Perspectives on inflation

Perspectives on inflation

"Team Transitory" vs "Team Persistent"

A little over one year ago, I wrote “After Covid 19, inflation?”. With data to May 2020 I made some considerations, among them:

The economy faces a health issue with mammoth economic consequences. The thermostat dialed the temperature down “automatically” and will likely maintain the “cooler temperature” while the virus is “active”. All the Fed can do is work to ensure the temperature does not fall even more. Given the latest data available (May), it appears the Fed is managing to “hold the fort”.

What the inflacionistas worry is with the aftermath, after the virus loses relevance. They argue the massive rise in the money supply observed so far ensures an inflation boom in the future.

As the thermostat analogy indicates, you have to take into account the behavior of velocity (money demand). So far, even with the “Federal Reserve pouring money into the economy at the fastest rate in the past 200 years”, what we observe is disinflation!

How will the Fed behave once the virus loses relevance? Will it set the thermostat at the previous temperature (previous trend level path)? In other words, will it make-up for the losses in nominal spending incurred during the pandemic, or not?

…If the Fed undertakes a make-up policy, inflation will temporarily rise (just as it temporarily fell when the thermostat was dialed down).

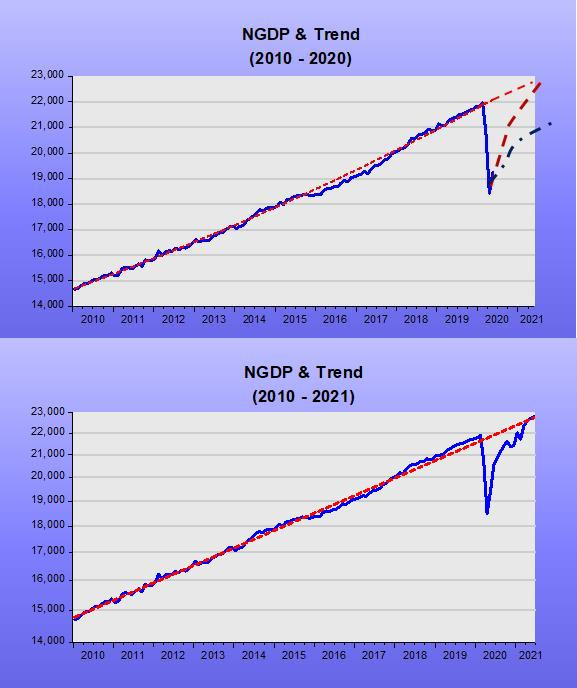

The two charts provide an illustration. The top chart, originally included in the “After Covid19, inflation?” post, shows the situation to May 2020 with dotted lines showing alternative scenarios. The bottom chart shows what actually happened.

Where aggregate nominal spending (NGDP) conforms to the more optimistic scenario from May 2020, and goes back to the pre pandemic (post Great Recession) level trend path.

The next charts zoom in on the recent period and shows that inflation temporarily fell during the “contraction” period and increased when NGDP rose to offset the previous drop.

The “steep” leg of inflation is associated with the “rush to trend” of NGDP. However, why did that manifest only then, having been subdued during the previous period when NGDP was also rising?

One group, the “Team Temporary”, appeals to supply bottlenecks - lumber, used cars, chips, container shipping, among others. The “supply bottlenecks” but a brake on real output expansion, and with spending increasing, prices rise. The next chart shows how, after a point, supply ceased to move towards the pre pandemic trend, flattening out.

If the “Team Temporary” conjecture is true, inflation will fall with supply bottlenecks being sorted out. How fast inflation falls will, however, be closely linked to how monetary policy behaves.

If the Fed keeps pressing the accelerator, higher inflation may become more persistent. That does not appear likely. Having reached the pre pandemic trend level path, the Fed is keeping spending on top of it, as illustrated in the NGDP& Trend chart above.

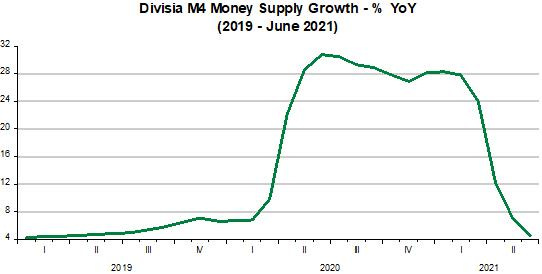

YoY Money supply growth has recoiled significantly, with broad money (Divisia M4) growth falling from highs of 30% in June 2020, to 4.5% this June, and is expected to have fallen below 4% (or even 3%) in July.

