The Fed´s monetary policy from the "pandemic get-go"

The Fed´s monetary policy from the "pandemic get-go"

If only the Fed "prayed on the NGDP level target altar", instead of the "boos" we hear, the applause would be deafening!

You might think this is very lucid introduction (especially from someone who´s advocating NGDP targeting):

“Suddenly the Federal Reserve seems to agree with critics who say its efforts to control inflation have come too late. Its delay has given inflation longer to get entrenched, and now that the Fed is hurrying to catch up, investors are having to shift their assumptions abruptly. Both factors complicate the central bank’s job, making it harder to curb inflation without tipping the economy into a recession.”

It isn´t, by a long mile. When you say: “its efforts to control inflation have come too late…” it´s as if the Fed got caught by surprise, with inflation suddenly coming out of left field!

This pandemic-induced cycle was from the get go going to prove difficult to understand and analyze. The main reason is that, contrary to most cycles (and the 2007-09 one is a clear (in spite of all the obfuscations) example), the present one was not Fed-induced.

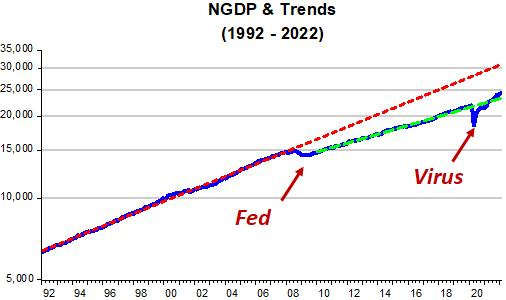

For the past 30 years, for which I have monthly data for NGDP (and RGDP), there were two long periods of “tranquility”; from 1992 to 2007 and from 2010 to 2019. The first was interrupted by the “Great Recession”, and the second by the Covid-19 pandemic. While the first interruption was “Fed-made”, the second resulted from a “knock-down” by “the virus”.

By period of “tranquility”, I mean the economy experienced nominal stability, or stable and steady growth in aggregate nominal spending (NGDP). The point of departure of the analysis is the equation of exchange M*V=P*Y, an identity that says that money supply (M) times its velocity (V) equals price (P) times real output (Y).

When you impose assumptions (or restrictions) on this equation, the most “popular” being that velocity is stable, writing the equation in growth form (where lower case letters represent the growth of the corresponding capital letter) we get (if V “constant”, its growth rate, v, equals zero);

m-y=p

which “translates” into the “meme” “inflation results from too much money chasing too few goods”. But V, unfortunately, is stable only until it isn´t, and when that happens the “meme” becomes invalid and the equation of exchange tells us that to keep NGDP (P*Y, or p+y) on its stable level trend path, the change in M (or m) has to be such as to offset changes in V (or v).

This approach to the equation of exchange has been named “Friedman´s Thermostat”.

