The Economist asks: “Has the pandemic shown inflation to be a fiscal phenomenon”?

The Economist asks: “Has the pandemic shown inflation to be a fiscal phenomenon”?

"A decade of QE did not cause much inflation. Fiscal stimulus has sent it soaring"

In the Dec 18, 2021 issue of The Economist we read:

Here is a potted history of recent economic policy and inflation. In the 2010s central banks created vast amounts of money through their quantitative-easing (qe) schemes, while governments enacted fiscal austerity. Inflation in the rich world was mostly too low, undershooting central banks’ targets. Then the pandemic struck. There was plenty more qe.

But the truly novel economic policy was the $10.8trn in fiscal stimulus implemented worldwide, equivalent to 10% of global gdp. The result was high inflation. The rich country that has splurged the most, America, has had the most inflation. With consumer prices rising at an annual pace of 6.8%, the Federal Reserve on December 15th was forced to acknowledge that inflation had become a big threat.

At first glance, this apparent supremacy of fiscal policy is awkward for the fans of Milton Friedman´s view that inflation is “always and everywhere a monetary phenomenon”. But does the experience of the pandemic show that inflation is really fiscal?

Before “shooting down” The Economist arguments, to set the stage I go back a decade and look at what was called “fiscal cliff”. The view, then, did not mention inflation (which was already low), but worried about its effects on growth and unemployment.

The “fiscal cliff”:

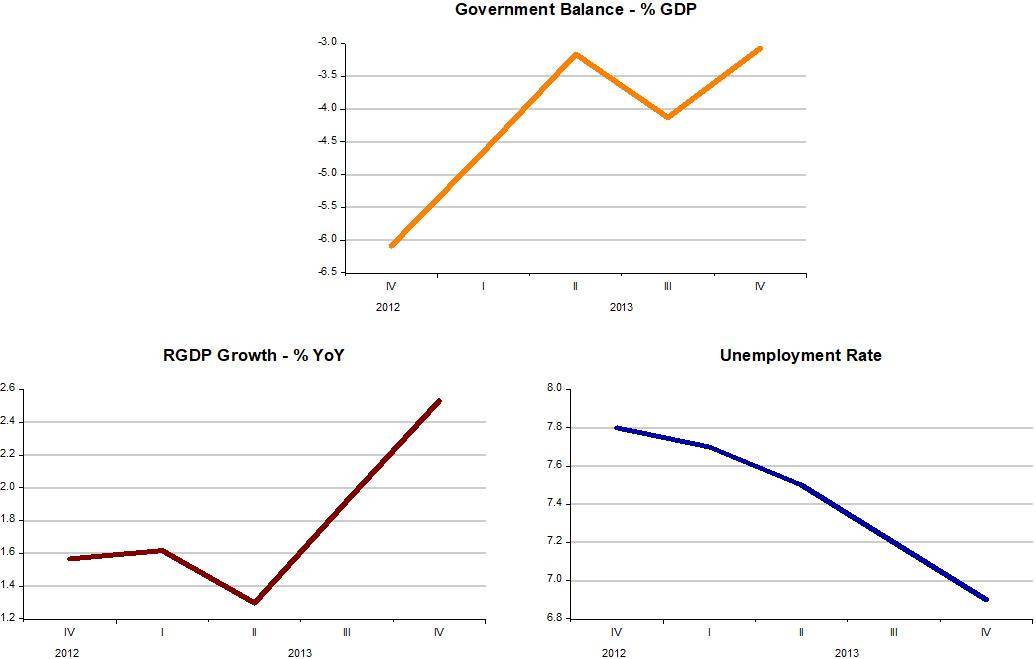

In late February 2012, Ben Bernanke, chairman of the U.S. Federal Reserve, popularized the term "fiscal cliff" for the upcoming reduction in the deficit. Before the House Financial Services Committee he described that "a massive fiscal cliff of large spending cuts and tax increases" would take place on January 1, 2013

The fiscal cliff would have increased tax rates and decreased government spending through sequestration. This would lead to an operating deficit (the amount by which government spending exceeds its revenue) that was projected to be reduced by roughly half in 2013. The previously-enacted laws causing the fiscal cliff were projected to produce a 19.63% increase in revenue and a 0.25% reduction in spending between fiscal years 2012 to 2013. The Congressional Budget Office (CBO) had estimated that the fiscal cliff would have likely caused a mild recession with higher unemployment in 2013.

