Monetary Mechanics

Monetary Mechanics

Explaining the different outcomes following the Great Recession & Covid-19

The question I will discuss is quite straightforward: Why, given an even more intense asset purchase by the Fed (QE) in 2008/09, there was no inflation following the Great Recession while inflation rose significantly in 2021/22?

Although there was no increase in inflation following the Great Recession, many notable names, for different reasons, feared that it would happen. Some examples:

The US last week showed its first signs of deflation for 55 years, prompting inevitable fears of further deflation in the future. Yet the primary reason for the negative rate of US inflation is the dramatic 30 per cent fall of commodity prices. That will not happen again. Moreover, excluding food and energy, consumer prices are up 1.8 per cent from a year ago. That is the good news: the outlook for the longer term is more ominous.

Martin Feldstein six years later in May 2015 repeats the mantra (introducing wages given that unemployment had been reduced significantly - from 10% to 5.2%):

…The higher wage costs are not showing up yet in overall inflation because of the countervailing impact of energy prices and import costs. But as these temporary influences fall away in the coming year, overall price inflation will began to increase more rapidly.

From Alan Meltzer in May 2009:

…Besides, no country facing enormous budget deficits, rapid growth in the money supply and the prospect of a sustained currency devaluation as we are has ever experienced deflation. These factors are harbingers of inflation.

When will it come? Surely not right away. But sooner or later, we will see the Fed, under pressure from Congress, the administration and business, try to prevent interest rates from increasing. The proponents of lower rates will point to the unemployment numbers and the slow recovery. That’s why the Fed must start to demonstrate the kind of courage and independence it has not recently shown.

From Alan Greenspan: Inflation - the real threat to sustained recovery June 2009:

For the benevolent scenario above to play out, the short-term dangers of deflation and longer-term dangers of inflation have to be confronted and removed. Excess capacity is temporarily suppressing global prices. But I see inflation as the greater future challenge. If political pressures prevent central banks from reining in their inflated balance sheets in a timely manner, statistical analysis suggests the emergence of inflation by 2012; earlier if markets anticipate a prolonged period of elevated money supply. Annual price inflation in the US is significantly correlated (with a 3½-year lag) with annual changes in money supply per unit of capacity.

From the St Louis Fed in October 2012:

The recent expansion in the monetary base (currency in circulation and bank deposits), brought about by the Federal Reserve's quantitative easing measures, has stoked fears of high inflation. Critics argue that by flooding the economy with massive amounts of liquidity—by expanding its balance sheet—the Fed may have set the stage for a possible surge in the future price level

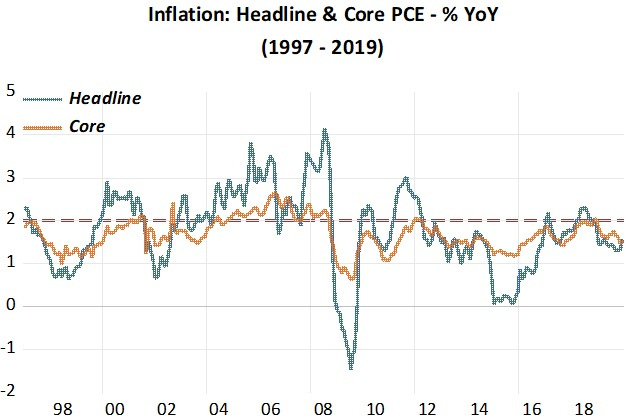

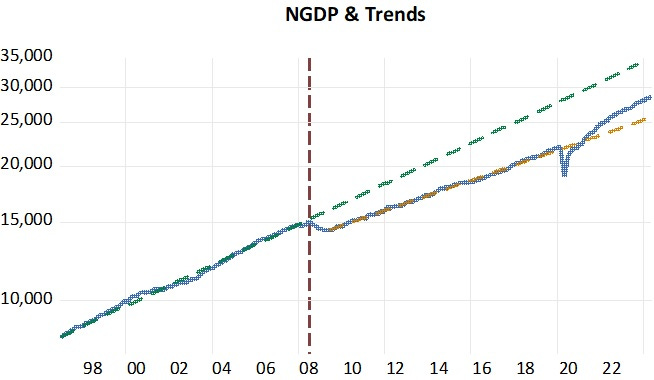

So what really happened to inflation from the decade before to the decade after the Great Recession? The chart illustrates.

