Right Mechanism, Wrong Crisis

Paul Krugman sees the oil market clearly and the Hormuz crisis partially

Yesterday Paul Krugman published: “Oil Prices could easily go much higher”

Krugman’s piece is interesting precisely because of what it gets right and what it conspicuously omits.

What he gets right

His core supply-and-demand argument is sound. The world economy’s reduced oil intensity is not a buffer — it is a ratchet mechanism that forces prices higher before demand destruction occurs.

The 1970s adjusted at $40 oil because $40 was crippling. The 2026 economy requires something closer to $150-200 before the same demand destruction kicks in. His “prices have to rise high enough to cause a crisis even though we’re less oil-dependent” framing is a clear statement of that logic.

Where he is conspicuously thin

The piece treats this as an oil price story. It is not primarily an oil price story, and Krugman’s knows it. The fertiliser transmission chain is nowhere in the piece. This is not a minor omission. Fertiliser is not a substitute good.

You cannot respond to a nitrogen price spike the way you respond to a gasoline price spike by driving less. The crop either gets planted at the prevailing input cost or it doesn’t get planted.

The demand destruction that Krugman correctly identifies as the oil market’s adjustment mechanism simply does not exist in the fertiliser-to-food chain on any timeline relevant to the 2026 harvest.

The LNG omission is equally significant. Krugman’s CPI-indexed oil price chart is doing a lot of work he doesn’t question.

European natural gas — which is LNG-priced at the margin since the 2022 Russian cutoff — is not in that chart. The 30 percent surge in European gas prices in nine days is not captured by a US CPI deflator.

The semiconductor fabrication facilities in South Korea and Taiwan that run on Gulf LNG are not in that chart.

The aluminium smelters, steel mills, chemical plants, and glass manufacturers that began curtailment in Europe in 2022 and never fully recovered, are not in that chart.

Krugman’s “the real oil price isn’t much higher than Trump’s first term” observation is technically correct but analytically misleading, because the system entering this shock is carrying the unrepaired structural damage of the 2022 energy crisis into a second, larger hit.

The deeper problem

Krugman is taking a single market mechanism and tracing it clearly to its logical conclusion. The price has to rise until demand is destroyed; therefore the price will rise further than people expect. That is a genuinely useful contribution to the public conversation.

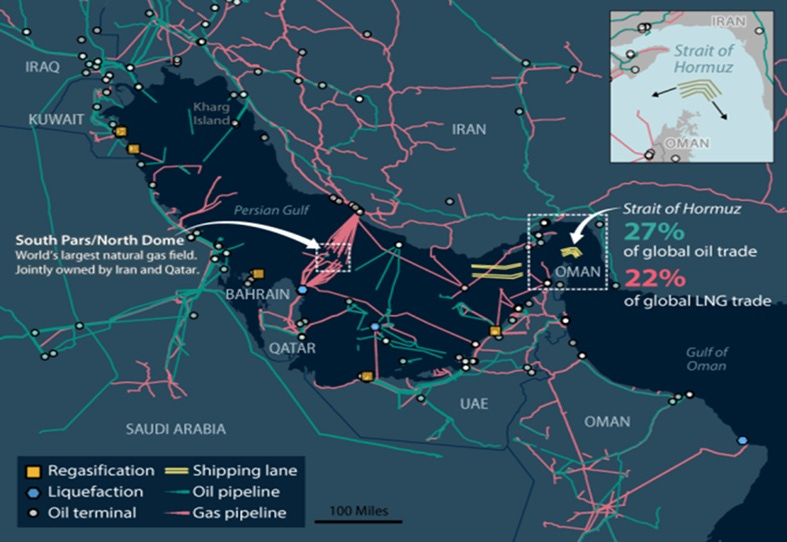

But the crisis brought on by the closure of the Starit of Hormuzis, something that never happened during previous conflicts, is not a single market shock.

It is a simultaneous shock to oil, LNG, fertiliser, shipping insurance, semiconductor energy inputs, and Gulf producer storage capacity, all activating at once in a system already weakened by two prior compound shocks.

The interactions between those systems are invisible in Krugman’s framework because his framework is a partial equilibrium model applied to a general equilibrium crisis.

The “alarmists warning of $150 oil” whom Krugman dismisses as too conservative are not wrong about the number. They are wrong about the variable.

The question is not whether oil reaches $150. The question is what $100 oil plus a 40 percent LNG spike plus a fertiliser shock plus a semiconductor energy cost crisis plus a European industrial curtailment wave plus a Global South sovereign debt trigger produces as a compound outcome.

The answer to that question requires a different analytical tool than the one Krugman is using.

The political subtext

There is also something worth naming about what Krugman is not saying. He is a prominent Democrat-aligned economist writing about a war launched by a Republican president.

His piece is carefully constructed to criticise the administration’s surprise at oil prices without engaging with the full catastrophic scope of what a sustained Hormuz closure produces — which would require him to describe something that looks less like a manageable demand-side adjustment and more like a generational shock.

That description would sit uncomfortably alongside the implicit message of his piece, which is roughly: this is bad, Trump is flailing, but the economy is more resilient than the alarmists say.

The evidence from the first fourteen days does not support the second half of that sentence. And Krugman probably knows it.

Before you go, click the ❤️ like button and re-stack this post to help me get it in front of as many people as possible.

Krugman made some predictions about oil in 2008 that were way off.

The price elasticity of demand is rather inelastic.