Seniority Ends at the Wall

Hanno Lustig says bondholders own the riskiest tranche of the United States — and retirees own the safest. He's right about the path to the Wall — but the ranking dissolves on impact.

This post comments on Hanno Lustig’s “The United States Capital Structure” (June 2, 2026). . His framing is the best way to think about who bears American fiscal risk. My addition is what happens to his ranking when the Wall is reached — the subject of my recent posts on the fiscal wall. See here and here.

Think of the United States federal government as what it has popularly, and appropriately, become over a century: a giant pension and insurance company with an army attached.

That is also Hanno Lustig’s image. The “firm” has roughly $28 trillion of marketable debt outstanding. It has 67 million Social Security recipients, 65 million Medicare enrollees, some 80 million on Medicaid. Sixty percent of its spending is mandatory — promises that flow automatically, with no annual vote. Only 27 percent is discretionary, defense included. The rest is interest.

And like any leveraged firm, it has a capital structure: an ordering of who gets paid, and who absorbs the losses when the bad state arrives.

The inversion

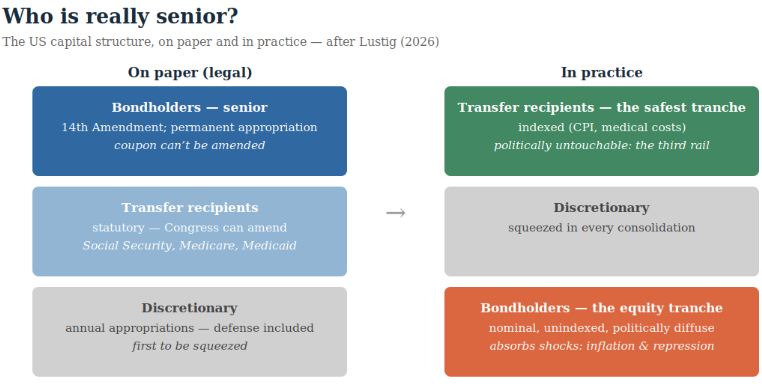

On paper, the bondholders look senior. The 14th Amendment says the validity of the public debt “shall not be questioned.” Interest is paid through a permanent appropriation, no annual vote required. Congress can amend Social Security with a statute; it cannot unilaterally rewrite a bond’s coupon.

Lustig’s insight is that the practical ordering is the reverse of the legal one.

The transfer recipients hold claims that are statutory but politically untouchable. And those claims are indexed: Social Security to the CPI, Medicare implicitly to medical-cost inflation, which historically runs hotter than CPI. Their real value is protected.

The bondholders hold claims that are legally sacrosanct but contractually nominal. Nothing prevents the United States from inflating their real value away — and no statute requires Treasury to pay them ahead of anyone else if cash runs short.

[Figure 1] — The US capital structure, on paper and in practice. Legally, bondholders sit on top; practically, the ordering inverts — indexed, politically protected transfer recipients hold the safest tranche, and nominal, unindexed Treasurys absorb the shocks.

So when an adverse fiscal shock arrives, it cannot land on the indexed, politically defended tranche. It lands on the one class of claimant that is contractually exposed to the price level and politically diffuse: the owners of Treasurys get hit by surprise inflation, financial repression, or both.

The boomers, in other words, own the senior tranche. The bondholders own the equity. COVID was the dress rehearsal: holders of US Treasurys lost about 15 percent in real terms, by Lustig’s reckoning, while indexed benefits sailed through untouched.

There is even a reason the market prices this rather than ignoring it. In textbook models, the bondholder and the beneficiary are the same representative person, so the risk washes out. In reality, bond ownership is concentrated. The people holding the equity tranche are not the people holding the senior one — so fiscal risk carries a price.

Three cracks in the ranking

The frame is illuminating, and I want to push on it in three places — not to overturn it, but to mark where it bends.

First, the seniority is an equilibrium, not a law. “Politically impossible to cut benefits” is true until it isn’t, and the politics that protect the senior tranche are themselves a function of the fiscal position.

Current law already contains the counterexample: when the Social S toecurity trust fund runs dry — 2033, on present projections — benefits are cut automatically by close a quarter unless Congress acts. The untouchable tranche has a haircut written into statute, and it is dated.

Second, inflation reaches the senior tranche through the side door. CPI indexation protects with a lag, and the index itself is a political variable — every chained-CPI proposal is an attempt to dilute the senior claim slowly. Medicare’s “indexation” is a commitment to pay for services, which Congress dilutes constantly through provider-payment formulas.

The tranches are less sealed than the diagram suggests; the inflationary adjustment assigned wholly to bondholders spreads upward.

Third — and this is the door into my own recent posts— Lustig´s post stops one step short of the regime question. Saying bondholders absorb shocks through inflation tells you who pays. It does not tell you what that does to the monetary regime that decides how much they pay, and when.