That´s why in June 2020, monetarists were positing:

By mid- or late 2021 the pandemic should be under control, and a big bounce-back in financial markets, and in aggregate demand and output, is to be envisaged. The extremely high growth rates of money now being seen – often into the double digits at an annual percentage rate – will instigate an inflationary boom. The scale of the boom will be conditioned by the speed of money growth in the rest of 2020 and in early 2021. Money growth in the USA has reached the highest-ever levels in peacetime, suggesting that consumer inflation may move into double digits at some point in the next two or three years.

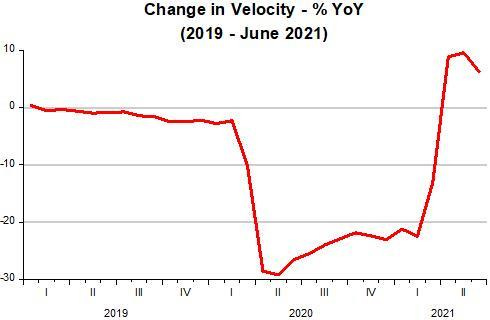

Forgetting to account for the fact that velocity (the inverse of money demand) tanked at the onset of the pandemic. In other words, if money supply growth hadn´t “ballooned”, the deep but brief recession would have quickly morphed into a “Greatest Depression”. Note from the next chart how money supply growth pictured above quickly managed to begin offsetting the drop in velocity (and later its subsequent rise).

To my mind, that was very good monetary policy. After all, after a recession, especially since this recession was not “Fed engineered”, you want to quickly make-up for the spending loss due to the pandemic!

Now, 14 months later, those same monetarists sent out an e-mail: “Time to go back to the fundamentals of inflation”

The rise in consumer price inflation in 2021, which is certainly very significant in the USA with CPI growing at an annual rate of 5.4% (June 2021), has caught many by surprise. In 2020, the consensus was that the pandemic would be disinflationary over the medium term and would thus require an accommodative monetary policy for a lengthy period. Now the debate has moved onto a consideration of whether the current inflationary episode will just be 'temporary' or not. Complacency dominates with leading central banks believing that inflation will fall to its target level in 2022 without any monetary tightening.

The summer may well be a good time to remember the fundamentals of inflation. According to what has been termed as the 'Friedman's k% rule', the rate of growth in the amount of money should mirror that in (real) economic activity, though allowing for changes in the velocity in money. As observed in the US data, sudden changes in the demand for money do occur in crisis times but tend to revert to pre-crisis levels afterwards. With the re-opening of the economy in the US and other leading economies, this means that excess money holdings accumulated in 2020 (thus, a fall in the velocity of money) will not persist for long and companies and households will increase their spending patterns. In fact, this is something we have already seen in recent months. The combination of the surge in the amount of money in 2020 and 2021 and the return of money velocity towards pre-crisis levels very much explain the current inflationary episode, which will very likely continue until the end of 2022.

If the US Fed wants to bring inflation down to its 2% target in the next few years, a necessary condition will be to return the annual rate of growth of money (broadly defined) to around 5%. With the current growth of the monetary aggregate M3 still in the double digits, the Fed's policies are not meeting the conditions to ensure inflation remains a short-term phenomenon.

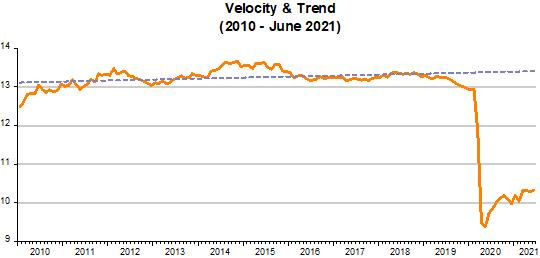

Different from June 2020, now they pay lip service to velocity (money demand) changes. The chart below shows that the level of velocity tanked at the onset of the pandemic, but it appears to be in no hurry to return to its trend level.

In fact, given that July witnessed the spread of the Delta Variant, velocity may even drop, which would require money supply growth to rise so as to offset the fall in velocity in order to keep NGDP on the trend path. If the spread of the Delta variant retards the sorting-out of supply bottlenecks, there could be additional pressure on inflation, unless the Fed allows NGDP to fall below trend again.

So far, indications are that the increase in inflation observed since February has temporary characteristics, associated with supply bottlenecks. We note that recently, PCE core inflation has decelerated. For July, CPI core inflation, for example, has turned down.

