Reviving a higher inflation target proposal

Reviving a higher inflation target proposal

A boom in employment & output is the inducement

At the Peterson Institute For International Economics (PIIE), David Reifschneider and David Wilcox write “Another Reason to Raise the Fed’s Inflation Target: An Employment and Output Boom”:

This Policy Brief highlights an additional and less-noted consequence of raising the inflation target modestly: The economy could enjoy a temporary but substantial boom in employment and output as it adjusted to the increase in the target. Model simulations suggest that if the target were lifted to 3 percent, the unemployment rate could average ¾ percentage point or more below its sustainable level during the first 15 years after the higher target is announced.

The funny thing is that a higher inflation target was proposed even before the 2% target became official in January 2012, being suggested by Olivier Blanchard in 2010!

Reifschneider & Wilcox summarize:

Blanchard, Dell’Ariccia, and Mauro (2010) put the issue of raising inflation targets on the table more than a decade ago.

Ball (2013) unequivocally answered the question they posed in the affirmative and argued for a 4 percent inflation target.

At a 2019 European Central Bank colloquium, Adam S. Posen argued that the 2 percent inflation target adopted by many central banks had “outlived its usefulness.” Because he anticipated that no single bank would be able to do so on its own, he proposed that major central banks should raise their targets in a coordinated way.

Gagnon and Collins (2019a) also advanced the case for raising the inflation target, not only to provide the Federal Open Market Committee (FOMC) with more room to cut the federal funds rate but also to increase the effectiveness of large-scale asset purchases.

Ubide (2017) recommended moving the inflation target up in a manner that would take advantage of inflation surges, essentially by using a mirror image of the “opportunistic disinflation” approach advocated by Alan Blinder and others in the 1990s

If you take a moment to think about these arguments, you realize how “out of place” (in one word stupid) they are.

What, then, would be the robust driver of employment and output “booms”?

Regular readers already know the answer I´ll give. And I´ll couch the argument through easy to follow illustrations.

