The Fed´s Shakespearean Moment

The Fed´s Shakespearean Moment

''To cut or not to cut. That´s the question"

From the FOMC Minutes

Federal Reserve officials said they were awaiting additional evidence that inflation is cooling and were divided on how long to keep interest rates elevated at their last policy meeting.

Powell at the ECB Forum in Sintra, Portugal:

We are well aware that if we go too soon, that we can undo the good work we've done in bringing down inflation. And if we go too late, we could unnecessarily undermine the recovery and expansion."

Here I´ll argue that the risks of being late are rising fast.

The main reason the Fed risks being late is that it believes interest rates define the stance of monetary policy. As I´ll show, it doesn´t, but it can nevertheless have deleterious effects on certain areas of the economy, particularly on the housing market.

The panel below provides insights into the “inflation problem”. The LHS shows that monetary policy began to tighten in early 2022. I know that because that´s when NGDP growth (which better defines the stance of monetary policy) began to slide lower.

When NGDP growth on a YoY basis stabilized after June 2023 (vertical dotted line), inflation also stabilized (the measure of inflation is the Harmonized CPI, which excludes OER).

The RHS of the panel indicates that a more “updated” measure of NGDP growth (the 3 month moving average of the 3 month annualized growth), has been very stable since December 2023. The latest data point shows a drop in the growth rate, possibly indicating that the Fed is inadvertently tightening monetary policy.

Given the stable growth of NGDP, all measures of inflation are stable. The CPI, which has the highest weight of OER shows the highest inflation rate, followed by the PCE, which has a lower OER weight, and with the Harmonized CPI, which completely excludes OER, having “landed” on the 2% target.

With its “inflation concern”, the Fed is being “blindsided” by OER, which is a price no one pays, is inputed and lagging!

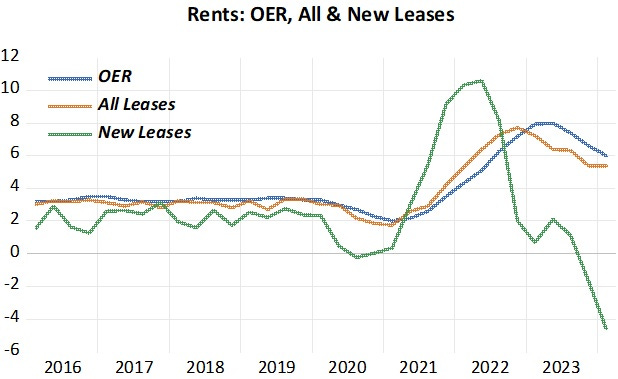

The next chart shows rents. New leases, all leases and OER. Rents (new leases) skyrocketed in much of the country during the pandemic, as Americans fled cities and sought living space. With a lag, all leases and OER began to rise.

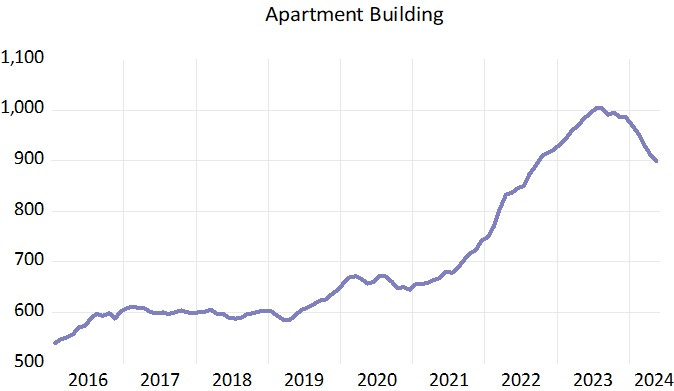

Rising rents helped fuel an apartment-building boom.

Now, new leases are falling fast, so it is to be expected that OER and All Leases will continue to fall, which will move both PCE and CPI inflation towards the 2% target.

From the arguments so far, it could be argued that the Fed is prevaricating with respect to cutting rates. That´s not the sort of behavior one should expect from such an important institution as the Fed.

If NGDP growth is showing that monetary policy is adequate, with inflation stable (and on the verge of transitioning to target), the labor market so far remaining strong as is real growth, what is being negatively affected by excessively high interest rate (that could spillover to other parts of the economy)?

The most likely candidadte is the housing market. The charts show that as soon as interest rates began to rise (first vertical dotted line), residential investment stopped rising and began to fall, while residential construction employment flattened. When interest rates stopped rising (second dotted line), both residential investment and employment rose timidly.

From this discussion, I conclude that the Fed is in greater risk of committing the “type two error” or, as Powell said: “if we go too late, we could unnecessarily undermine the recovery and expansion.”

You want to ask an economist, not a banker. Where does money come from?

What economists are is stupid. I've picked almost every top and bottom (except initially QE2) in history. Banks don't lend deposits period. Japan is a perfect example.