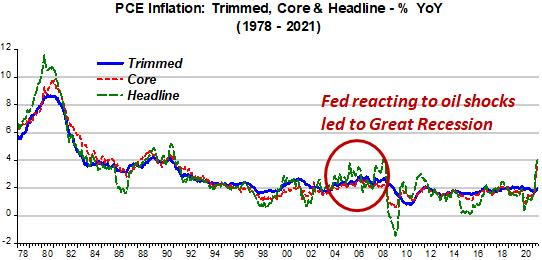

Let us look at inflation over a wide span. I concentrate on three versions of the PCE index. The headline, Core & Trimmed Mean versions.

From the St Louis Fed site, regarding the trimmed mean PCE:

The individual price changes are sorted in ascending order from “fell the most” to “rose the most,” and a certain fraction of the most extreme observations at both ends of the spectrum are thrown out or trimmed. The inflation rate is then calculated as a weighted average of the remaining components. The trimmed mean inflation rate is a proxy for true core PCE inflation rate. The resulting inflation measure has been shown to outperform the more conventional “excluding food and energy” measure as a gauge of core inflation.

Note the definition of inflation: a persistent rise in All prices. The 70s, satisfies the definition, with all price constructs on a rising trend.

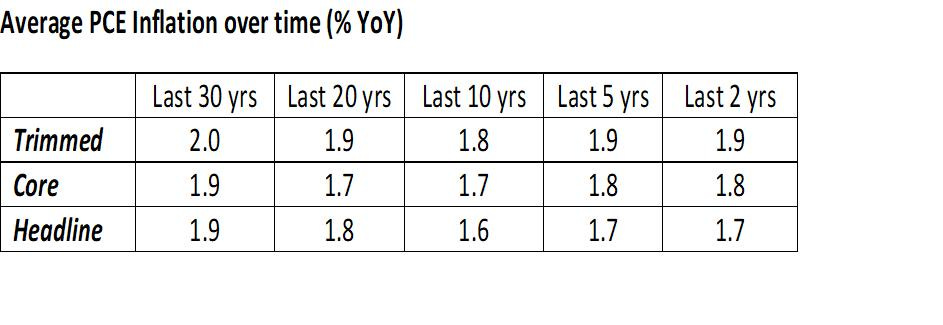

The Table below shows that after inflation was “conquered”, it became low & stable, varying very little over long or shorter spans. Note that even for the most recent period, average inflation is still below the Fed´s new AIT framework.

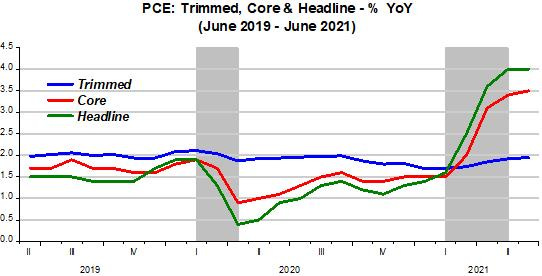

The chart below, covering the last two years, indicates that in a pandemic, core inflation is more than just leaving out food & energy prices.

Given that not all prices are rising, and those that are appear on the verge of reversing trend, the definition of inflation is not satisfied!

In my view, although in practice the Fed gets high grades for the conduct of monetary policy during the pandemic, the problem is the “language” of policy is all “screwed-up”. For one it is confounded with interest rate policy and the associated talk of “tapering” and such. Then, more confusion is brought to bear with the focus on employment/unemployment. More recently, things like “green monetary policy”, came on board.

The Fed´s objective should just be to balance money supply and money demand, or offset velocity changes in order to keep nominal spending (NGDP) growth on a stable level path. Choosing the “appropriate” level path is an important and non trivial consideration. Following the Great Recession, for example, the Fed “chose” to follow a “low” level path. Although nominal stability was attained, it was never satisfactory, as most felt they were living in a “depressed” state.

Going forward, how the pandemic evolves will be the main constraint on the Fed´s actions. So far there are no indications that it will “choose” to follow a path consistent with the views of “Team Persistent”!

You don't get it. Barnett didn't predict the "time bomb" in 1981. I did. And I predicted that AAA AAA Corporates would go to 15.48%. They went to 15.49%.

The definition of "transitory" is: "tending to pass away : not persistent".

Yet regardless of the slight deceleration in some of the #s, inflation remains virulent. Inflation exacerbates income inequality. Inflation is the most destructive force capitalism encounters.

FAIT increases prices faster than incomes"