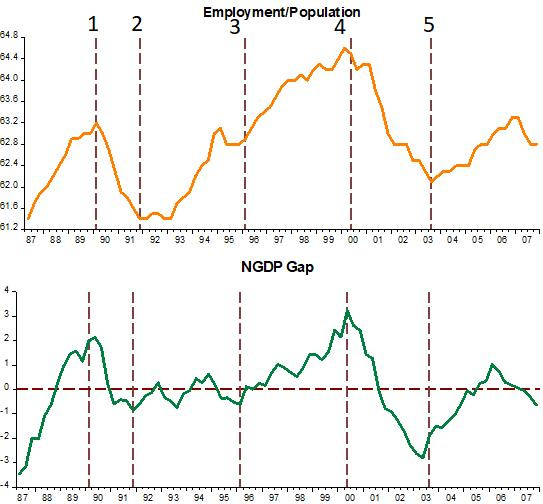

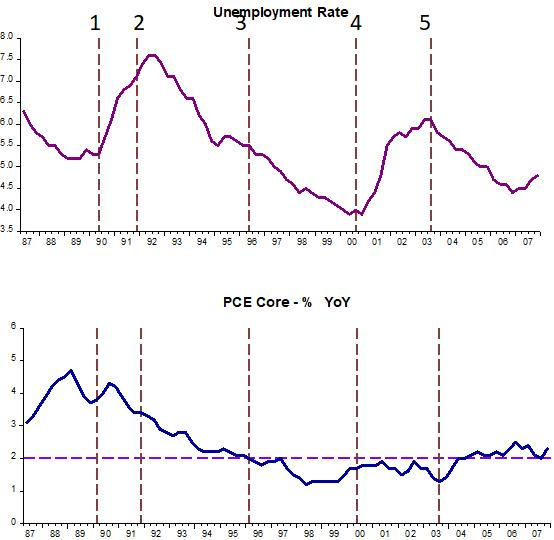

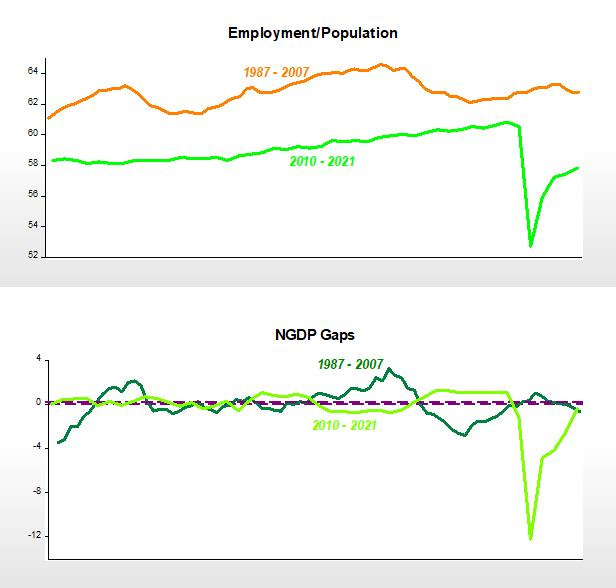

The charts that follow indicate that during the Great Moderation, from 1987 to 2007, fluctuations in employment conform to fluctuations in NGDP relative to its trend level growth path, which I call NGDP Gap.

Note, for example, that between bars 2 & 3, NGDP evolves very close to trend. During that time, employment rises. When NGDP growth accelerates (climbs above the trend level path), employment rises even more.

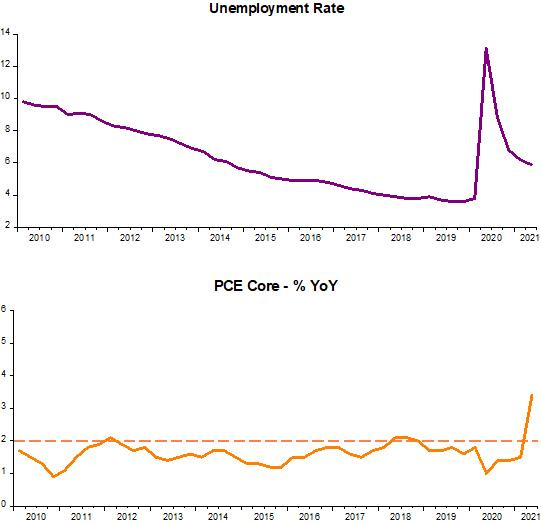

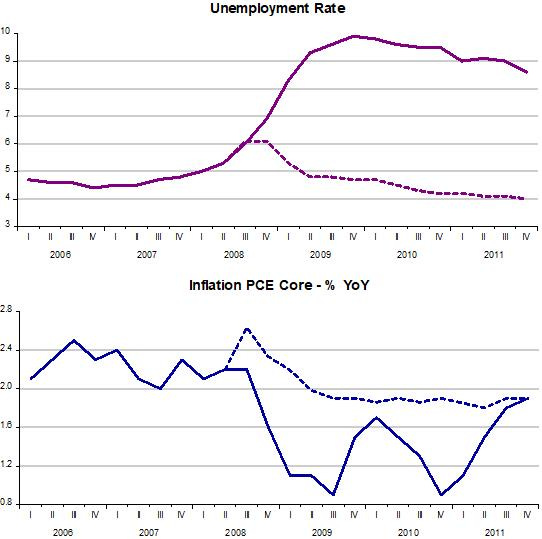

The next set shows that unemployment falls with employment rising and rises when employment falls, but there is no rise in inflation to propel the “booms”!

