The Fed does not believe in money

The Fed does not believe in money

Powell "cancels" money

I think it is “terrifying” that money, the raw material of monetary policy, is being “sidelined”.

Powell in an exchange with Senator John Kennedy during the February 2021 Senate hearings:

Senator Kennedy: (01:18:14)

Let me stop you, Mr. Chairman, because I’m going to have one last question quickly. M2, the money supply is up. I think about $4 trillion over the past year, or $6 trillion. $4 trillion, $6 trillion, what’s a few trillion? It’s up 26%, the highest amounts since 1943. What does that tell you?Jerome Powell: (01:18:35)

Well, when you and I studied economics a million years ago, that M2 and monetary aggregates generally seem to have a relationship to economic growth. Right now, I would say the growth of M2, which is quite substantial, doesn’t really have important implications for the economic outlook. M2 was removed some years ago from the standard list of leading indicators, and just that classic relationship between monetary aggregates and economic growth in the size of the economy, it just no longer holds. We’ve had big growth of monetary aggregates at various times without inflation, so something we have to unlearn, I guess.

Soon the Fed may get rid of any and all monetary aggregates. On March 2006, it got rid of M3:

M3 does not appear to convey any additional information about economic activity that is not already embodied in M2 and has not played a role in the monetary policy process for many years. Consequently, the Board judged that the costs of collecting the underlying data and publishing M3 outweigh the benefits

In recent weeks, Federal Reserve monetary data took another step backward?

“Savings deposits” and “other checkable deposits” are now lumped together. Worse, bank deposits are now reported monthly rather than weekly and with a long lag.

So, as the world becomes filled with more granular data and government agencies request ever greater quantities of data from banks and nonbank financial institutions, the Federal Reserve is moving in the opposite direction with its own reporting.

The Fed has also discontinued the release of MZM (Money Zero Maturity), a broader aggregate than M2, that includes money market funds.

It really appears that Money is something that we really have to unlearn, so we´ll stop polluting peoples minds with that “vile data”!

Unfortunately, if that happens the Fed will be in the high seas, in a storm, and without a compass!

Powell and the Fed now only care about the number of people working and how to get it higher, not about an age-old statistic (the unemployment rate) that, for all its familiarity, overlooks a key group, namely those who stopped looking for work during the pandemic and need to be brought back.

That´s true. In the last quarter of 2000, for example, the unemployment rate was 3.9%, not much different from the 3.6% in the last quarter of 2019, before the pandemic hit. Nevertheless, while the participation rate at the end of 2000 was 67%, it was a significantly lower 63.2% at the end of 2019.

On the other hand, while the employment population ratio was 64.3% at the end of 2000, it was only 61% at the end of 2019. With those facts, there´s no doubt that the 3.9% rate of unemployment in 2000 reflected a much better labor market than the lower 3.6% rate observed at the end of 2019.

With the onset of the pandemic, labor force participation fell to 60.8% in the second quarter of 2020, before rising to 61.4 in the first quarter of this year. Meanwhile, the employment population ratio fell to 52.9% in the second quarter of 2020, rising to 57.4% in the first quarter of 2021.

How are these different labor markets related to monetary policy? In my view, the stance of monetary policy is not gauged by interest rates but by the behavior of aggregate nominal spending (NGDP) growth. In that sense, monetary policy is “expansionary” if NGDP growth is trending up. It is “contractionary, if NGDP growth is trending down. If NGDP growth is stable, we can say monetary policy has achieved “Nominal Stability”.

As I´ll show, the Level path along which nominal stability is obtained matters. In fact it is the difference in level paths that determine the overall strength of the labor market, beyond just what is indicated by the level of the unemployment rate.

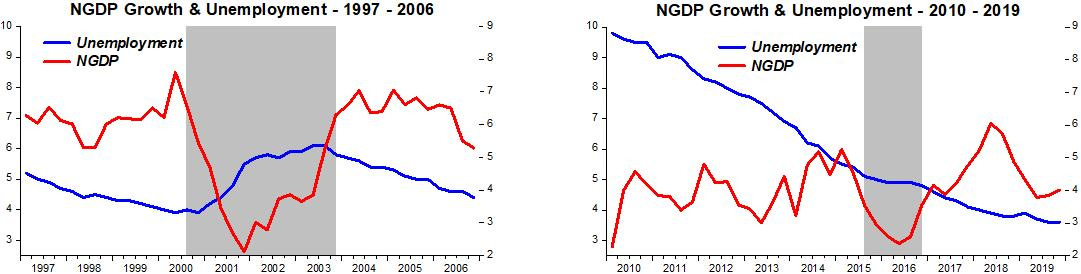

I examine two periods. The 10 years from 1997 to 2006 that preceded the “Great Recession”, and the 10 years from 2010 to 2019, that followed the “Great Recession”.