Where the capital structure meets the wall

Here the Lustig frame and the fiscal-wall arithmetic snap together, and each supplies what the other lacks.

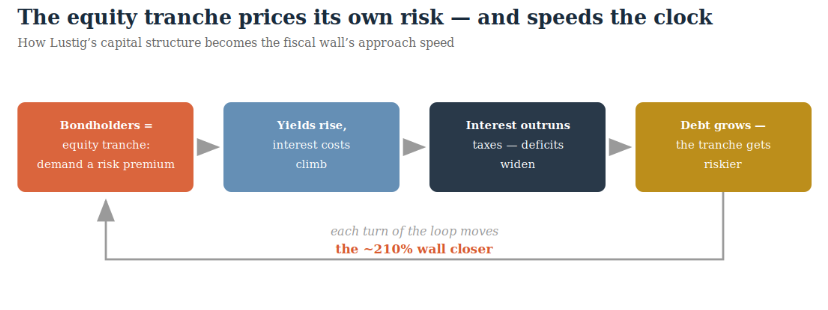

If bondholders are the equity tranche and they know it, then the yield they demand must carry a fiscal-risk premium — and that premium grows with the debt.

The riskier the equity tranche becomes, the higher the return it requires; the higher the return, the faster interest outruns the taxes available to pay it.

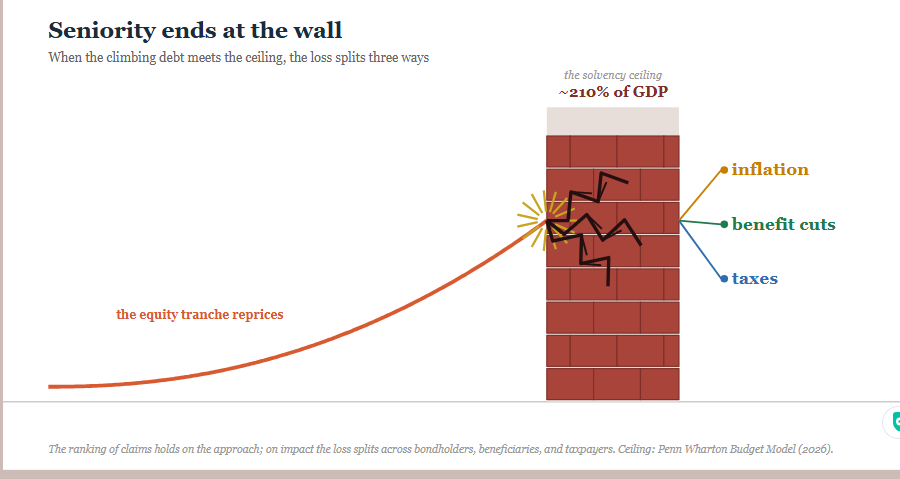

Lustig’s capital structure is the microfoundation of the wall’s approach speed. The Penn Wharton Budget Model’s recent estimate puts the outer bound near 210 percent of GDP, with a median arrival in the late 2040s and meaningful odds far sooner; a bondholder class that reprices its tranche moves those dates closer.

[Figure 2] — The loop that speeds the clock: the equity tranche demands a fiscal-risk premium, yields rise, interest outruns taxes, debt grows, the tranche gets riskier — and each turn moves the ~210% solvency ceiling closer.

And his conclusion — the adjustment lands on bondholders through the price level, not on benefits through cuts — is the asset-pricing version of the argument I have been making from the monetary side.

The fiscal-real models see two exits from the room: impossible taxes or explicit default. The history of fiscally exhausted countries with their own currency says the cornered government takes neither; it takes the third door, the one the models without money cannot see.

The dollar gives before the bond does. Lustig reaches the same door from security design: the equity tranche absorbs the loss, through diminishing purchasing power.

But now run his ranking all the way to the wall, and watch it dissolve.

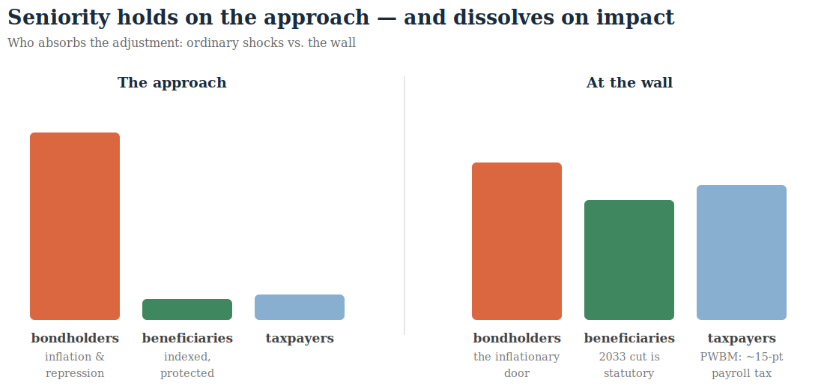

The seniority ordering describes the approach — the long path in which shocks are absorbed by the tranche least able to resist.