Not only inflation did not increase, it was actually lower than during the decade before the Great Recession!

John Williams at the time president of the San Frncisco Fed wrote in July 2012: Monetary Policy, Money, and Inflation

…These purchases [QEs] increased the demand for longer-term Treasuries and similar securities, which pushed up the prices of these assets, and thereby reduced longer-term interest rates. In turn, lower interest rates have improved financial conditions and helped stimulate real economic activity.

The important point is that the additional stimulus to the economy from our asset purchases is primarily a result of lower interest rates, rather than a textbook process of reserve creation, leading to an increased money supply. It is through its effects on interest rates and other financial conditions that monetary policy affects the economy.

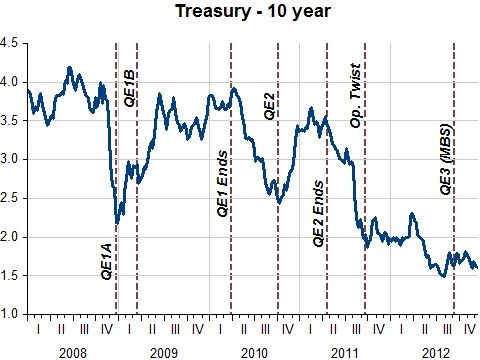

Reality was very different. As this old chart shows, at every new QE program long-term interest rates would increase, falling when the program was “ended”! This reflects the fact that an increase in QE improved expectations of a rise in future economic activity, increasing rates.

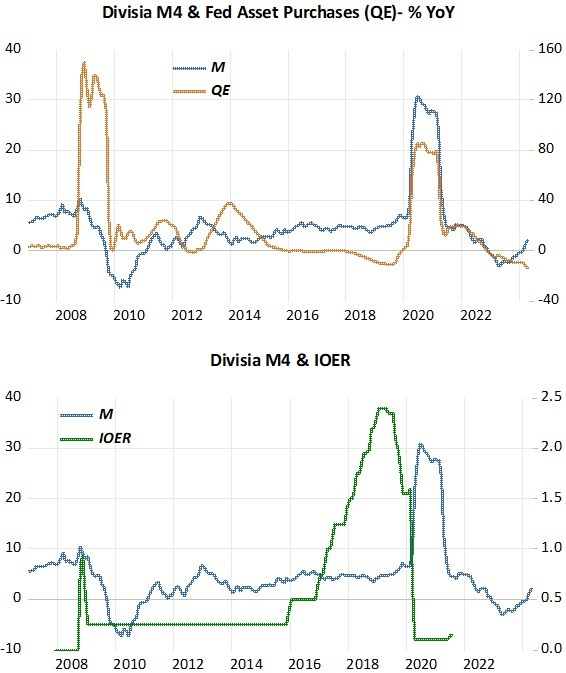

The next chart indicates that Williams´ view of monetary policy is wrong! By introducing the payment of interest on excess reserves (IOER) in October 2008, the Fed in effect “blocked” the “textbook process of reserve creation”, inducing by that action a fall in money supply growth (and a drop in the level of the money stock) thus condemning the economy to remain “depressed”. The “blocking effect” of IOER is what Greenspan and the others failed to take into account when “fearing inflation”!

