State of Play (April 21)

State of Play (April 21)

Is the inflation risk real, as Larry Summers thinks?

Both the GDP monthly data from IHS Markit and the broad money (Divisia M4) from the Center for financial Stability for the month of April were released. What do they tell us?

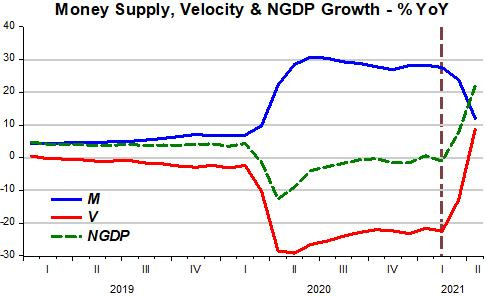

The “working of the thermostat chart” below shows that from February to April, broad money supply growth dropped from 28% (YoY) to 12%, velocity rose from -23% to +9%. The result was an increase in NGDP YoY growth from -1% to +22%.

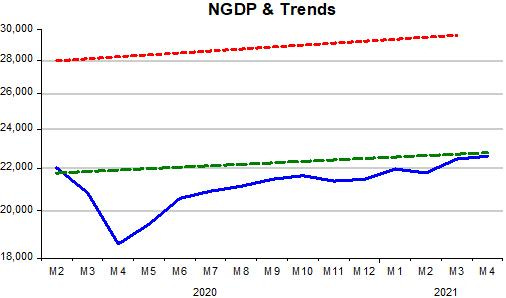

It seems the economy “heated up” quite a bit. Now we ask, what level of “warmth” did the “heating up” achieve? Very close to the level of “warmth” that prevailed since the GR to the start of the pandemic and that´s far “cooler” than the level that prevailed before the GR!

The “adjusted, or real warmth”, however, shows almost no improvement from the March level, and remains very far below the level of “real warmth” that prevailed before the GR.

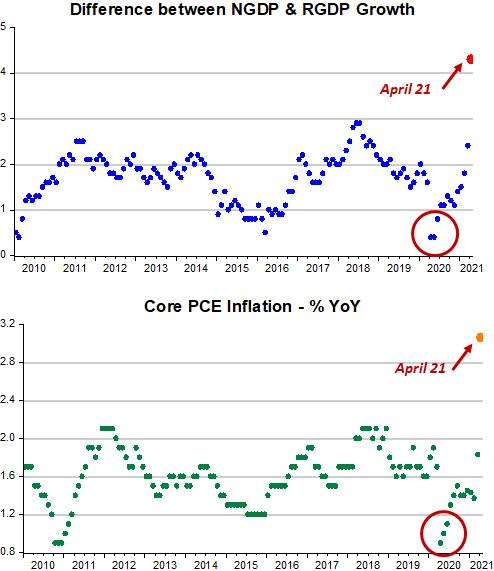

While nominal aggregate demand (NGDP) growth “turns on a dime”, aggregate supply growth faces bottlenecks. With the quick demand turnaround, the economy faces “shortages” of many things. The Fed believes that these shortages are temporary, that this is only a blip and that inflation will subside.

The charts below illustrate the point. The top chart graphs the difference between NGDP and RGDP growth, while the bottom chart graphs the rate of core PCE inflation.

What these charts tell us is that if the Fed is successful in maintaining Nominal Stability (stable level trend path for NGDP), it will also keep RGDP growth stable and also get low and stable inflation.

As the crimson circle suggests (and the first three charts in this post indicate), when NGDP tanks (its growth rate becomes negative), the immediate effect is for RGDP growth to fall by less (reducing the difference between NGDP & RGDP growth) and for inflation to fall significantly.

The quick turnaround in NGDP growth has the opposite effect. To avoid a more protracted rise in inflation, the Fed will have to dampen the speed of NGDP growth (by “fiddling with the thermostat”) or, in other words, offsetting more forcefully the rise in velocity that takes place with the progressive control of the pandemic.

Hopefully, we´ll get a taste of Keynesian economics. As Roger Farmer put it:

In Keynesian economics: Demand creates its own supply.

Neither Friedman nor Barnett got AD right.. AD is money times transactions' velocity, not N-gDp.