The two charts below have the same scales for ease of comparison, and show the connection between NGDP growth & unemployment. When NGDP growth is stable, unemployment stays on a downward trend. When NGDP growth falls (shaded areas) unemployment rises or, as during the most recent 10 years, stops falling. The difference in outcomes is related to the magnitude of the NGDP growth fall, much bigger in 2001-03 than in 2014-15.

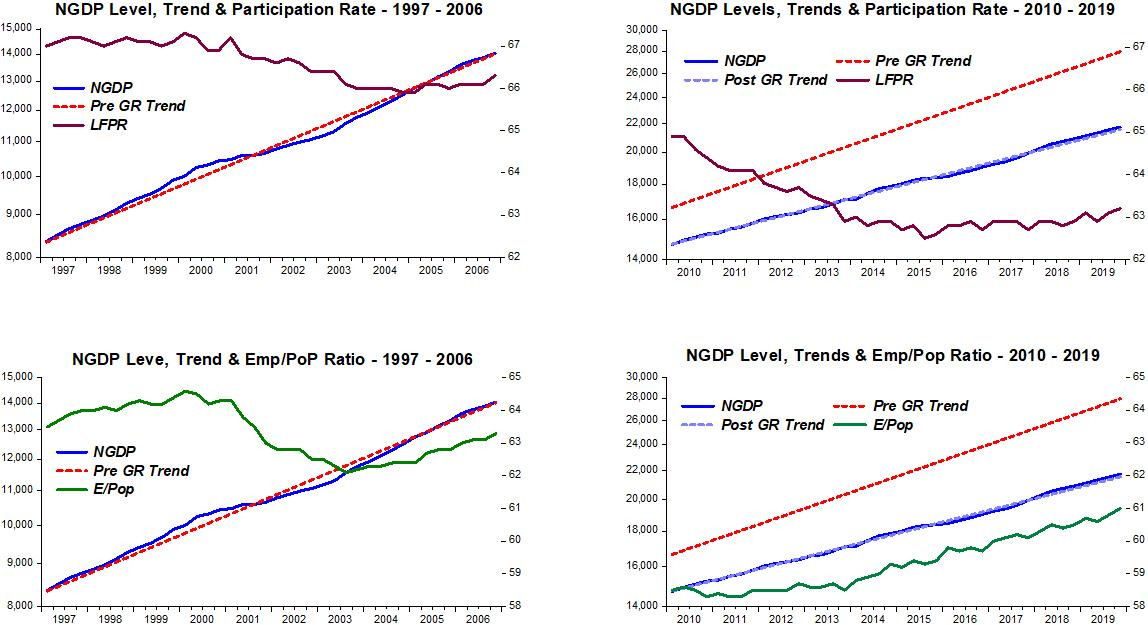

The determinants of the unemployment rate, that also define the “quality” of the labor market, are the employment population ratio (E/PoP) and the labor force participation rate (LFPR). Although the rate of NGDP growth has some influence, those quantities are more closely tied to the Level of economic activity, or to the Level Path followed by NGDP.

The charts below show this, relating the NGDP trend level to both the LFPR and E/PoP. In each chart the scale for the LFPR is the same. That is also the case for the charts relating E/PoP and the trend level NGDP path.

In the charts for 1997-06, the drop in the E/Pop in the 2001 recession may be reflecting some structural, maybe demographic, changes. Nevertheless, when NGDP goes back to trend, the E/PoP ratio begins to rise.

The impact of the drop in level is clear in the post GR period. After the drop in the NGDP level (that has a counterpart in the level of real output), NGDP growth remains stable. The E/PoP ratio soon begins to rise very slowly, but the LFPR appears to have been permanently affected. It is the combination of a slowly rising E/PoP and low but stable LFPR that gives rise to the falling rate of unemployment.

My takeaway is that if the level of economic activity does not rise above the trend path observed after the GR, unemployment would likely remain low, but the labor market would nevertheless remain week, with low LFPR and E/PoP (and obviously, minority groups would suffer more).