The deficit was in fact reduced by half. However, real growth picked up and unemployment fell in 2013!

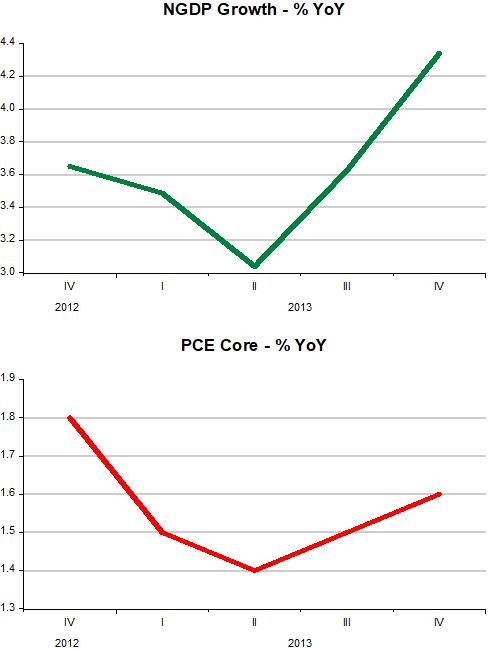

Why did this happen? With the “fiscal cliff” in place, monetary policy quickly became expansionary (i.e. the “thermostat was dialed-up”), so that NGDP growth rises. At that point, real growth turns up, unemployment continues to fall and inflation picks up. The figures illustrate.

