Parsing, once again, and hopefully more convincingly, the Post Covid Economy

Parsing, once again, and hopefully more convincingly, the Post Covid Economy

Maybe a deeper understanding of the "facts" will be helpful to market participants

Many cried “wolf” too early, but when the “wolf” (inflation) took some time to show up, it was because of never well explained “lags” in the effect of monetary policy!

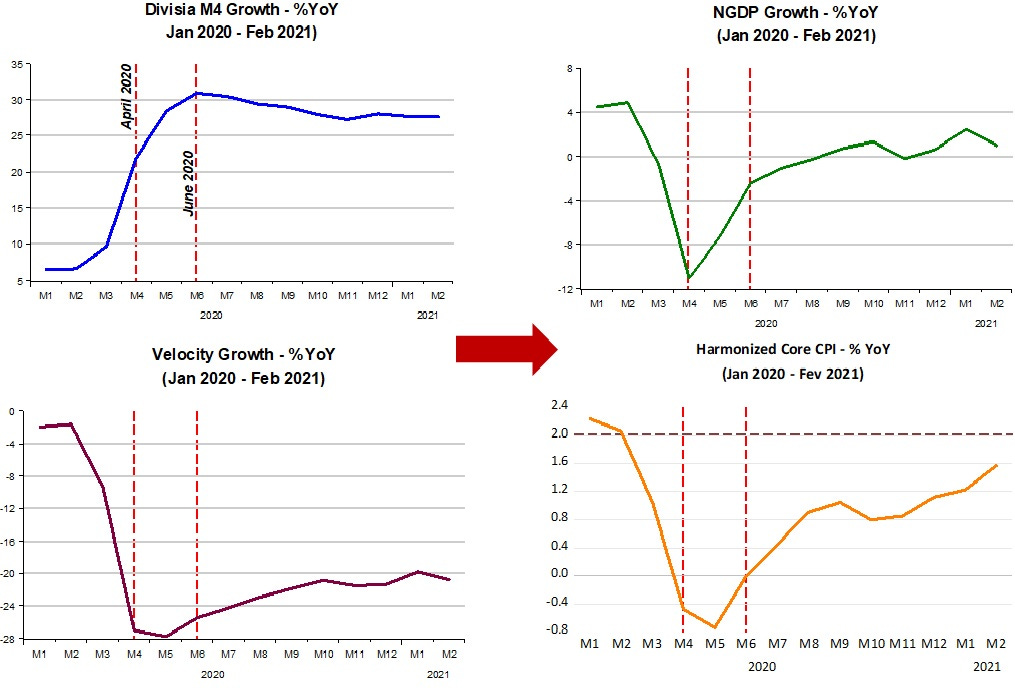

The two charts below, both from Spring 2020, April and June, respectively, are illustrative of the “one-legged monetarist” view that the only thing that matters for inflation is the growth rate of the money supply.

However, when we look at monetary policy from the “Perfect Correspondence” perspective , what happened becomes crystal clear.

The charts below show the stages of the C-19 economy. In the first stage, after being hit by the surprise and mostly desinflationary shock of C-19, money growth, “exploded”. But that was the right action for the Fed to take because velocity tanked (money demand growth, its inverse, skyrocketed)!

Note that between April 20 and June 20, velocity bottoms out and then begins a gradual increase. Meanhile money supply growth keeps rising, leading to a strong reversal in both NGDP growth and inflation.

After June 2020, velocity continues on a gradual rise while money supply begins a less gradual fall. The result is that both NGDP growth and inflation also gradually increase.

It is clear that the early “exploding inflation” calls from what I called “one-legged” monetarists were unfounded. Monetary policy during that phase was “appropriate”.

