The economy "play" in 4 "acts"

The economy "play" in 4 "acts"

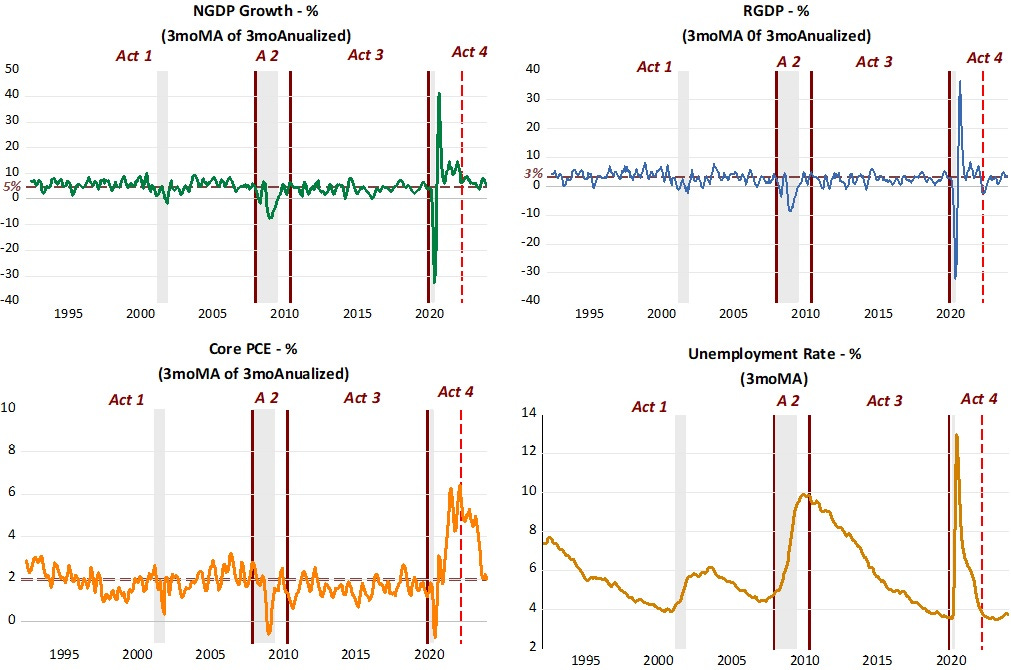

Act 1: The Great Moderation; Act 2: The Great Recession; Act 3: The Depressed Moderation; Act 4: The C-19 Cycle

Te “actors” in the play are, in order of apperance:

Aggregate Nominal Spending (NGDP) growth

Real Output (RGDP) growth

Inflation (the core PCE)

Unemployment

The play also contemplated using a band, collectively known as FOMC to provide some musical background. During “rehearsals”, however, they were so “off-key and noisy” that the producers though best to leave them out of the “play”.

The costume designer thought it best to dress up the actors in “smoothed clothes” so as to minimize the noise observed when they acted in their raw state. The “smoothed” clothes chosen was the three month moving average of the three months annualized growth rate, except for the unemployment “actor”, who just gets the three month moving average “coat”.

Panel 1 below shows the actors´performance for the whole play (4 acts). An analogy to Bethhoven´s 6th symphony (Pastoral); Act 1 would be “sea of tranquility”, Act 2 “stormy weather”, Act 3 “subdued tranquility after the storm” and Act 4 “tempest, wind & lightening”.

I´ll concentrate the analysis of the play to Act 4. Act 4 seems very different from the other Acts, leading many to be confused and trying to compare it to “long ago plays”.

Our “leading actor” is the smoothed growth of NGDP (or aggregate nominal spending). The 5% growth is the average growth of NGD during Act 1. During Act 2, this growth rate falls significantly and never fully recovers, with NGDP growth during Act 3 being more subdued.

The behavior of the other actors during Acts 1 - 3, reflect the behavior of the leading actor, with real growth falling below the 3% rate observed during act 1, inflation falling below the 2% rate of Act 1 and unemployment falling slowly after being hit by “stormy weather”.

The next panel details Act 4.

I added some “subtitles” to the “plot” to make it easier to follow. The C-19 shock was surprising and “one of a kind”, which makes the 4th Act very different from the others.

Initially, every “actor” tumbles except unemployment, which shoots up. Analysts of the 4th Act pay a lot of attention to the inflation “co-star”, attributing its rise mostly to supply constraints associated with C-19.

My analysis indicates that the rise in inflation was mostly due to increased nominal spending growth which generated “excess demand”, with supply constraints playing at most a “supporting role”. Additional evidence for this is that real output growth was also up, with unemployment “naturally” decreasing.

By the time the FOMC began the process of rate hikes, “excess demand” had essentially been eliminated and inflation had peaked. Real output growth fell in early 2022 as a result of the negative real shock from the War in Ukraine.

Thereafter, NGDP growth remains very close to its Act 1 rate of 5%, real output growth recovers, remaining close to its Act 1 rate of 3% and unemployment stays low and stable.

Inflation initially falls slowly, but the pace of decrease rises once supply constraints lose importance. “Smoothed” inflation is now also down to the Act 1 rate of 2%.

I left the “FOMC band” out of the play because, especially in Act 4, it has been doing the right thing but is unaware of this, which makes the “Band” dangerous, in the sense that it may easily do something wrong!