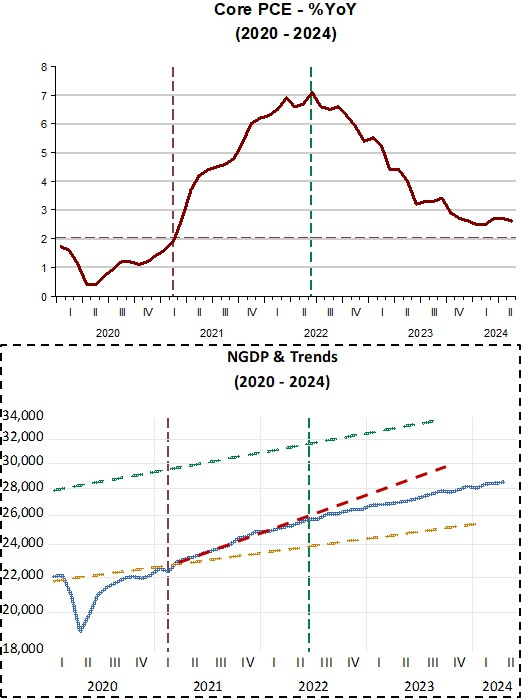

By contrast, in 2020, with the Fed quickly getting rid of IOER, money supply growth quickly rose. This time around, it´s not surprising that the economy reacted quickly. The recession, although one of the deepest, was also the shortest on record, with a full recovery accomplished inside 12 months!

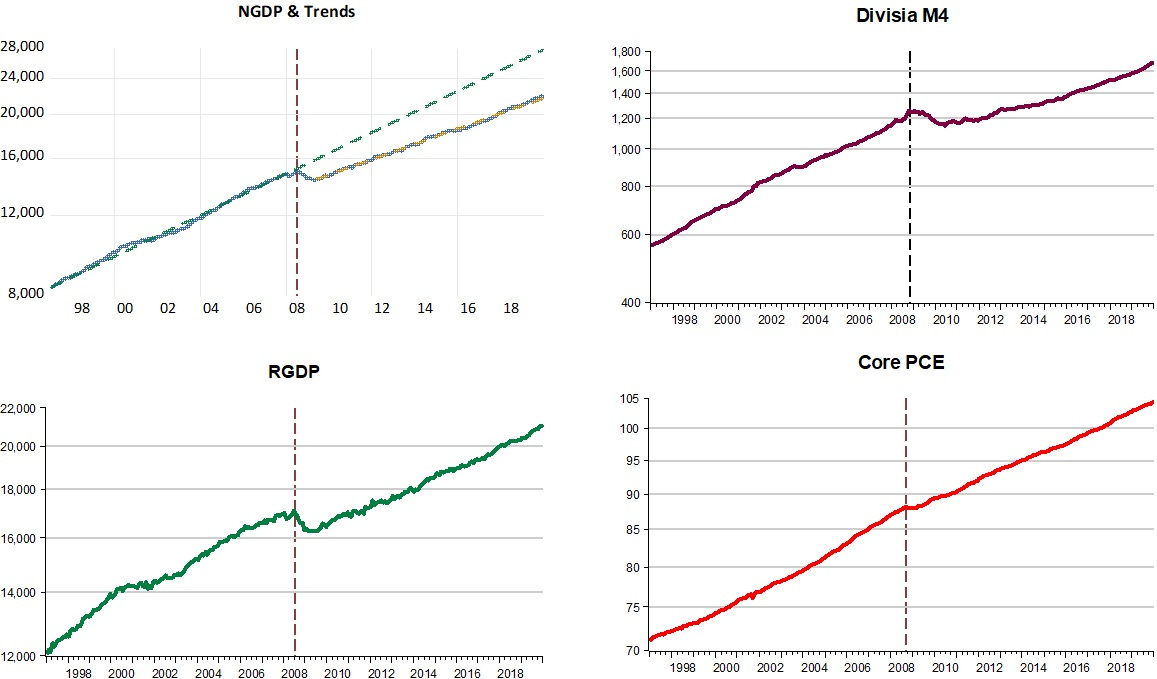

The panel below is strong evidence against Williams´view on “additional stimulus”, showing that in effect the Fed´s “monetary policy” condemned the economy to a “depressed expansion”. The breaks in all the series happen at about the same time and even with the Fed keeping interest rates at very low (close to zero) levels, the economy remained depressed (rising along a lower level path). That´s true even for the price level series.

