The Monetary Policy Tango

The Monetary Policy Tango

If you take the wrong steps, your predictions will be wide off the mark

Thirty years ago Eric Leeper wrote “The policy tango: Toward a Holistic View of Monetary and Fiscal Effects”. He was concerned about how monetary policy and fiscal policy should “dance so as not to fall off the stage”.

Here, I´m concerned about how the identity MV=PY (or, in growth form m+v=p+y) should be interpreted if the objective is to keep p+y (aggregate nominal spending, or NGDP) stable. In other words, how should m and v “dance” so as to attain that goal?

It follows directly that to keep p+y stable, m should offset changes in v. Probably the best analogy is to a thermostat. Here, m would be the “thermostat”, v the “outside temperature” and p+y (NGDP) the “inside temperature”.

In a house, we know that a well functioning thermostat keeps the inside temperature stable if it closely offsets changes in the outside temperature. If so, you won´t freeze in winter or melt in summer.

We also know that it is not the thermostat setting that determines the outside temperature, but it is the outside temperature that determines the setting of the thermostat. For instance, given the desired level of the inside temperature, if the outside temperature is stable, the thermostat will not be changing. But if the outside tempearture changes, the thermostat will also change to offset it so as to keep the inside temperature at the desired level.

I´ll only concern myself with how the monetary policy tango was “danced” in the last 15 years. The events that transpired during those years are sufficient to convince anyone of the benefits of “smooth dancing” and also of the drawbacks when there are “misteps”.

The first picture shows the “moves” in v and m over this period.

The dashed verical lines numbered 1 - 6 indicate “moments”.

Note that between lines 1 and 2, while velocity falls, money growth intially remains stable and then also falls. What do you expect happened to the “inside tempearture” (NGDP growth)? It should fall (and increasingly so).

Between lines 2 and 3, velocity increases significantly while money growth falls by much less. What should happen to NGDP growth? Since the “outside temperature” (v) increased while the “thermostat” (m) was “dialed down” by much less, the “inside temperature” (NGDP growth”) should rise.

Between lines 3 and 4, the small oscillations in the “outside temperature” (v) are closely offset” by changes in the “thermostat” (m). What do you expect happened to the “inside temperature (NGDP growth)? It should remain stable.

Before considering the post C-19 “moves”, the next picture shows that our expectations about NGDP growth from the “moves” in m and v are realized!

The “moves” so far are related to growth rates. But we are also interested in levels. Between lines 2 and 3, for example, we observe that after turning negative, NGDP growth only climbed back to a rate that was not much different from the growth rate it experienced immediately before going negative. Therefore, the drop in the level of NGDP after the “mistep” became permanent.

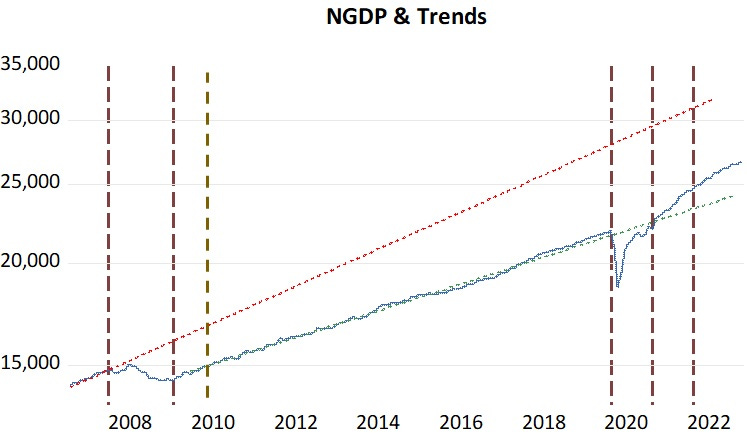

This is clearly shown in the next picture which shows the trend level path of NGDP before the monetary policy “mistep” and the one that prevailed later. Since, as shown in the first picture above, when the “outside temperature” (v) began to rise the “thermostat” (m) was dialed down somewhat, the “inside temperature” (NGDP was not allowed to rise to the previous level!

From line 3 onwards (until C-19 hit), the level of NGDP was permanently lowered and its stable growth rate was also lower (observe that the two growth trend lines are not parallel).

