Money Demand, the oft forgotten link

Money Demand, the oft forgotten link

What does excessive money growth mean?

After coming across talk titles such as these:

‘Is inflation caused by deteriorating inflation expectations or excessive money growth?’

On the 2020-21 surge in the amount of money and the return of inflation and ‘boom and bust’ cycles.

It was a ray of sunshine to read a sentence such as this one from Alexander Salter:

I’m personally skeptical that the demand-side factors are currently in the driver’s seat. You can’t infer the looseness of monetary policy from ongoing Fed purchases. Whether money is tight or loose depends on money supply relative to money demand. Velocity remains depressed, which means money demand remains elevated. Thus, the Fed’s “expansionary” activities could just be appropriate monetary policy.

To put a damper on the “obsession” with inflation expectations, these two sentences from Jeremy Rudd´s “Why do we think inflation expectations matter for inflation? (And should we?) should do the job:

[By] telling policymakers that expected inflation is the ultimate determinant of inflation´s long-run trend, central bank economists implicitly provide too much assurance that this claim is a settled fact. Advice along these lines also naturally biases policymakers toward being overly concerned with expectations management, or toward concluding that survey or market-based measures of expected inflation provide useful and reliable policy guideposts. And in some cases, the illusion of control is arguably more likely to cause problems than an actual lack of control.

Related to this last point, an important policy implication would be that it is far more useful to ensure [à la Greenspan] that inflation remains off peoples radar screens than it would be to attempt to ‘re-anchor’ expected inflation at some level that policymakers viewed as being more consistent with their stated inflation goal.

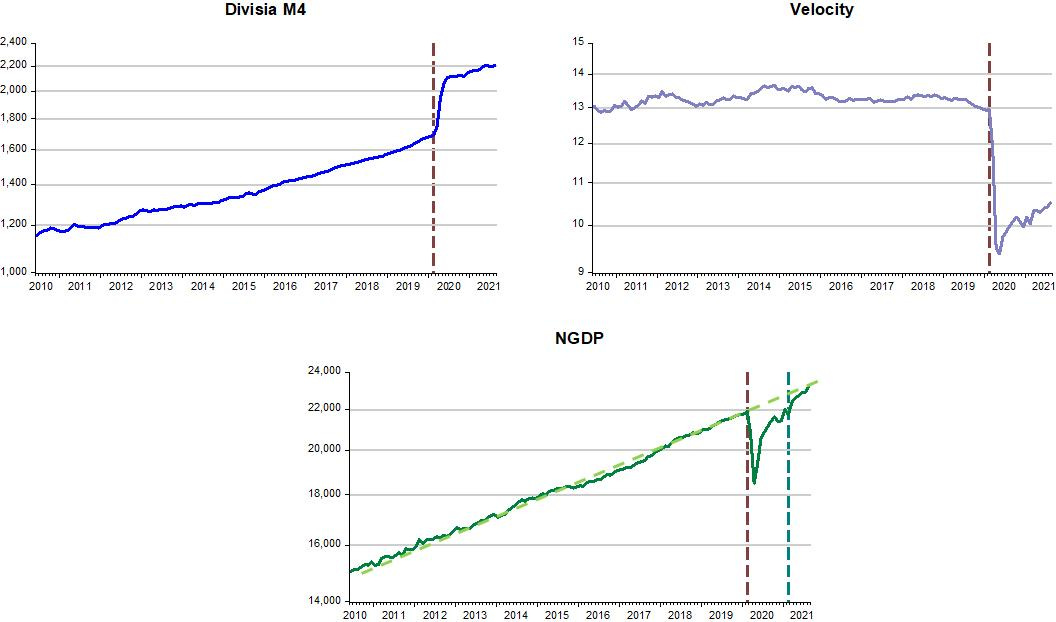

And now to “excessive” money growth. What is “excessive”? Maybe “excessive” refers to the fact that after rising for close to 4% YoY for 10 years, in a handful of months from February to July 2020, money supply growth jumped to 30% YoY!

However, as Alexander Salter reminds us, you have to gauge money supply relative to money demand. To economize on words, the charts illustrate.

Before Covid19 hit, broad money supply (Divisia M4) rises along a smooth stable trend (near 4% YoY). Velocity (inverse of money demand) is stable (near 0% YoY). Putting “two & two” together, from the equation of exchange in growth form (m+v=p+y), since m~4%, v~0%, we get that p+y, or NGDP growth ~4%.

