…The Fed can always fall back on the unemployment rate to claim that although inflation is low now, it will creep back up to its 2 percent target with the economy operating at full employment.

The minutes of the July FOMC meeting made clear that central bankers remain committed to this Phillips curve framework. Although persistently low wage growth calls that claim into question, the Fed has good reason to believe wage growth will soon accelerate.

To understand why, note that there is no single wage measure. We have a number of different compensation metrics. Obviously, using the “best” or “right” measure would be optimal, but in the absence of such knowledge, I created a composite based on the average of some common compensation measures.

With this measure I created a Phillips curve for wages. You can see that the current spot on the curve (17.II) is an outlier: The Fed’s relative confidence that the economy is operating at full employment is not unreasonable. If recent data are historical outliers, then wage growth will jump sharply higher — and probably soon if unemployment keeps pushing lower.

My counterargument at the time:

Tim Duy puts too much emphasis on the latest “spot” being an outlier. However, if you do a more detailed analysis you find that’s not the case. The charts below illustrate.

It is clear that post the 2008 crisis, the Wage Phillips Curve not just flattened, it became flat. You see that the current (2017.II) spot is only an “outlier” if you think the data generating process has remained stable, which it clearly hasn’t.

The “outlier”, if there is one, is the 2008.IV spot. It occurs during the transition from the “steep” to the “flat” Wage Phillips Curve. At that time unemployment was rising fast, but wage stickiness impeded wage adjustment.

Duy’s conclusion is turned on it’s head. Since the recent data are not “outliers”, there is no indication that wage growth will jump sharply higher, let alone soon. Therefore, by remaining committed to its Phillips Curve framework, the Fed will continue to err, causing painful damage.

Update

What transpired on the way to C-19? Unemployment fell and remained low and stable while inflation was low (below target) and stable throughout!

The configuration observed in the chart above, where unemployment continuously decreases and remains very low, while inflation barely moves, is not what the “conventional wisdom” would “predict”.

Even with all this evidence, high brow people like Larry Summers “pound from the pulpit”:

The US Needs 5% Jobless Rate for 5 Years to Ease Inflation - Bloomberg

To explain the result in the chart panel above, many will evoke the pursuit of an appropriate interest rate policy by the Fed! But was that it?

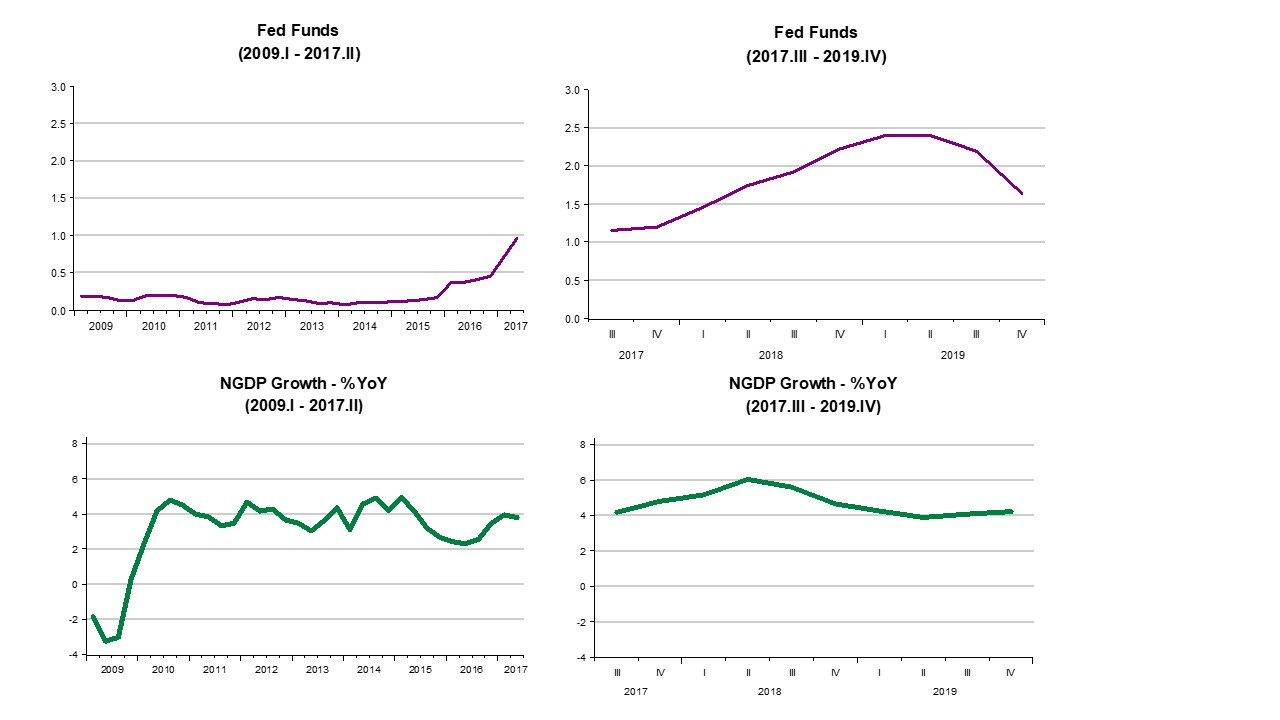

The panel below indicates that interest rates stayed put at close to zero from the end of the 2007/08 crisis to 2015, after which point it began to move up. All through that period monetary policy was “accused” of being excessively easy. Did that influence the outcome for inflation and unemployment?