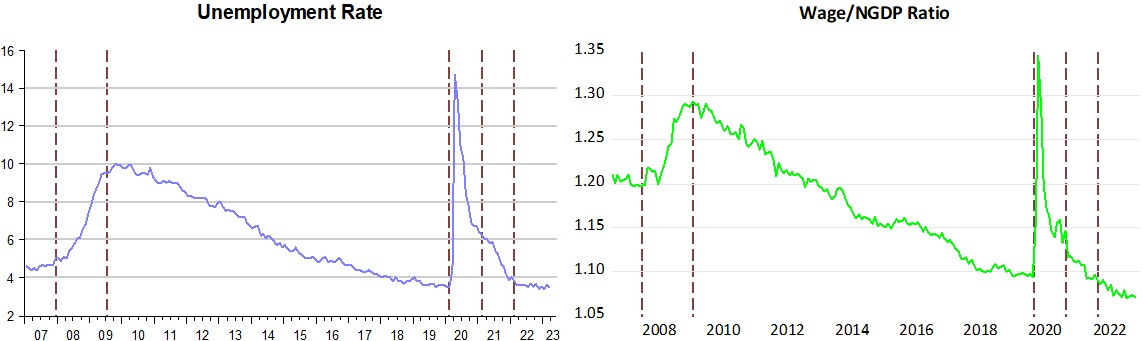

The NGDP level has important economic consequences. For example, as the next two pictures indicate, the unemployment rate is closely determined by the Wage/NGDP ratio. The intuition is that the higher the “cost of labor”, W, relative to aggregate spending (NGDP) which equals aggregate receipts, the higher unemployment will be. Also, unemployment will fall in tandem with the fall in the Wage/NGDP ratio.

A lower level of NGDP and also lower growth rate of NGDP than otherwise will imply, at each point, a higher Wage/NGDP ratio. Therefore, the fall in the unemployment rate will be slower. As counterpoint , note how fast unemployment fell after C-19, associated with a higher NGDP level and a faster NGDP growth rate!

(You can also wonder, for example, as to how a permanent lower level of NGDP impacted productivity, and thus the long term level of real output).

Now let us concentrate on the post C-19 period, starting at the vertical line 4.

The drop in the “outside temperature” (v) due to the implications of the pandemic was sudden and deep. Contrary to what happened between vertical lines 1 and 2, the “thermostat” (m) adjusted quickly to the new (and much “colder”) outside temperature.

With that, the previous level of NGDP was quickly recouped. Note that for that to happen, the growth of NGDP had to climb much higher than its previous rate to get the level of NGDP back to its trend path. This is something that did not happen in the Great Recession, condemning, as we saw, NGDP to a permanently lower path.

The next picture shows two core measures of CPI inflation. The “normal” measure and the one that additionally excludes shelter and used cars.

By the time the economy reaches vertical line 5, the NGDP level and trends picture shows that NGDP is back to its trend path. Inflation is hovering near trend and unemployment is down to a little over 6%.

To maintain nominal stability (NGDP evolving along trend), the Fed would have to bring NGDP growth back to the ~4.5% growth (the average obtained during 1992 to 2019). to keep NGDP moving along the trend path.

That, as we know, did not happen, with NGDP climbing above the trend path. That transpired because, from the first picture above, while at that point the “inside temperature”, v, began to quicly rise, the “thermostat”, m, was insuficiently adjusted down, with the result that the “inside temperature”, NGDP growth continued to rise, taking the level of NGDP above its trend path.

I know that the Fed does not pursue (or target) nominal stability (stable NGDP growth along a level trend path). It targets inflation @2%. In August 2020, the inflation targeting framework was revised to read Average Inflation Targeting (that quickly became Flexible Average Inflation Targeting (FAIT).

Where did the Fed err after both the GR and C-19? My view is that aftter the GR it was very much concerned with inflation (that´s clear from reading the transcripts of the time). In early 2021, the Fed was obsessed with its employment mandate. At the time, unemployment was a little above 6%. This is clear from reading Powell´s speech at The Economic Club of New York: “Getting Back to a Strong Labor Market”, where towards the end we read:

The revised statement emphasizes that maximum employment is a broad and inclusive goal. This change reflects our appreciation for the benefits of a strong labor market, particularly for many in low- and moderate-income communities.