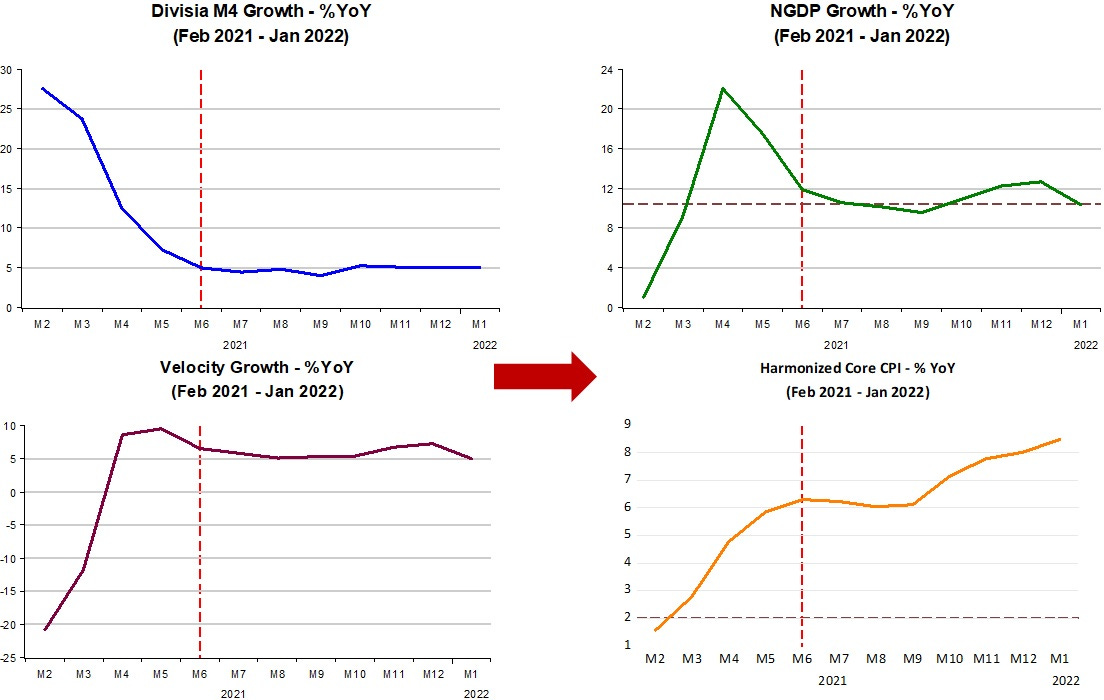

Now for the second (truly inflationary) stage.

To “one-legged” monetarists, since money supply growth is falling, inflation should fall. However, it rises. But that´s, again, because “lags” are “long & variable”, so the rise in inflation is a consequence of the previous “money explosion”!

Note that inflation increases due to the fact that, although money supply growth drops, velocity increases more. No wonder both NGDP growth and inflation increase. More, they move in accordance (with no “lags”) to the relative moves in money growth and velocity. When both money supply growth and velocity growth stabilize at approximately the same rate (to the right of the vertical dotted line), NGDP growth stabilizes at a rate which is the sum of those two rates.

According to the “thermostat analogy”, if the “outside temperature” (v) stabilizes at something close to 5% “degrees”, and the “thermostat dial” (m) is increased also by approximately 5% “degrees”, the inside temperature (NGDP) will rise by the sum of those two, or approximately 10% “degrees”.

That made the “house” “too hot”, increasing inflation despite a fall in money supply!

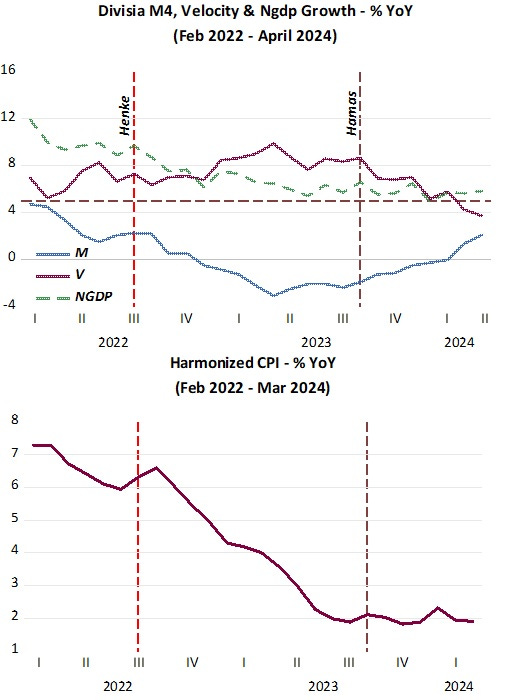

The third phase of the post C-19 economy is the monetary tightening phase. This begins in early 2022 (and not because that´s when rates begin to rise), but due to the fact that money supply growth begins to fall, even while velocity does not move much.

This time around, I put together the data for money growth, velocity and NGDP growth, which I believe , makes it easier to visualize this phase of the process.

The two vertical lines indicate “special moments”. Everyone may remember that from mid-2022, prognosis of an upcoming recession became “popular”. Some of those were tied to the fact that in March 2022, the Fed had begun a strong hike in rates, but I want to emphasize the forecasts of the typical one-legged” monetarist.

