State of Play (July 21)

State of Play (July 21)

Simultaneous supply & demand shocks imply "hardships" for central bankers

Last month´s caption was from Steve Hanke at the WSJ on July 28:

Fed Chairman Jerome Powell conceded at his press conference Wednesday that prices had caught the central bank by surprise, but he showed no particular concern. The Federal Open Market Committee’s statement Wednesday after its two-day meeting also showed little interest in reeling in what has been the most reckless monetary policy since Arthur Burns roamed the Eccles Building. History hasn’t been kind to Burns.

This month I borrow from Nouriel Roubini´s August 31 piece for Project Syndicate “The Stagflation Threat is Real”:

There is a growing consensus that the US economy’s inflationary pressures and growth challenges are attributable largely to temporary supply bottlenecks that will be alleviated in due course. But there are plenty of reasons to think the optimists will be disappointed.

While Hanke stressed the inflationary effects of the Fed´s reckless monetary policy, Roubini adds to that the supply constraints, leading to a stagflationary scenario.

I have been warning for several months that the current mix of persistently loose monetary, credit, and fiscal policies will excessively stimulate aggregate demand and lead to inflationary overheating. Compounding the problem, medium-term negative supply shocks will reduce potential growth and increase production costs. Combined, these demand and supply dynamics could lead to 1970s-style stagflation (rising inflation amid a recession) and eventually even to a severe debt crisis.

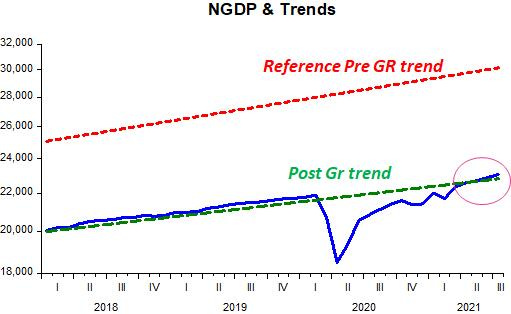

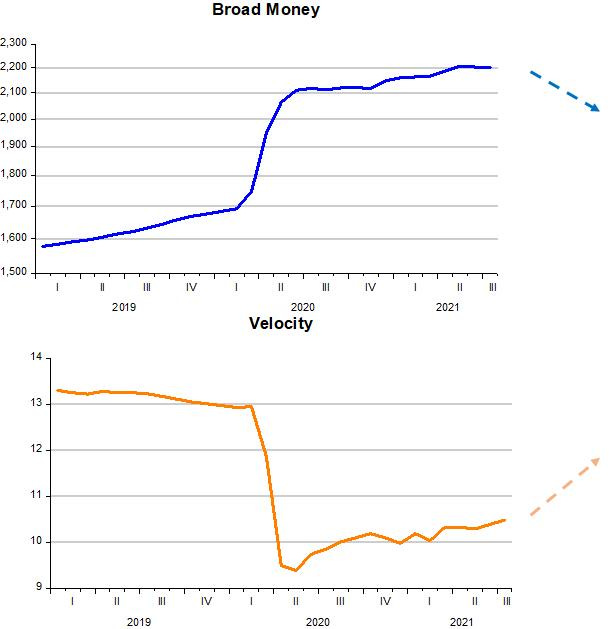

The “Thermostat” is a useful analytical apparatus to tackle these questions. Here, monetary policy (“juggling” the money supply) is the thermostat. It´s function, as always, is to keep the “inside temperature” (NGDP) stable in the face of variations in the “outside temperature” (velocity).

The chart shows the workings of the “Thermostat”

Note that, between the two vertical bars, the rise in the “outside temperature” is higher than the fall in the thermostat setting, so that the “inside temperature” rises. To the right of the second bar, the fall in the thermostat setting is bigger than the fall in the “outside temperature”, resulting in a drop in the “inside temperature”.

Before the start of the pandemic, the “Thermostat” was working fine, keeping the “inside temperature” very stable, as you can verify from the almost constant growth in NGDP.