Recognizing the economy's ability to sustain a robust job market without causing an unwanted increase in inflation, the statement says that our policy decisions will be informed by our "assessments of the shortfalls of employment from its maximum level" rather than by "deviations from its maximum level."12 This means that we will not tighten monetary policy solely in response to a strong labor market.

Finally, to counter the adverse economic dynamics that could ensue from declines in inflation expectations in an environment where our main policy tool is more frequently constrained, we now explicitly seek to achieve inflation that averages 2 percent over time.

This means that following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time in the service of keeping inflation expectations well anchored at our 2 percent longer-run goal.

For the previous decade inflation had averaged less than 2%, so now the Fed was concerned with the strenght of the labor market without having to worry about inflation going above 2%.

While after the GR the Fed thought it “proper”, given its inflation concerns, to keep the economy at a “cooler” temperature permanently, in early 2021 it thought it “proper”, given its labor market concerns, to keep the economy at a “warmer” temperature (and I hope also permanently, because disaster will likely ensue if it tries to bring the spending level down to the previous one).

In the first picture in this post, you will notice that after line 6 (early 2022), the “thermostat”, m, is working to bring the “inside temperature”, NGDP growth, down by more than offseting the rise in the “outside temperature”, v.

In the second picture you observe that NGDP growth is effectively coming down. When it reaches the “normal” growth rate of ~4.5%, the Fed should try to adjust the “thermostat” to keep it there, just like he managed to keep NGDP growth stable (along a lower level path) after the GR!

Picture 4 indicates that the unemployment rate has stabilized at a “low” level and picture 5 shows the “less constrained” (by remaining supply impediments (used cars) or distorted by survey methods (shelter)) elements of Core CPI inflation coming down consistently.

It appears, however, that the Fed again has done a 180 degree about face, now showing “exclusive” concern with inflation.

For example, in his latest Monetary Policy Report to Congress one week ago, Powell says:

We remain committed to bringing inflation back down to our 2 percent goal and to keeping longer-term inflation expectations well anchored. Reducing inflation is likely to require a period of below-trend growth and some softening of labor market conditions. Restoring price stability is essential to set the stage for achieving maximum employment and stable prices over the longer run.

A more “radical” statement was made earlier this month by Bill Dudley, until 2018 president of the New York Fed and Vice-Chair of the FOMC:

“Better to risk a deep economic recession,” Bill Dudley writes in Bloomberg Opinion, “than out-of-control inflation.”

The funny thing is that Powell will never admit that he (Fed) was responsible for inflation rising persistenly above target!

These non sequitors and outlandish statements are, unfortunately, quite common, both from policymakers and policy wonks.

For example:

This is Rogoff in July 2008:

Of course, today’s mess was many years in the making and there is no easy, painless exit strategy. But the need to introduce more banking discipline is yet another reason why the policymakers must refrain from excessively expansionary macroeconomic policy at this juncture and accept the slowdown that must inevitably come at the end of such an incredible boom. For most central banks, this means significantly raising interest rates to combat inflation.

And this is Rogoff a few months later, in February 2009:

Excess inflation right now would help ameliorate the problem. For that reason, it would be far better to have 5pc to 6pc inflation for a couple of years than to have 2pc to 3pc deflation,” he told the Central Banking Journal

or,

Feldstein in 2009 wrote:

The US last week showed its first signs of deflation for 55 years, prompting inevitable fears of further deflation in the future. Yet the primary reason for the negative rate of US inflation is the dramatic 30 per cent fall of commodity prices. That will not happen again [what certainty]. Moreover, excluding food and energy, consumer prices are up 1.8 per cent from a year ago. That is the good news: the outlook for the longer term is more ominous.

Hopefully, by looking back at its past performances, the Fed finally appreciates the advantages that flow from learning to Tango properly!

Based on the rate-of-change in our “means-of-payment” money supply, the May #s, there will be no recession this year.

Exceptionally good piece. Especially liked Wage/NGDP ratio.