The next chart is proof that Williams´assertion that

The important point is that the additional stimulus to the economy from our asset purchases is primarily a result of lower interest rates, rather than a textbook process of reserve creation, leading to an increased money supply. It is through its effects on interest rates and other financial conditions that monetary policy affects the economy.

is wrong. Since now there was no IOER “blocking” the monetary impact from QE, aggregate nominal spending (NGDP) recovers quickly, being back on the post GR trend line by early 2021. In both instances, “zero rates ruled”, so it must have been the increased money supply in 2020 that is responsible for the diametrically opposite outcomes. This is one more evidence that interest rates do not define the stance of monetary policy. The stance of monetary policy is better defined by the behavior of NGDP.

Interestingly macroeconomic outcomes are never the result of monetary policy choices, but always the result of “fortituous” events. Just as the Great Recession was the result of a financial crisis (induced by the crash in house prices), the increase in inflation after C-19 was the outcome of supply shocks.

The next charts show that, on the contrary, it is the Fed choices that determine outcomes. Note that inflation only rises when monetary policy becomes expansionary, indicated by the fact that NGDP rises above the post GR trend path. Note also that inflation begins to fall when the NGDP growth trend flattens, a clear indication that monetary policy became less expansionary.

Why did the Fed choose to pursue an expansionary policy in early 2021? A few months earlier the FOMC had adopted a new strategy for monetary policy called Flexible Average Inflation Target (FAIT), that would require that if inflation remained below 2% for a time it would have to rise above 2% for a time to bring average inflaation to 2%.

In early 2021, the Fed decided to “improve” the labor market. A February 2021 speech by Powell was entitled “Getting back to a strong labor market”. The FOMC´s Phillips Curve mentality felt that the resulting increase in inflation above 2%, given that inflation had for long been below 2%, would be consistent with its new strategy!

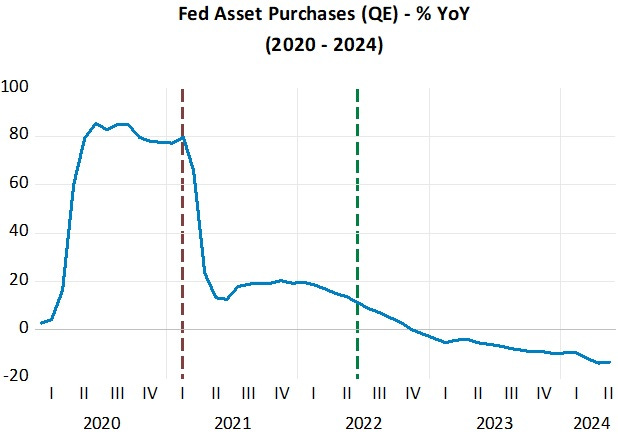

The chart below indicates that monetary policy became expansionary after early 2021 because the Fed did not reduce the pace of asset purchases (QE) fast enough, thus not allowing money supply growth to fall sufficiently to offset the rise in velocity that was taking place.

Over the past two years, QE has fallen more consistently even becoming negative (quantitative tightening). Not surprisingly, NGDP growth and inflation have fallen. The small “excess inflation” still present is mostly to quirks from owners equivalent rent that will be “disposed off” in the near future.

The Fed, however, measures the stance of monetary policy by looking at interest rates and inflation, leading to at least a few FOMC members to want to keep rates higher for longer with some even contemplating another increase since there´s still a bit of excess inflation to be “purged”!

It is always by looking at the economy through the wrong lense that the Fed makes mistakes, resulting in either an increase in inflation or a fall in economic activity (increased unemployment).

Let´s hope they come to their senses soon.

If you'd write a book I'd read it.

If the Fed were in fact looking only at inflation (and taking account of the holding quirk,) AND they were willing to zig as well as zag, AND they valued real growth more and feared the risk of undershooting inflation more, they WOULD be readjusting their QT and EFFR instruments. All three errors are affecting their decision making.