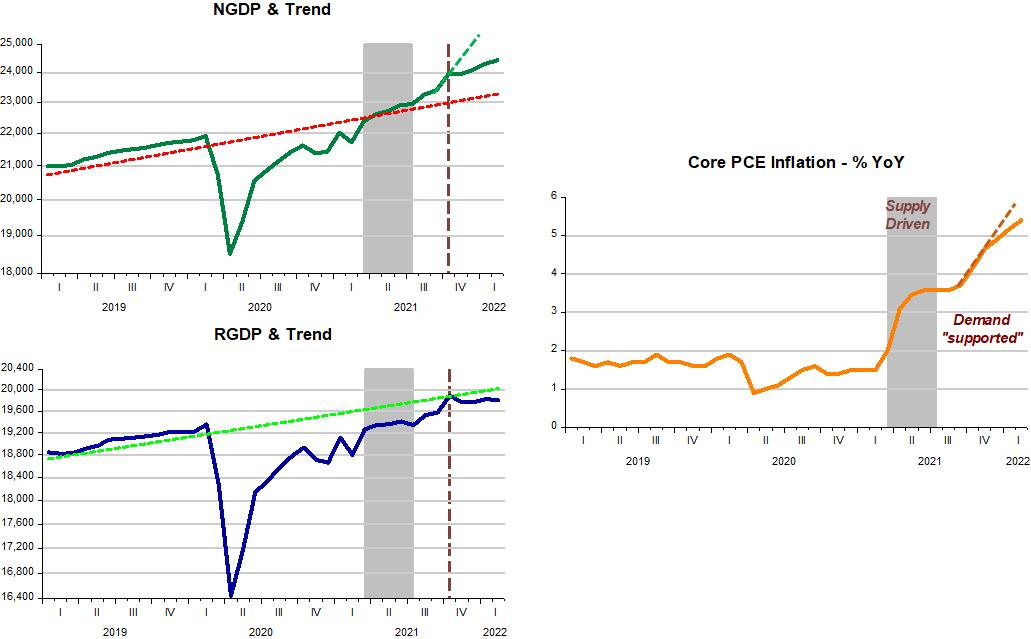

The chart below shows how NGDP evolved over the past 30 years. The two periods of “tranquility” are evident. Following the first interruption in the GR, NGDP evolved again stably but along a significantly lower path (a.k.a. “Depressed Moderation”).

Different from what happened after the GR, after the “virus” knock-down, NGDP quickly went back to “post GR trend path”.

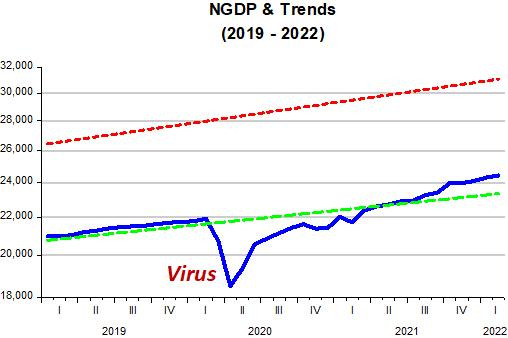

The next chart zooms-in to the recent period, showing that just 13 months after tanking, NGDP was back on its trend path (soon after the Fed went “overboard”, but more on this later).

What gave way to these two very different results for the behavior of NGDP after the two shocks?

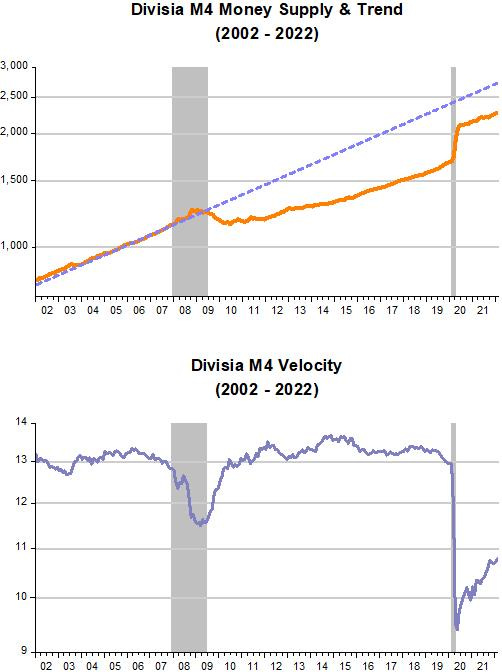

The “Thermostat” interpretation of the equation of exchange elucidates. The period is shorter (2002 - 2022) so as to make things more clear.

Note that velocity was relatively stable before and after the GR up to the “virus attack”. Money supply was rising steadily and so NGDP was also rising steadily in both periods, resulting in “tranquility” (which translated into low/stable inflation and stable RGDP growth, not shown but believe me).

When the GR came along, velocity declined significantly; however, money supply did not increase to offset it, so NGDP tumbled. When velocity climbed back to its stable level, money supply fell, “condemning” NGDP to remain lower. Thereafter, money supply rose steadily which, combined with velocity remaining stable at the previous level, kept NGDP on a stable rising path, i.e. “tranquility 2.0” (or “depressed Great Moderation”).

In early 2020, the virus attacked. This was a supply shock, over which the Fed has no control. The demand shock that went together was the result of the deep & abrupt fall in velocity. The demand side of the shock was much stronger than the accompanying supply shock, leading to a deep drop in NGDP (and RGDP) together with a smaller fall in inflation.