At the wall itself, the arithmetic outranks every tranche. The Penn Wharton endgame is a permanent payroll tax of some 15 points or benefit adjustments once thought unthinkable; the 2033 automatic cut is the statutory preview.

When “politically impossible” meets “arithmetically necessary,” something politically impossible happens anyway. The only question is the mix: how much lands on the bondholder through inflation, how much on the beneficiary through the benefit formula, how much on the worker through the tax code.

[Figure 3] — Who absorbs the adjustment. Along the path to the Wall, the equity tranche takes it quietly through inflation and repression. At the Wall, the arithmetic outranks every tranche: the inflationary door, the statutory 2033 benefit cut, and the PWBM ~15-point payroll tax compete for the same correction.

Seniority, in other words, is a fair-weather concept. It tells you who absorbs the ordinary shocks. It cannot tell you who absorbs the extraordinary one, because at that point the capital structure is no longer a constraint on the outcome — it is one of the things being restructured.

What to take from the frame

None of this diminishes the post; it extends it. Three things are worth carrying.

The legal-versus-practical seniority distinction is the simplest way to explain why US fiscal risk concentrates in the Treasury market rather than the benefit rolls — and why the term premium, not the politics of entitlements, is where the strain will show first.

The indexation asymmetry — real claims for beneficiaries, nominal claims for bondholders — is the mechanism by which the inflationary exit redistributes. It is one thing to say inflation is the likely door; it is another to specify exactly who is standing in front of it.

And the concentration point deserves more attention than: because bond ownership is concentrated, the fiscal risk is priced, visible, and capable of moving markets before the arithmetic binds. The equity tranche can panic. Senior tranches rarely do.

Which is the final, uncomfortable symmetry. In Lustig’s structure, the bondholders sit at the bottom and absorb the shocks — until the day their repricing is the shock. The capital structure holds right up to the moment it becomes the thing that breaks.

Postscript: the door Furman doesn’t name

Jason Furman, who chaired the Council of Economic Advisers under Obama, has just recently published an op-ed in the Times that reads like the political-economy companion to the argument above — the same structure, seen from inside the machine. It is worth reading against the frame.

Start with the one number I dated. I put the automatic benefit cut at 2033 and near a quarter.

The new trustees report, which is Furman’s reference, moves it forward: the retirement fund now empties in about six years, with a statutory cut of 22 percent waiting on the other side. The haircut written into the senior tranche kept its place in the law and lost some runway. That is the “equilibrium, not a law” quip, confirmed by the calendar — the date didn’t hold still; it moved closer.

Furman states the senior-tranche thesis more bluntly than I did. Recipients haven’t taken to the streets, he writes, because they know from experience they will be spared — “it’s everyone else who will be made to pay.”

That is the indexed, politically defended tranche described from the inside. And he supplies the microfoundation I only gestured at: the share of the voting-age population drawing benefits rises from the twenty percent that first made Social Security the third rail to roughly thirty percent within six years. The seniority is not holding by accident. The tranche gets more senior through demographics.

But the revealing part is what his frame cannot see — and it is the same blind spot I attributed to the fiscal-real models. Furman lays out the two exits clearly.

Close the gap on benefits alone and you need immediate cuts of about a fifth, which Congress will not do. Close it on revenue alone and the top effective rate clears fifty percent, which it also will not do. Then he predicts the path the country actually takes: kick it down the road, and draw on the rest of the budget to cover the shortfall.

That third option is not a resolution. It is the mechanism by which a ring-fenced program shortfall becomes general debt.

The moment Social Security is paid out of the general fund, its deficit stops being a benefits problem and becomes a Treasury problem — which is to say it moves onto the equity tranche, the precise redistribution this post is about. Furman sees the can being kicked. The capital structure tells you where it lands.

So we agree on the approach path and diverge on the vocabulary. He names benefit cuts, tax increases, and the can. The post above names those plus the door he leaves out: the dollar gives before the bond does.

Furman´s predicted response — spare the senior tranche now by reaching into the general fund — is not an escape from the loop in Figure 2. It is one full turn of it. Protecting the beneficiary today is what brings the wall, where no tranche is spared, closer.

Which leaves his closing worry and mine in the same place. Furman hopes Congress finds a fix that does not come at the expense of our children. The capital structure is less hopeful about the form that fix takes: the bill is paid by whoever holds the claim that cannot vote and is not indexed. For now, that is still the bondholder.

Actually anyone with fixed dolllar value savings holds the risk. The US will eventually inflate its way out of debt instead of defaulting

We should be be doing the expenditure recustions and tax increases now not when we hit a “wall” because a) the damage of deficits starts to accreu when the deficit ocurrs and b) the choice of taxes and cuts is more likely to be better considered earlier rather than later. And over-target inflation is not the best respones even at a “wall.”

[Great image!]