The Fed & War

The Fed & War

Not quite rid of the pandemic, another S shock comes along to tax the Fed

How unlucky is Jay Powell? Two back to back big shocks rocked his boat! Different from 14 years ago, when his predecessor Ben Bernanke was the major force behind the 2008 crisis, Powell is an “innocent bystander” to the crises that intruded during his tenure.

The first shock - Covid19 - was both a demand and a supply shock. Initially, the demand (velocity) shock was much stronger than the supply shock. We know that because both real output and inflation fell. The recession was very deep but also very short (just two months from peak to trough). That happened because monetary policy reacted very quickly, with money supply growth rising steeply to accommodate the rise in money demand (fall in velocity).

By April 20, at the trough of the recession, broad money (Divisia M4) was rising 22% YoY, which was double the highest rate of broad money growth witnessed during the inflationary 1970s!. No wonder that it was then that warnings of an imminent inflation explosion began to appear.

That “high” rate of money growth was sufficient to brake the fall in economic activity, but to pull the economy back up, money growth had to keep rising. It did, and by June 20, broad money growth peaked at 30% YoY. By then, what I called “One-legged monetarists” were having a fit!

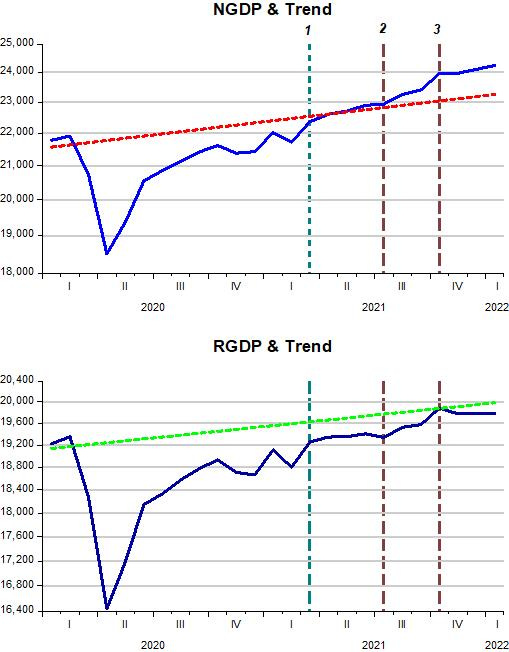

The charts below provide a clear illustration of Powell´s Fed actions since the February 2020 peak in economics activity.

The Fed quickly moved to offset the demand (velocity) shock that tanked nominal spending (NGDP) and real economic activity (RGDP). By March 2021 (bar 1), the Fed had put nominal spending back on the pre-pandemic (post GR) trend path. And NGDP remained on that trend path for the next few months, until July 21 (bar 2).

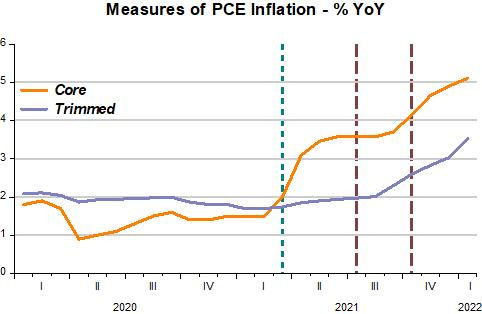

Note that RGDP was still below its pre pandemic trend level path, remaining quite stable during the next few months. At that point (March 21, bar 1), the supply constraints became binding. Although NGDP was rising along the trend path, some measures of inflation began to rise. However, with NGDP rising along trend (a state of nominal stability), inflation “levelled-off”.

Lesson 1: The best the Fed can do when confronted with a supply shock is to keep nominal spending growth stable (nominal stability). If it “tightens” because of the increase in inflation that inevitably occurs, it will impart instability to the system and likely bring forth a recession.

For some reason, in July 21 (bar 2) the Fed “tipped its hand”, allowing NGDP to climb above the pre pandemic trend. This was the Fed´s first mistake since the start of the pandemic. RGDP climbed to trend, but inflation soon increased again. I like to think that was the point when monetary policy became expansionary, with excess demand the factor driving inflation.

After October 21 (bar 3) the Fed´s “hand levelled off” again. This was a “partial correction” of its July 21 mistake and bode well for the scenario going forward, which I discussed here. After that, in late February 22, the second supply shock hit with the invasion of Ukraine by Russia and the economic consequences it has so far entailed.

I evoke Lesson 1 above. The best the Fed can do, no matter how “massive” the supply shock becomes, is to keep NGDP stable. Since NGDP is above the pre pandemic trend path, this means keeping NGDP “constant” close to the present 24 trillion dollar level, at least until it hits the trend path sometime in the first half of 2023!

In order to keep NGDP “constant”, the Fed will have to very closely offset changes in velocity. When, until recently, we could expect that velocity would rise with the waning of the pandemic, now it could fall again due to the uncertainties brought forward by geopolitical events.

In short, the Powell Fed is facing and will continue to face big challenges. It´s not as simple as Krugman puts it. According to him:

Finally, what impact will the Ukraine war have on economic policy? Spiking oil and food prices will raise the rate of inflation, which is already uncomfortably high. Will the Federal Reserve respond by raising interest rates, hitting economic growth?

Probably not. The Fed has long focused not on “headline” inflation but on “core” inflation, which excludes volatile food and energy prices — a focus that has stood it in good stead in the past. So the Putin shock is exactly the kind of event that the Fed would normally ignore. And for what it’s worth, investors appear to believe that it will do just that: Market expectations of Fed policy over the next few months don’t seem to have changed at all.

In 2008, for instance, Bernanke focused on headline inflation. It was a disaster. If he had focused on Core, the disaster might have been mitigated, but would still have been significant. As George Selgin succinctly puts it:

The sole merit of "core" inflation is that it leaves out prices of some goods most subject to supply innovations (or "shocks"). But this is really a crude, and fundamentally flawed, way of doing what would be better done by targeting NGDP instead of any inflation measure.

One thing is maybe clear. If Powell successfully navigates the storms ahead, he will be “hailed”. After all, with all the “disasters” Bernanke “promoted”, he was hailed “The Hero” by The Atlantic and got named “Man of the Year” by time magazine!