I believe what mattered most was that after recovering from the criss “blast”, the fact that nominel aggregate spending (NGDP) growth remained very stable was the decisive factor. In other words, monetary policy was not “easy”, but “appropriate”, providing Nominal Stability.

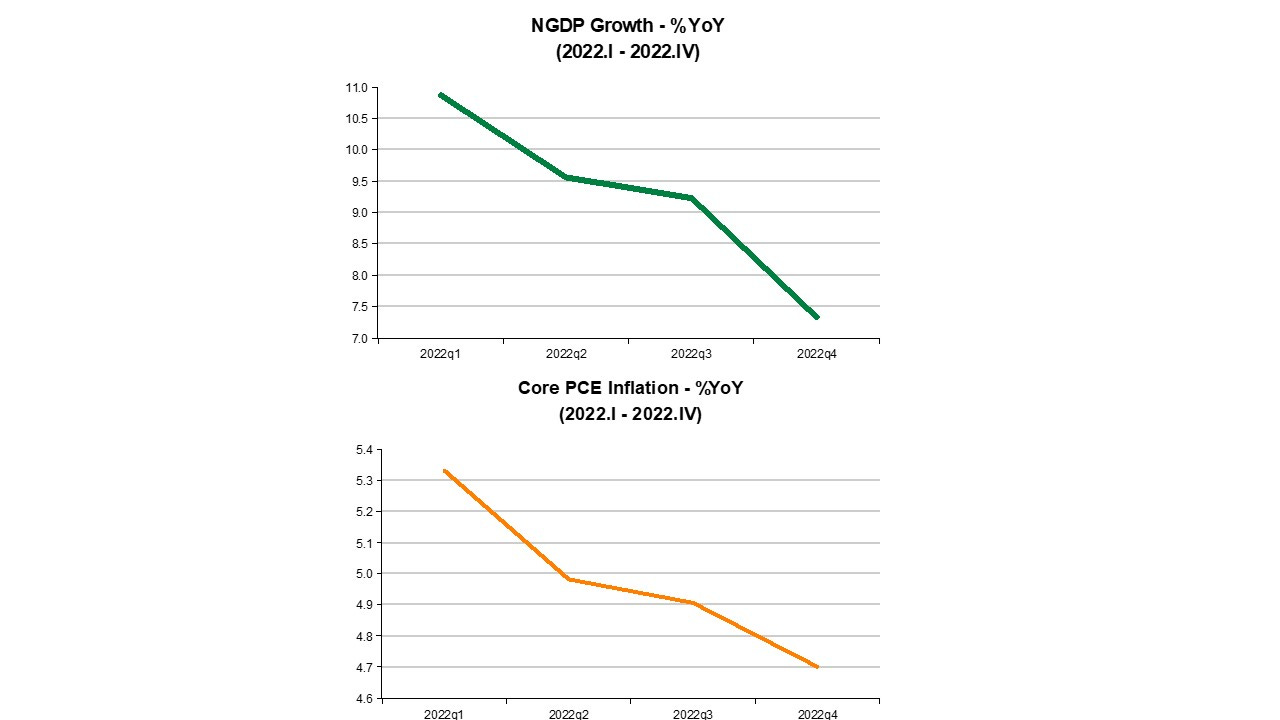

Moving to the present, the quick climb in interest rates over the past year has only been “good” to “incite” a banking crisis! “True monetary policy” has been moving in the right direction; reducing aggregate nominal spending (NGDP) growth towards the “target rate” of 4-5% growth, at which time inflation (in the charts below you can see their “DNA” is similar) will stabilize close to target!

Thanks for reading Money Fetish! Subscribe for free to receive new posts and support my work.

Lawrence K. Roos, former President, Federal Reserve Bank of St. Louis and part-time member of the FOMC (the Fed’s policy arm), was cited in the Wall Street Journal’s “Notable and Quotable” column, April 10, 1985, as follows:

“…I do not believe that the control of money growth ever became the primary priority of the Fed. I think that there was always and still is a preoccupation with stabilization of interest rates”.

Lawrence K. Roos, former President, Federal Reserve Bank of St. Louis and part-time member of the FOMC (the Fed’s policy arm), was cited in the Wall Street Journal’s “Notable and Quotable” column, April 10, 1985, as follows:

“…I do not believe that the control of money growth ever became the primary priority of the Fed. I think that there was always and still is a preoccupation with stabilization of interest rates”.

Great post. Would love to hear you back on Macro Musings to talk through this and other recent insights.