When the pandemic hit, the “outside temperature” (velocity) plunges. That´s a demand side shock. At the same time, aggregate supply also contracts, but the “thermostat” doesn´t take that into account. Since the fall in the “outside temperature” was a surprise, the “thermostat” reacts with some delay. But it did react to try and bring the “inside temperature” back to its previous level.

As the next chart shows, it succeeded, with the “level” of warmth stabilizing at the preceding trend path.

A basic principle of good monetary policy is that it should not react to supply shocks because if it does, you risk destabilizing the system.

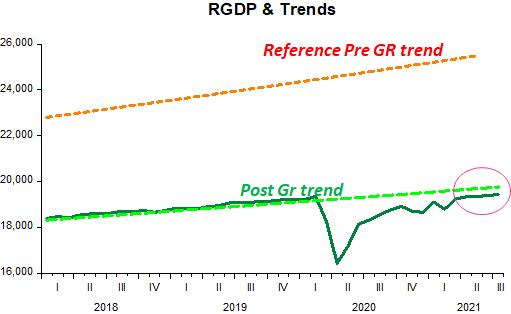

The next chart describes the “real warmth” that resulted from the workings of the thermostat described in the previous chart.

Note that until early this year, “real warmth” (RGDP) was closely following “general warmth” (NGDP). Since then, NGDP rose to trend and remained on that path, while RGDP flattened out.

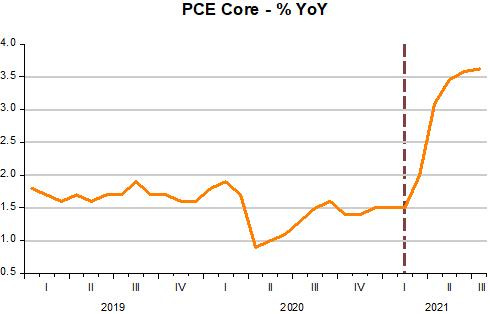

That´s when the supply bottlenecks became an effective constraint. And as the dynamic AS/AD model indicates, a supply shock will decrease real output growth and increase inflation. As the next chart indicates, that´s exactly what happened.

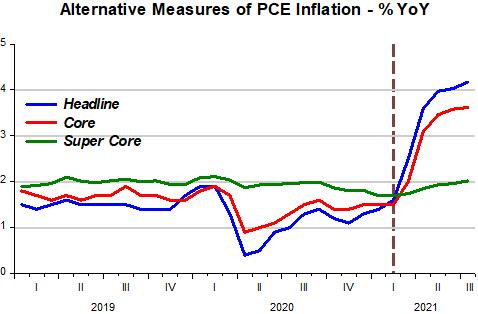

The nature of the supply shock this time around, is different from the usual oil price type supply shock, with supply bottlenecks affecting different sectors with different intensities.

This is clearly evident in the next chart, which illustrates movements in headline, core and “super core” (trimmed mean PCE) prices. It´s obviously more than just your typical food and energy supply shock, given that ex food & energy prices also increased, but still substantially less than an overall increase in the general price level (which is the definition of inflation), with many sectors not experiencing supply bottlenecks, as indicated by movements in the “super core” prices.

Powell´s stated objective (when he shows concern with the labor market and redefines the concept of “maximum employment”), is to take NGDP to a higher trend level path. He also seems to understand that this has to be done with care, given the distortions from the pandemic still present.

If the Fed doesn´t get “anxious” and waits out the pandemic-related distortions to abate, it is unlikely that inflation will become a concern.

Over the next several months as the pandemic wanes and supply bottlenecks get resolved, it is likely that velocity will rise to near levels that prevailed before the pandemic. The quantity of money will have to decrease by an amount necessary to put NGDP (and RGDP) at the desired level path.

A little short, but the Fed has managed this crisis much better than the last. I heard a rumor that Biden is considering replacing Powell, but I think it would be a mistake.