policy rate was close to zero from 2009 to 2015 and inflation was also very low and stable throughout, and remained so until early 2021.

According to Barro, if inflation didn´t budge for a decade despite an aggressive monetary policy after the Great Recession, the fact that inflation went up this time around must have been caused by something else, with an extraordinary fiscal expansion being the culprit!

Contrary to what Barro, and many others think, monetary policy during and after the Great Recession was not aggressively expansionary, but aggressively tight! On the other hand, after Covid-19 hit, monetary policy became aggressively expansionary!

The panel of charts below “paints the picture”.

In words, and using the “thermostat analogue” of the equation of exchange, if you look at the right hand side of the panel, you note that in early 2008 velocity began to fall (red bar). Looking up, you note that money supply remained on trend, not rising to offset the fall in velocity (the “outside temperature”). Looking at the top chart in the LHS of the panel, NGDP (the “inside temperature”) drops (bringing down with it real output).

In early 2009 (green bar) velocity begins to rise. Money supply, this time falls, thus offsetting the rise in velocity and “condemning NGDP to a lower level path. With velocity rising back to its relatively stable level and money supply evolving along a stable (but lower) path, NGDP (and RGDP) also evolved stably along a lower path (and lower associated growth rate).

Did real output “potential” really fell permanently or did “extraordinarily constrained” aggregate demand made it so? I vote for the later! Although unemployment fell monotonically throughout the next ten years while inflation remained low and stable, the “quality” of the labor force (things such as labor force participation and employment ratio were very negatively impacted.)

Moving over to the recent period, impacted by the pandemic, we observe the behavior of monetary policy is very different. Note that between the red and green bars velocity falls a little and money supply rises a little, keeping NGDP relatively stable. But when velocity tanks with the eruption of the pandemic, the “delay” in the rise in the money supply leads to a big drop in aggregate nominal spending (NGDP). The even larger fall in RGDP is explained by the negative supply shock embodied in the pandemic.

Monetary policy, this time around reacted quickly, with money supply strongly rising to offset the sudden big drop in velocity. With that, NGDP began a rapid rise back to the previous trend level. With the rise in spending, RGDP has nowhere to go but up, a different outcome to the one that resulted from monetary policy choices during and after the Great Recession!

This time around, the monetary policy response was really “aggressive”, with NGDP even climbing above the post GR trend level path. Combined with the supply restrictions (both from the effects of the pandemic on supply chains, lockdowns, among others, and war related effects) the “aggressive monetary policy response” explains the inflation observed, without any need to appeal to “new fiscal based” explanations.

In this vein, it is sad to see that the leader of the most important central bank in the world could say, last June, that:

'I think we now understand better how little we understand about inflation,' the chair divulged at the European Central Bank (ECB) Forum in Sintra, Portugal. 'This was unpredicted.'

In my last post “The Eagle has Landed”, I concluded that by not having a clear understanding of the ongoing process, Powell and the Fed could cause a lot of pain, just as by not understanding the monetary causes of the Great Recession it “condemned” the economy to a long period of “depression” (or, as Larry Summers calls it, “Secular Stagnation”).

Hey, a bit late for commenting, but here it goes. Thought to share that Isabel Schnabel, a European Central Bank policy-maker of some clout, just yesterday noted this:

"Against this backdrop, current circumstances call for responsible fiscal policy. Governments need to be clear that current budget deficits are backed by future primary surpluses, via either future higher tax rates or lower spending.

If governments do not credibly signal their commitment to responsible fiscal policies, the private sector may eventually expect that higher inflation is needed to ensure the sustainability of public debt.[16] This would be the case if high unfunded budget deficits ended up eroding the credibility of the central bank to pursue its monetary policy objectives, endangering price stability. [17]"

She explicitly linked the second paragraph (footnotes 16 & especially 17) with the FTPL.

https://www.ecb.europa.eu/press/key/date/2022/html/ecb.sp221124~fa733bc432.en.html

What fiscal theory does is recognize that government debt creates all financial assets. Sure, Divisia M4 is an improvement over the older correlations of economic activity with M2. But it's still lacking, because Divisia M4 does not take into account many assets that are now money-like, such as ETF's. Your Divisia M4 trend chart does not take account of the additional money equivalents in our economy. The fiscal theory includes everything, and that's why Cochrane's predictions are right, the Fed is not done with tightening. Creation of federal debt is the underlying cause of prices, not just creation of Divisia M4.