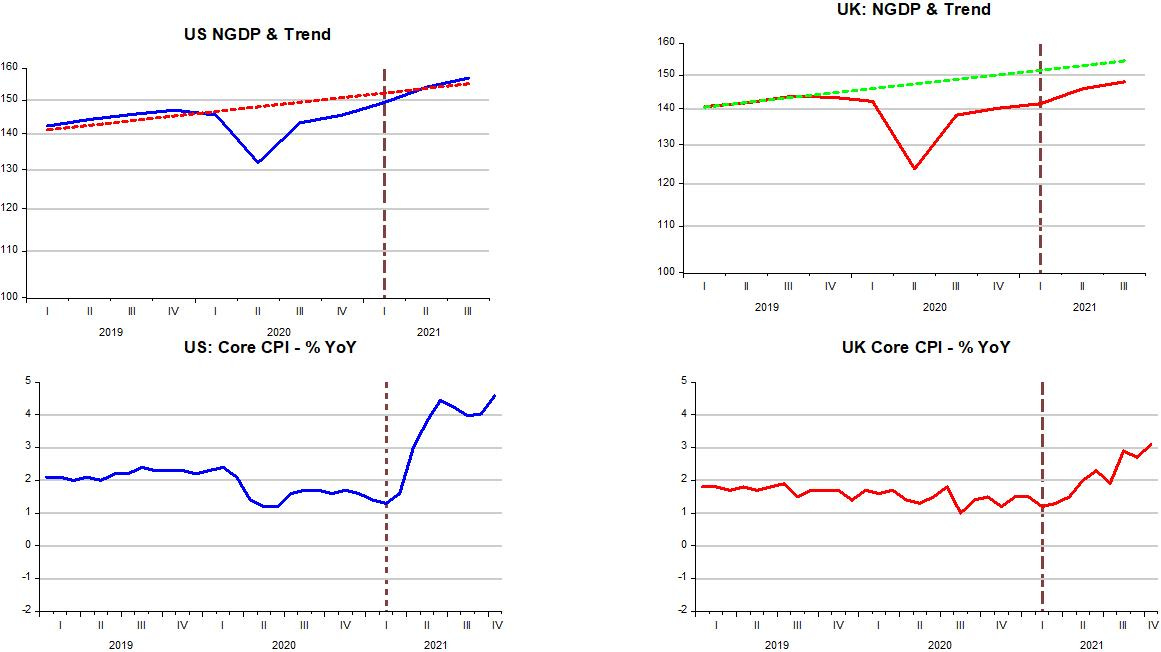

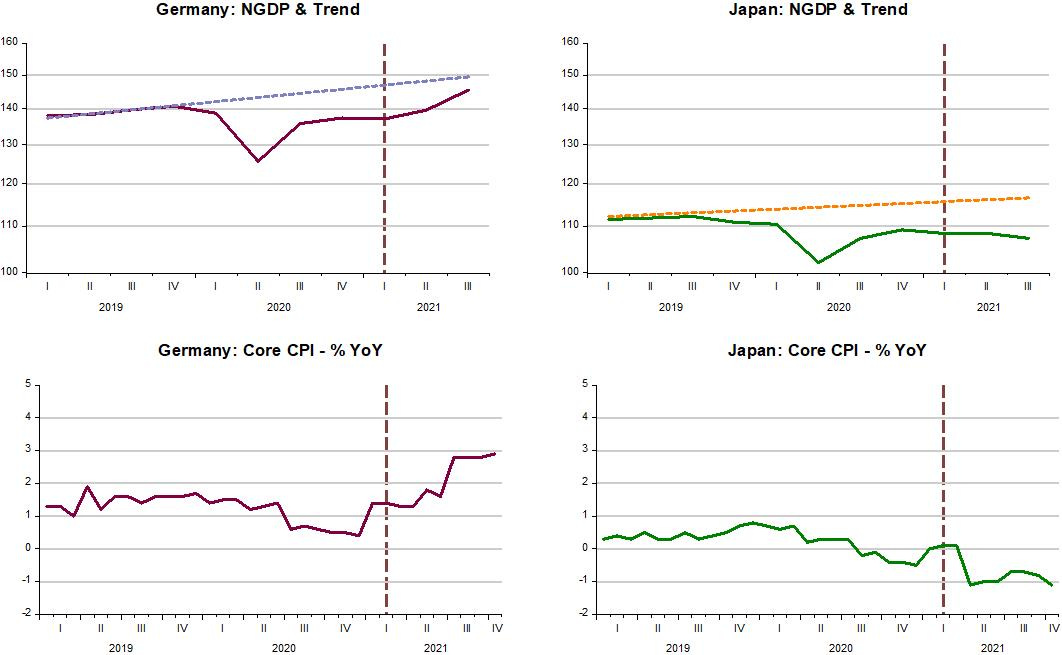

Back to The Economist. According to this survey of G20 countries Covi19-related fiscal “stimulus” (maybe “relief” would be a better description) as of May 2021, the US was not the rich country “that splurged the most”. Japan beats the US hands down. Of the countries that I analyze below (US, Germany, UK and Japan), the US only “splurged” more than the UK.

If fiscal stimulus was responsible for “soaring” inflation, Japan was the exception to the rule, because inflation there dropped to -1%!

Although the example of Japan would be enough to debunk The Economist´s arguments, I´ll go further and show that inflation continues to be everywhere a monetary (policy) phenomenon.

What we see in the panels below is that inflation is highest in the countries where monetary policy was more expansionary.

As I have argued for long, NGDP growth is the best indicator of the stance of monetary policy. The US conducted monetary policy in order to take nominal aggregate spending (NGDP) back to the trend level that prevailed during 2010 - 2019, before the pandemic hit.

In the UK and Germany monetary policy, although recently more expansionary, allowing NGDP to rise, has not been expansionary enough to take NGDP back to trend. With monetary policy very similarly expansionary in the UK and Germany, inflation in those two countries are also very similar.

Japan “clinches” the argument, being the only country in the sample that has tightened monetary policy, with NGDP dropping. No surprise, then, that inflation in Japan has fallen, despite all the fiscal “splurge”!