In August of 2022, Steve Hanke (the “representative agent” for that group) “pontificated”:

In an interview with CNBC’s “Street Signs Asia” on Monday, Hanke argued that a major economic downturn had been made inevitable due to U.S. money supply soaring and stagnating.

“We will have a recession because we’ve had five months of zero M2 growth, money supply growth, and the Fed isn’t even looking at it,” he said. “We’re going to have one whopper of a recession in 2023.”

Henke does not desist. From just yesterday:

The Fed has BLUNDERED, AGAIN. "The US is currently experiencing an 'unprecedented' monetary contraction. The US has only experienced four monetary contractions since the founding of the Fed in 1913. All have resulted in recessions."

We all know that 2023 came and went without a recession taking place! On the contrary, real growth has remined robust since early 2023 and unemployment remained below 4% throughout!

The second “special moment” comes about when Hamas “terrorized” Israel in early October 2023. At that point, velocity begins to fall (money demand rises), likely reflecting the increased geo-political uncertainties that would likely (and did) follow that event.

Note that until then, NGDP was gradually falling, reflecting the continued tightening of monetary policy, where money supply growth was falling in the face of a relatively stable velocity.

When the Hamas “event” happens, the Fed quickly “eases on the brake” and the fall in NGDP becomes more gradual (despite the fact that interest rates had peaked immediately prior to the “event”).

Note than when “Hamas” happens, one measure of inflation, the Harmonized Core CPI (that only excludes the “turbulent” OER) had already “landed” at the 2% target.

Now things are getting more complicated. While the Fed remains attached to its “lack of confidence” that inflation is truly moving to the target rate, some commentators and market participants are beginning to have qualms.

These two (among several others) are saying the same thing from different perspectives:

The fact that equities are not responding well to the renewed pullback in Treasury yields and the swaps market beginning to price in a September rate cut is signaling something important: that stock market investors are also becoming concerned about the economic slowdown and what it means for the earnings outlook.

Krugman´s view:" So it’s time to stop obsessing about inflation, which increasingly looks like yesterday’s problem, and start worrying about the possibility of a recession as the economy’s strength finally begins to erode under the strain of high interest rates."

Also, society in general has shown more doubts:

There's a great divide in the U.S., and it's not partisan. It's the big gap between how people see their finances (pretty good) and their view of the overall economy (terrible), and it's persisted for years since the pandemic.

Brian Albretcht at Economic Forces tries to understand the “feeling”:

The broad takeaway is that we shouldn't confuse the micro for the macro. The US economy is a vast, complex system, more like the weather than a machine. Understanding the complexity and the relative scale of different actors within it is essential for clear-eyed analysis and effective policy.

Likely unconsciously (therein lies the danger), the Fed is doing the right thing (very likely, not beginning to bring rates down is, also unconsciously, a wrong move). If monetary policy (distinct from interest rate policy) continues to bring NGDP growth to the 5% rate, to which it is very close, PCE inflation, the inflation that “matters”, will also continue to converge to the 2% target. With that, real growth will remain positive and adequate and unemployment low and stable

I believe that´s the necessary condition for nominal stability, which in the end is what will “pacify” a host of economic actors. I also know that for success in market activities, it is not enough to be right. What matters is the “wisdom” (or “ignorance”) of crowds. But it may be “profitable” to know when the “crowds views” begins to change towards the “correct wisdom”!

It's valuable to look back and analyze the course of N-gDp. The relationship between money and economic growth was textbook during C-19. It also represented a classic example of banks don't lend deposits, i.e., "flight to liquidity".

“Quantity leads and velocity follows”. Cit. Dying of Money -By Jens O. Parson

Hanke is supposedly an expert on the money stock. Not so. M2 is mud pie.

Means-of-payment money hit all-time highs in November 2020. Should have hit the brakes then.

The money stock can never be properly managed by any attempt to control the cost of credit. The FED may have lost control of the money stock in April 2024 (up $264b since Feb).

It's valuable to look back and analyze the course of N-gDp. The relationship between money and economic growth was textbook during C-19. It also represented a classic example of banks don't lend deposits, i.e., "flight to liquidity".

“Quantity leads and velocity follows”. Cit. Dying of Money -By Jens O. Parson

Hanke is supposedly an expert on the money stock. Not so. M2 is mud pie.

Means-of-payment money hit all-time highs in November 2020. Should have hit the brakes then.

The money stock can never be properly managed by any attempt to control the cost of credit. The FED may have lost control of the money stock in April 2024 (up $264b since Feb).