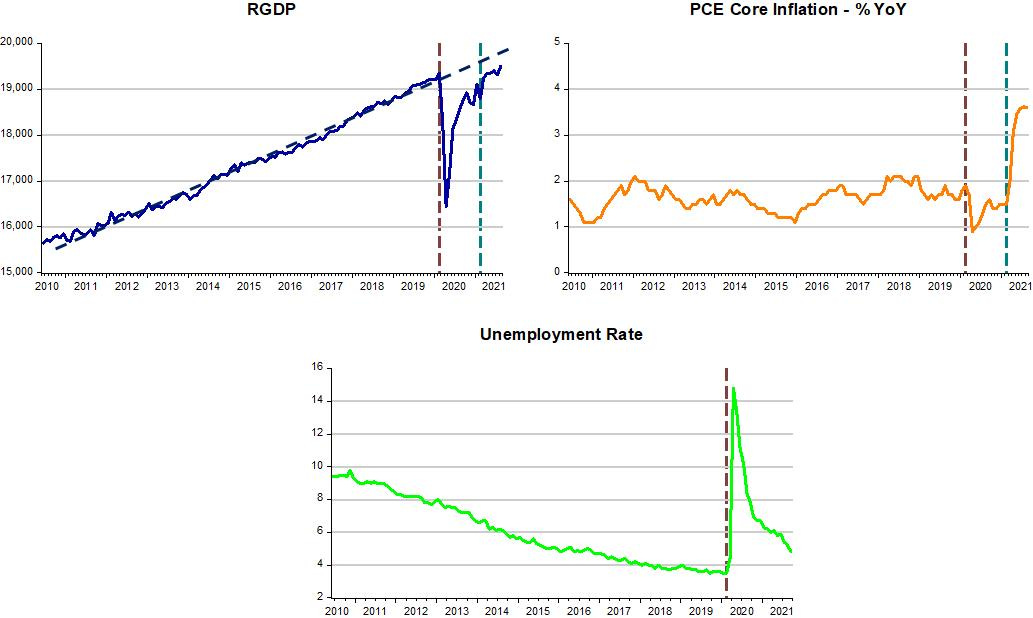

During the 2010s, therefore, the US economy enjoyed a measure of Nominal Stability. One implication of nominal stability is that both output growth and inflation are stable. (A consequence of nominal stability is that the rate of unemployment shows a declining trend).

As the next charts show, real output (RGDP) climbs at a rate a bit above 2% YoY while inflation remains stable averaging a little below 2% YoY. Unemployment falls throughout.

Covid19 throws a monkey-wrench into the system. Velocity tanks (money demand skyrockets). Money supply growth reacts with a delay, sufficient to “drown” NGDP (and RGDP) and propel unemployment to “wuthering heights”. Even inflation takes a hit!

As soon as money supply “catches up” to money demand, things began to accommodate. NGDP begins the trip back to the pre-Covid19 trend path, RGDP picks up, unemployment falls while inflation remains contained. I just imagine what would have transpired if the “excessive money growth spells inflation” crowd had been in charge!

After March 22 (to the right of the second bar in some charts), inflation begins to rise. Where is that coming from? Two things to note:

NGDP closes up on the trend path

The rise in RGDP stalls due to supply bottlenecks

The “slack” is picked up by inflation.

We face a supply side inflation, a combination of a classic supply shock (energy & food) and Covid19 induced supply bottlenecks. Meanwhile, nominal expenditures are set to remain close to the trend path. In a supply shock inflation the Fed does best to keep NGDP on the trend path because otherwise it will produce unwanted nominal instability.

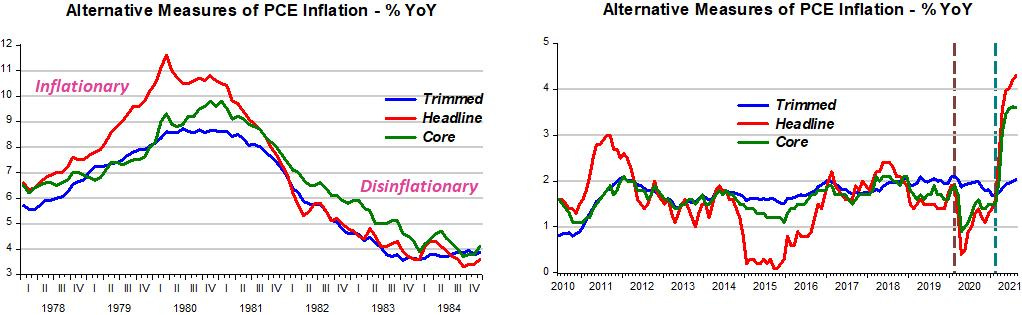

To make sense of what´s happening, I examine three alternative measures of PCE inflation. The “headline” variety which considers all prices in the index, the “core” measure, which strips out prices of food & energy, and the “trimmed” measure, where a certain fraction of the most extreme observations at both ends of the spectrum are thrown out or “trimmed”.

During inflationary and disinflationary times, they all show comparable trends, as shown in the LHS chart below. When inflation is stable (RHS chart), the most volatile component is the headline variety, which reflects the “classic” supply shocks, with both core and trimmed measures fluctuating close together.

When supply bottlenecks hit (in addition to oil/food shocks), the “compatibility” of the core and trimmed measures is lost. While the LHS chart is consistent with the definition of inflation (disinflation) as an increase (decrease) in the rate of the overall level of prices, over the last 6 months, while the rate of core price increase has gone up, the trimmed (“super core”) measure has stayed “put”.

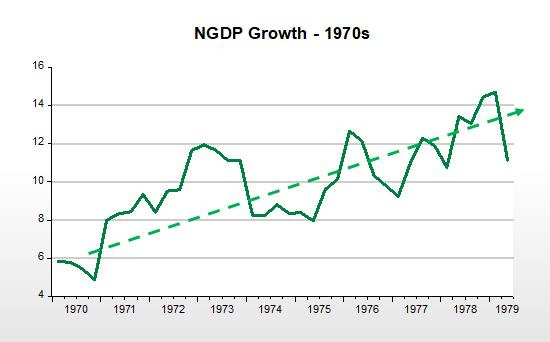

This tells us that the inflation that people talk about is not as generalized as the proper definition of inflation requires! In fact "a “classic inflationary process” cannot happen if NGDP growth is stable. For that, like in the 1970s, NGDP growth has to be trending up.

To “wait-out” the supply bottlenecks resolution, the best the Fed can do is to keep NGDP evolving stably along the trend path its on. If the Fed “worries” about inflation and “cramps” aggregate nominal spending through misguided monetary policies it will, once again, regret the action later!

PS Krugman has a clear and simple argument to resolve supply bottlenecks. In addition to saving lives, it will spare the Fed the risk of making costly mistakes!

But the biggest thing that could bring fast relief would be undoing the skew in demand by making people feel safe buying more services and fewer goods. The way to do that is by getting the pandemic under control, above all by getting more people vaccinated.