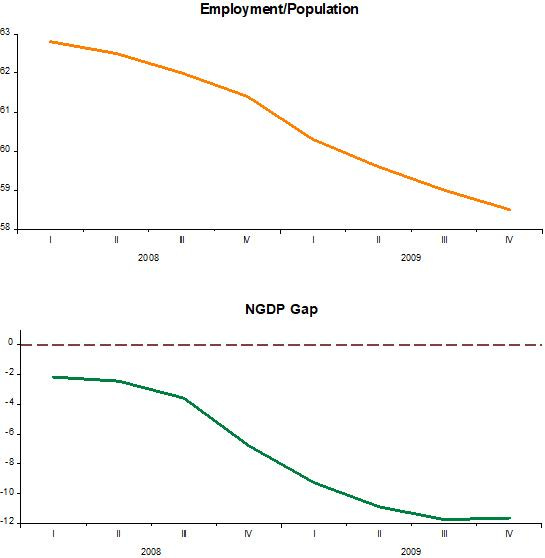

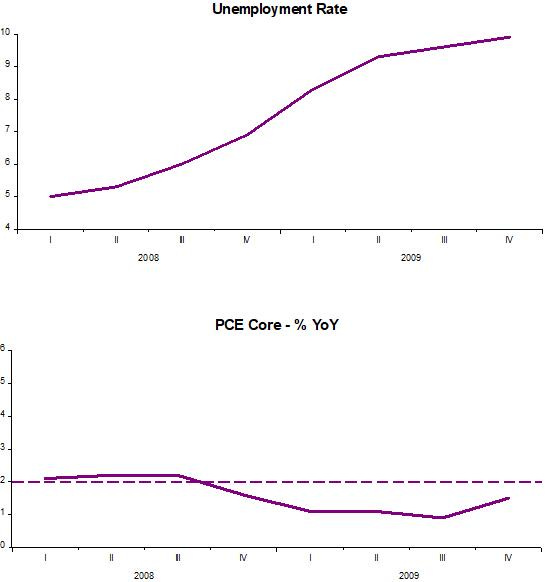

Going into the Great Recession, again it is NGDP relative to the trend level growth path that drives the process. Note that inflation has no say in it.

During the post Great Recession period (ending before the pandemic hit) NGDP is very stable. Employment shows no fluctuation and rises only very gradually after remaining flat for a few years (more on that later).

When the pandemic hit, NGDP tanks and so does employment. With NGDP bouncing up, so does employment. Note, however, that the employment bounce back is cut off. That´s the point in which supply bottlenecks come into play.

As the next set shows, with supply bottlenecks binding and NGDP rising, inflation increases, but NOT employment.

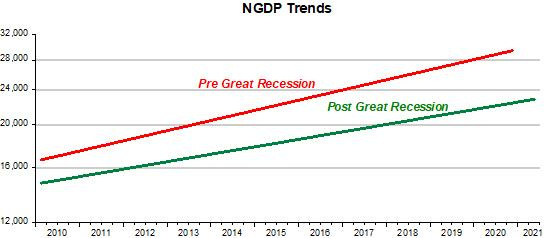

The next chart sets the stage for some required explanations for the different behavior of employment pre and post Great Recession. The trend level growth path post GR is significantly lower than the pre GR path.

As the next set shows, that explains why the level of employment is higher pre GR. And since NGDP stability is higher post GR, so is employment stability before the pandemic hit.

Interestingly one of the Reifschneider & Wilcox punchlines is:

In addition to reducing economic volatility in the long run, an increase in the inflation target would generate a temporary but substantial benefit as the economy adjusts to the new higher level of trend inflation. These transitional benefits are the focus of this Policy Brief.

As we illustrate using model simulations, the economy would likely experience a marked boom in employment and output during the transition period, provided the FOMC vigorously pursued attainment of the higher target rate.

If you substitute “inflation target” for “NGDP Level target” you get the same result in a simpler and more effective (and proven) way!

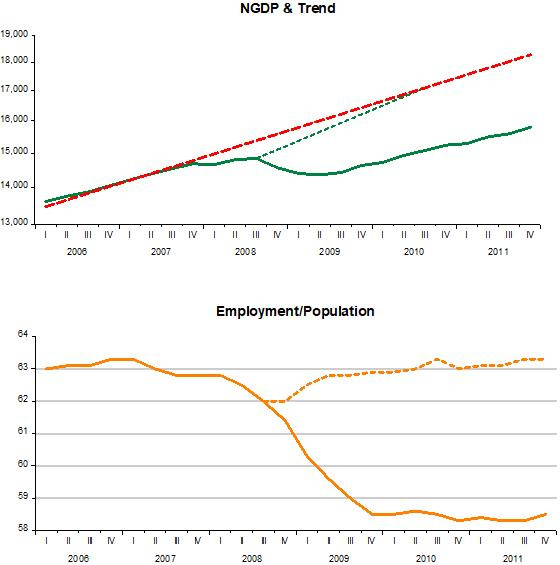

Below I do some back-of-the-envelope simulations asking what would happen to employment, unemployment and inflation if the Fed did not allow the Great Recession to take hold in the second half of 2008.

The charts need no accompanying words, perfectly illustrating the “magic” of stabilizing NGDP at an appropriate level path.

PS (Aug 31) Just saw that George Selgin did a post on R&W “suggestion” for a higher inflation target. George´s arguments are much deeper, but the conclusion is the same:

Were natural rates observable, implementing such an ideal policy would be a cinch. But because they aren't, the question becomes whether something close to it, or at least better than Reifschneider and Wilcox's proposed, permanent three percent inflation target, is possible. I think it is, and it's called nominal GDP (or simply NGDP) targeting.

PS1Coming up later this week “State of Play (July 21)”

"If you substitute “inflation target” for “NGDP Level target” you get the same result in a simpler and more effective (and proven) way!"

And yet, sadly, policymakers and central bankers continue to turn a blind eye.