On Headline & Core Inflation

On Headline & Core Inflation

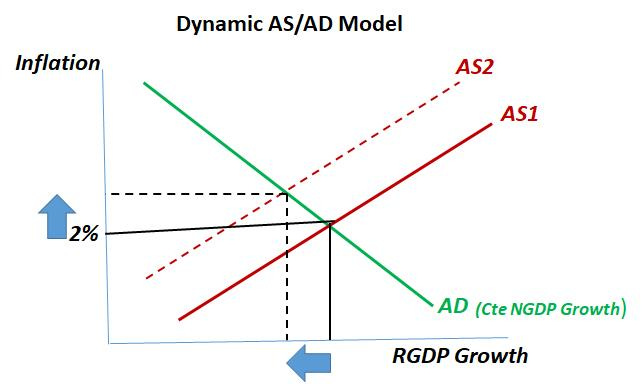

Shows how prone to error Inflation Targeting can be

Claudia Sahm put up a Q&A post. The last (and longer) answer is on Core vs Headline:

“Core inflation” is another important term THAT IS WILDLY MISUNDERSTOOD AMONG ECONOMISTS and thus confuses everyone…

That “confusion” is the best indicator that inflation targeting (IT) is a “bad” target. The graph below is a good illustration. It represents the Dynamic Aggregate Demand/ Aggregate Supply model. (The only observation I need to make is that the AD curve was drawn as a straight line for simplicity. It must be interpreted as a “Rectangular Hyperbola”, in which case every point on the curve gives the same AD (or NGDP) growth, say, 5%).

The graph is drawn to show the effects of a negative supply shock (increase in oil price, or fall in productivity growth, for example). This is the type of shock that puts the IT Fed in a bind. What to do? If the Fed reacts to the rise in inflation by “tightening” monetary policy, growth will fall by more (the recession will deepen) and unemployment will increase further.

The “best” outcome in such a case is for the Fed to keep AD, or NGDP, growth stable. That´s, however, hard to do if the Fed targets inflation and is afraid to lose its credibility if it allows inflation to rise.

That is exactly what happened in 2008. The second leg of the oil price rise that happened in 2007/08 “derailed” the Fed. This is clear in Bernanke´s summary of the June 2008 FOMC Meeting:

My bottom line is that I think the tail risks on the growth and financial side have moderated. I do think, however, that they remain significant.

We cannot ignore them. I’m also becoming concerned about the inflation side, and I think our rhetoric, our statement, and our body language at this point need to reflect that concern.

We need to begin to prepare ourselves to respond through policy to the inflation risk; but we need to pick our moment, and we cannot be halfhearted. When the time comes, we need to make that decision and move that way because a halfhearted approach is going to give us the worst of both worlds. It’s going to give us financial stress without any benefits on inflation.

So we have a very difficult problem here, and we are going to have to work together cooperatively to achieve what we want to achieve.

After that point, NGDP growth (which was already falling due to restrictive monetary policy) crashed, and RGDP growth (already negatively impacted by the oil shock), plunged the economy into the “Great Recession”!

From the perspective of the AS/AD graph above, the AD curve (NGDP growth) shifted strongly to the left.

Despite this “tragedy”, closely tied to the “inadequacy” of inflation targeting, just two years later, in May 2011, James Bullard, president of the St Louis Fed disparaged the concept of Core inflation in “Measuring Inflation: The Core Is Rotten”:

Many discussions of monetary policy, even within the central banking community, discuss movements of subsets of prices instead of the overall or headline measure of price changes.

The most famous subset is the “core”—all prices except those relating to food or energy. Core inflation is the measured rate of increase of these prices. Control of core inflation is not the goal of monetary policy, although it sometimes seems to be given the amount of emphasis put on this concept in the U.S.

In my remarks tonight I will argue that many of the old arguments in favor of a focus on core inflation have become rotten over the years. It is time to drop the emphasis on core inflation as a meaningful way to interpret the inflation process in the U.S.

One immediate benefit of dropping the emphasis on core inflation would be to reconnect the Fed with households and businesses who know price changes when they see them. With trips to the gas station and the grocery store being some of the most frequent shopping experiences for many Americans, it is hardly helpful for Fed credibility to appear to exclude all those prices from consideration in the formation of monetary policy.

There are several key arguments that are commonly used to favor a focus on core inflation in monetary policy discussions. I will argue that all of them are essentially misguided.

Because of this, the best the central bank can do is to focus on headline measures of inflation. The headline measures were designed to be the best measures of inflation available—the Fed should respect that construction and accept the policy problem it poses. Many other central banks have solidified their position on this question by adopting explicit, numerical inflation

It is not hard to show that Bullard´s arguments are wrong, and terribly so. The next set of charts show that very clearly.

Inflation, in this case consumer price inflation, means a continuous increase in general (or overall) index of consumer prices (here represented by the PCE (personal consumer expenditures)) index.

The top chart shows that over a long span of time (60 years with quarterly data) both the headline and core index give out the same information. Notice that during the “Great Inflation”, both indices rise steeply (meaning inflation is rising/high).

If the two indices give out the same information over time, if the Fed, although it targets headline inflation, bases its decisions on the behavior of core inflation, it does, or should do so systematically, because it is “convenient” (maybe by minimizing the chance of perpetrating gross monetary policy errors like it happened in 2008).

In the second chart, note that during the “Great Inflation” both the headline and core inflation rates increase continuously, satisfying the definition of “inflation”. That´s due to monetary policy being generally expansionary (from the perspective of the AS/AD graph above, it´s as if the AD curve is moving to the right).

The food and oil price shocks of the period had the effect of magnifying the inflation effects of those monetary shocks. These real (supply) shocks also change relative prices, so that headline inflation is higher than core inflation during those shocks.

The third chart reproduces the facts over the last three decades. Note that over the period, average headline and core inflation are almost exactly the same (and below the 2% target). Headline inflation, however, is much more volatile, widely “jumping” around, therefore much harder to hit!

In 2008, Bernanke´s Fed fell into the “headline trap”. It wasn´t supposed to happen because in 1997 Bernanke (with Gertler & Watson) had published “Systematic Monetary Policy and the Effiects of Oil Price Shocks”. Their conclusion:

Substantively, our results suggest that an important part of the effect of oil price shocks on the economy results not from the change in oil prices, per se, but from the resulting tightening of monetary policy. This finding may help to explain the apparently large effects of oil price changes found by Hamilton and many others.

To conclude, if the Fed will go on targeting inflation, don´t listen to Bullard, but be guided by core!

Kudos. One of the best economic blogs.

Irving Fisher was one of the best economists to ever live (Leland Pritchard was the best).

You can't explain inflation without the distributed lag effect of money flows.