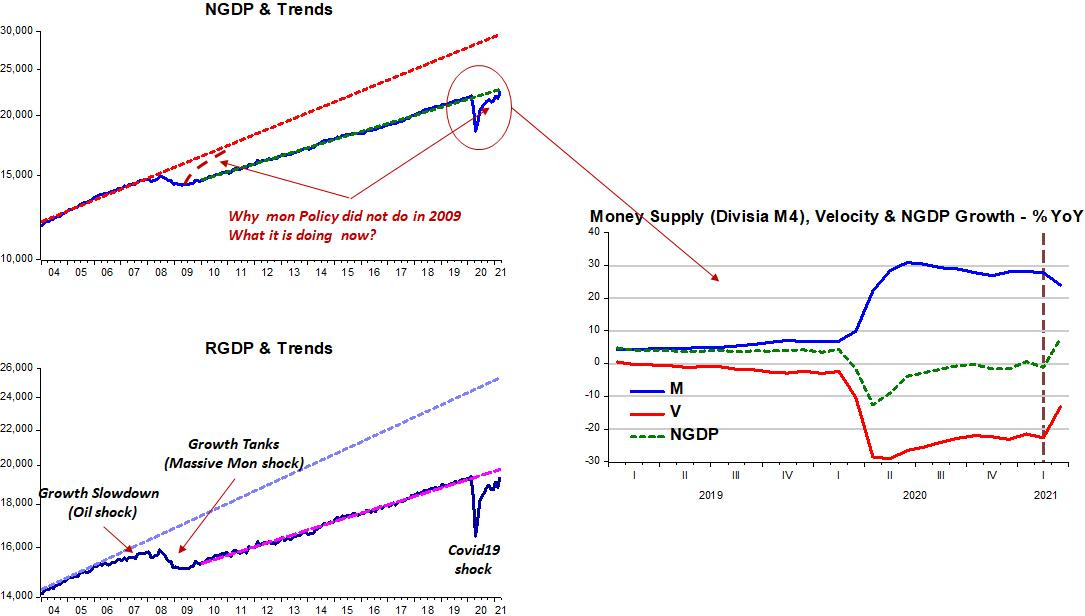

The next chart summarizes the past and shows the situation at present. The data used in the charts are monthly NGDP & RGDP data from Macroeconomic Advisers (now IHSMarkit) and Divisia Monetary Indices from the Center for Financial Stability

To the question, “why monetary policy did not do in 2009 what it is doing now (i.e. taking NGDP back to the trend path it was on before the Covid19 shock), the answer is easy:

The GR was the result of a massive monetary policy error, but the Fed never recognized (at least publicly) it erred. this is clear in statements from Bernanke (Fed chair) in the September 2008 FOMC Meeting (which took place right after Lehmann imploded) and from Tim Geithner, in the October FOMC Meeting:

Ben Bernanke on September 16 2008 24 hrs after Lehamn (pages 77 78)

As I said, I think our aggressive(!) approach earlier in the year is looking pretty good(!), particularly as inflation pressures have seemed to moderate.

Overall I believe that our current funds rate setting is appropriate, and I don’t really see any reason to change.

On the one hand, I think it would be inappropriate to increase rates at this point. It is simply premature. We don’t have enough information. There is not enough pressure on inflation at this juncture to do that. On the other hand, cutting rates would be a very big step that would send a very strong signal about our views on the economy and about our intentions going forward, and I think we should view that step as a very discrete thing rather than as a 25 basis point kind of thing.

We should be very certain about that change before we undertake it because I would be concerned, for example, about the implications for the dollar, commodity prices, and the like. So it is a step we should take only if we are very confident that that is the direction in which we want to go.

And Tim Geithner on October 2008 (page 144):

I just want to make a couple of other points. I think the only way to be predictable in a crisis like this is to be predictably inert or to be late. I don’t understand the basic argument that you add to confidence by being inert or by being late or, as the Chairman said, by being passive despite overwhelming evidence about changes in the outlook and risks to financial stability

The argument that makes me most uncomfortable here around the table today is the suggestion several of you have made—I’m not sure you meant it this way—which is that the actions by this Committee contributed to the erosion of confidence—a deeply unfair suggestion.

… But please be very careful, certainly outside this room, about adding to the perception that the actions by this body were a substantial contributor to the erosion in confidence.

This time around, there was no monetary policy error, so the Fed felt “free” to take corrective actions. If Powell thinks it is the setting of the policy rate that is driving monetary policy, he´s in for a unpleasant surprise. In the right hand side chart, the big jump in NGDP growth in March (from 0% to 8% YoY) was the result of velocity rising and money supply growth falling by much less. This has taken NGDP to very close to the trend path it was on before the Covid19 hit.

Yesterday, Yellen, although now Treasury Secretary, cannot get rid of her “overheating - inflation” mindset, caused a temporary ruckus:

“It may be that interest rates will have to rise somewhat to make sure our economy does not overheat, even though the additional spending is relatively small relative to the size of the economy,” Yellen said. “It could cause some very modest increases in interest rates to get that reallocation.”

To make significant and lasting improvements in the labor market, Powell and the Fed must revert to putting back money in monetary policy. Just as (by chance) the Fed was able to keep NGDP growth on a stable path both before and after the GR (although at markedly different level paths), now it has to choose where it wants to place NGDP. Just keeping NGDP growing along the post GR trend will not improve the labor market situation. It will have to go above that level.

And the quicker Powell puts money (preferably the broadest definition of money like Divisia M4) back into monetary policy, the better he will be able to control the transition and minimize the worries about “overheating” & “inflation”.