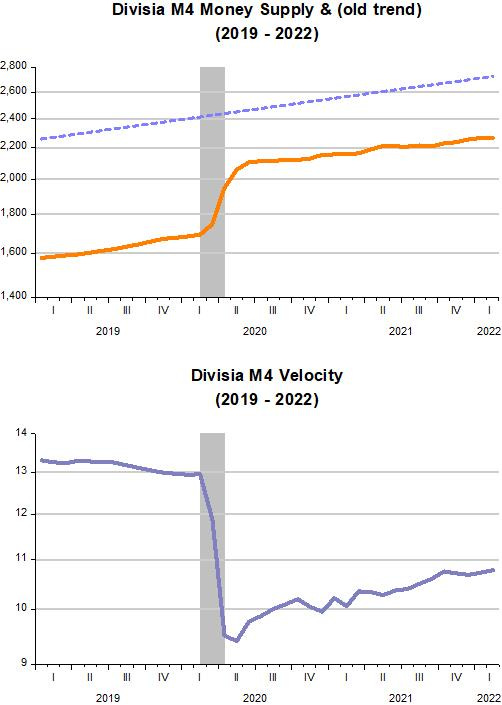

This time around, the Fed reacted quickly “dialing the thermostat” to “warm up” the “inside temperature” (NGDP). The zoom-in of the previous charts illustrates.

The Fed acted appropriately when the virus attacked. That was not what many pundits and commentators thought. Already in Spring and early summer of 2020, many were “shocked” by the record growth in the money supply. Since the growth in money supply was what was needed, the basis for the dire inflation predictions was clearly wrong. Imagine the depth and duration of the recession that would have taken place if the Fed “listened” to those critics!

In fact, the recession ended up being the shortest on record and the recovery also the fastest, especially given the depth of the fall!

In my last post “The “definitive” breakdown of inflation”, I showed the chart below, pointing out where the Fed made a mistake.

It happened when the Fed allowed NGDP to climb above the trend path. The first increase in inflation was the result of the supply shocks, that kept RGDP below the trend level. That was the “unavoidable” inflation, consistent with maintaining nominal stability.

Imagine if the Fed was level targeting NGDP. It would have mostly avoided going above that path and inflation would not have increased due to this “demand component”.

Therefore, the view that “Suddenly the Federal Reserve seems to agree with critics who say its efforts to control inflation have come too late", is clearly wrong. The increase in inflation above the supply driven (unavoidable) inflation only came about because the Fed was erroneously expansionary after mid-2021!

In a tweeter comment to my last post (linked above)@frances_coppola wrote it could be summarized as “don´t panic”.

I hope that the Powell Fed does not “panic”, but takes responsibility for the “excess inflation” that has materialized, and acts to bring it down in a “gentle” (or recession avoiding) fashion.

It´s interesting to note that on previous occasions Fed members tried to avoid responsibility for the outcomes of their actions. Two examples, one from long ago and a more recent one illustrate:

Consider the following quotation from the minutes of a November 1937 Fed meeting, some months after the economy went into recession in the middle of the depression:

We all know how it developed. There was a feeling last spring that things were going pretty fast… If action is taken now it will be rationalized that, in the event of recovery, the action was what was needed and the System [Fed] was the cause of the downturn. It makes a bad record and confused thinking. … I would rather not muddy the record with action that might be misinterpreted.

And this one by Tim Geithner in September 2008:

The argument that makes me most uncomfortable here around the table today is the suggestion several of you have made—I’m not sure you meant it this way—which is that the actions by this Committee contributed to the erosion of confidence—a deeply unfair suggestion.

… But please be very careful, certainly outside this room, about adding to the perception that the actions by this body were a substantial contributor to the erosion in confidence.

Note: I use the broad money defined by the Divisia M4 index. That´s not the usual one, with (simple sum) aggregates like M2 being the usual monetary statistic used in most analyses. The reason (and advantages) of using Divisia M4 were presented here.

Very nice analysis. BTW, there's no link in the final sentence to an explanation for why you used M4 to define broad money.

Excellent analysis. One wonders, assuming that Fed reduces excess demand in an optimum way, how long will the supply issues persist..