The coming transitory inflation

Will be the outcome of a monetary policy that strives for a better economy

Yesterday I put “foot in mouth” when I tweeted the chart below.

And writing that the “price level is still far below the pre GR trend path”. With that I was “chastised” by George Selgin, who wrote:

It's absurd to suggest that the Fed needs to return to that long-defunct trend level! Inflation expectations adapt.

That comment was “awarded” many “likes”, but although I was not trying to suggest that at all, I admit that would be a natural interpretation! In fact, I think Price Level Targeting is, in many ways, even worse than Inflation Targeting.

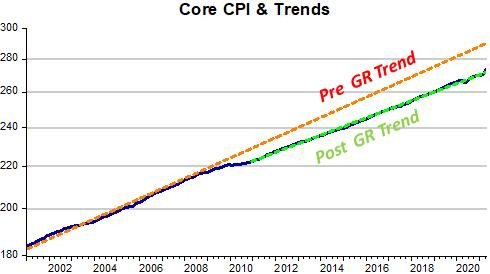

The things I want to bring attention to after the hoopla about yesterday´s CPI print is better developed by looking at the Core version of the chart above.

The Core CPI is certainly a much smoother process, basically because it´s much less impacted by volatile price, or supply, shocks.

George says “inflation expectations adapt”. They certainly do. “Expected”, or trend, Core CPI inflation Pre “Great Recession” (going back all the way to the early 1990s, when inflation became “low & stable”) is 2.3% (remember, given the Fed targets PCE inflation, that CPI inflation is, on average, 0.4p.p. above PCE inflation).

Post “GR”, “expected”, or trend, Core CPI inflation is a bit lower, at 2.0%. That is consistent with the below target PCE inflation experienced over the last 10 years.

Although the Price Level has shifted down, “expected”, or trend, inflation has moved down much less.

To me, the important question to be answered is “what drove that pattern”?

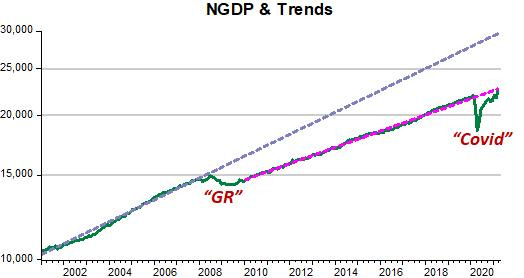

If we look at the most encompassing nominal aggregate, NGDP, we note that following the GR, the Fed never “bothered” to bring aggregate nominal spending back to its previous level. After the Covid19 shock, however, the Fed has (as of March) put NGDP back very close to its post GR trend path.

Before the GR, “expected”, or trend, NGDP growth was 5.5%. Thereafter, the Fed “calibrated” NGDP growth at 4%. The takeaway is that a permanently lower level path of NGDP will be accompanied by a permanent lower Price Level path, and a lower NGDP growth rate brings about a lower rate of price inflation.

I believe the inflation rate falls by less than “warranted” by the fall in the growth rate of NGDP because of the explicit 2% inflation target.

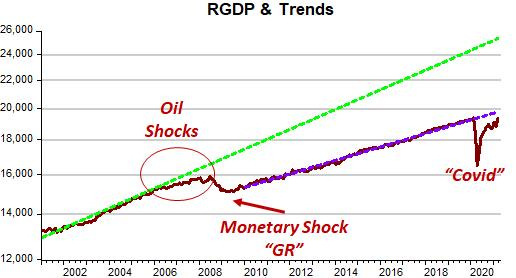

The real implications of the Fed´s purposeful reduction of the level path of aggregate nominal spending is evident in the real output (RGDP) chart.

Note that during the period of oil shocks, RGDP growth falls (while NGDP growth remains on trend). That´s an implication of “good” monetary policy. However, when the Fed got extremely worried about the rise in the headline inflation in mid 2008, monetary policy was tightened, bringing about a crash in NGDP.

With those actions, the Fed “drove” the economy into what Larry Summers called “Secular Stagnation” (could also be called “long depression”).

Now, if the Fed, as Powell frequently mentions, wants to take the economy to a “better place”, they will want to raise the level of NGDP above the “low post GR path”, in other words, somewhere between the Pre and Post GR trend paths.

If this happens, the increase in the NGDP level will also increase the Price Level. During the transition period, inflation will rise, with that being the only way that the price level will increase. We must note that the stronger the reaction of RGDP, the lower the increase in inflation (and the Price Level).

My hope is that the Fed will not “cold feet” with the rise in inflation, because that is to be expected and will be transitory.

Could Fed/fiscal be trying to move US to the higher nominal GDP line? A quick 30% shift up effectively fixes some of the debt and spending issues unless inflation genie (and rates) gets loose.