Looking for patterns

Looking for patterns

As some believe, has the economy entered a recession?

How quickly views change! Until just “the other day”, labor markets were “too tight” and there was no urgency for the Fed to lower rates. Now, the labor market is weakening rapidly and the Fed must start the rate lowering process, and it should start with a 50 bp cut!

This made more urgent because in August, the Sahm rule triggered! There is more:

This month, the French-born economists Pascal Michaillat and Emmanuel Saez introduced a variant of the Sahm indicator that adds declines in the job vacancy rate. By their reckoning, according to data through July, “the probability that the U.S. economy is now in recession is 40 percent,” and “the recession may have started as early as March 2024.”

Peter Coy commenting on a paper presented at Jackson Hole (The latest incantation of the Phillips Curve):

Benigno and Eggertsson analyzed 111 years of U.S. economic history, including six major surges in inflation. They found that in a tight labor market (more vacancies than job seekers), the vacancy rate tends to shoot up even when the jobless rate declines only a little. Also, it takes only a small increase in economic activity to produce a big burst in inflation. (In economists’ terms, the Phillips curve suddenly steepens.) In a loose labor market (more seekers than vacancies), it’s the opposite: It takes a big decline in economic activity to bring inflation down just a little…

…As for current monetary policy: If the economy gets softer from here and we’ve passed beyond the Beveridge threshold, the unemployment rate could rise considerably more than it has so far. They say it’s also possible — but less likely — that their calculations are wrong and the labor market is still fairly tight, making it more vulnerable to an inflation spike.

Between the two risks of high unemployment and high inflation, we’ve been focused for three years on the latter, and understandably so. But if Benigno and Eggertsson are right — and I think they are — it’s unemployment we should be more worried about now.

It appears we never learn. By always keeping a version of the Phillips Curve as the main guide to monetary policy (in fact interest rate) decisions, thus alternating between concerns with inflation and unemployment, the Fed “enhances” business cycle fluctuations.

The question I want to address is: “is the labor market indicating the economy is weakening”? My answer will be No. To reach that answer, I look, not at the rate of unemployment (u) but at its determinants, the Employmet/Population ratio (EPOP) and the Labor Force Participation Rate (LFPR), with u=1-(EPOP/LFPR).

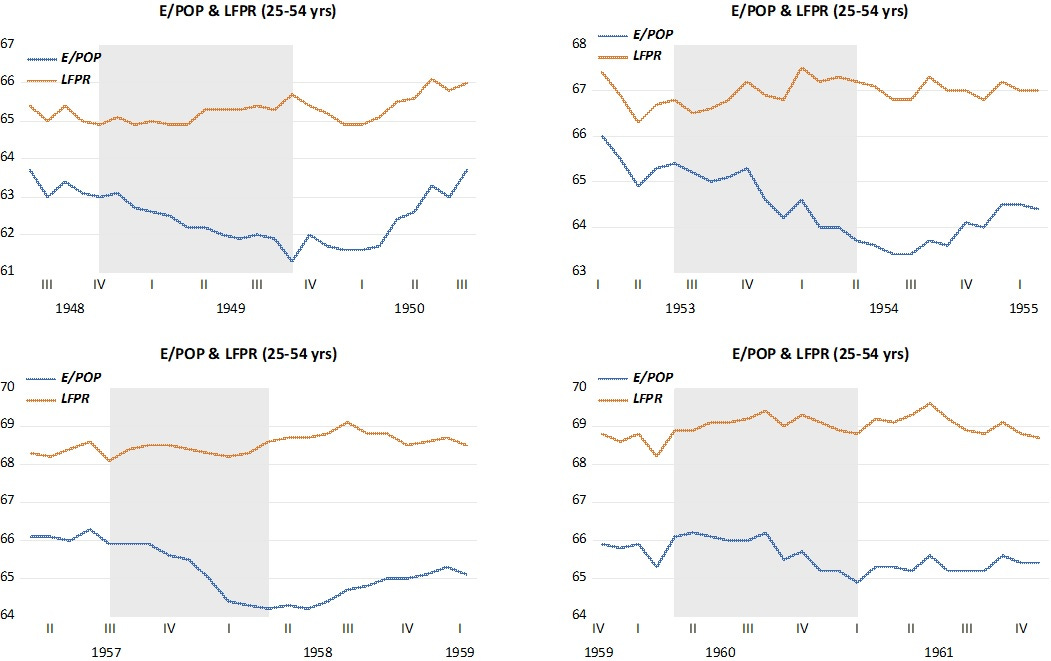

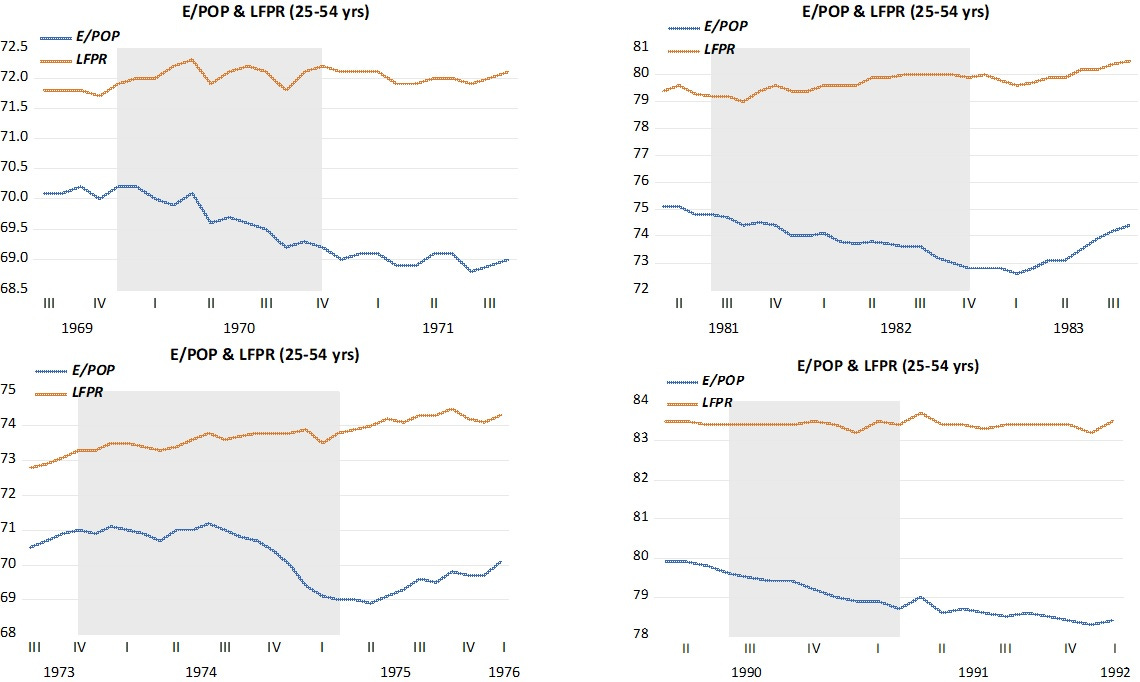

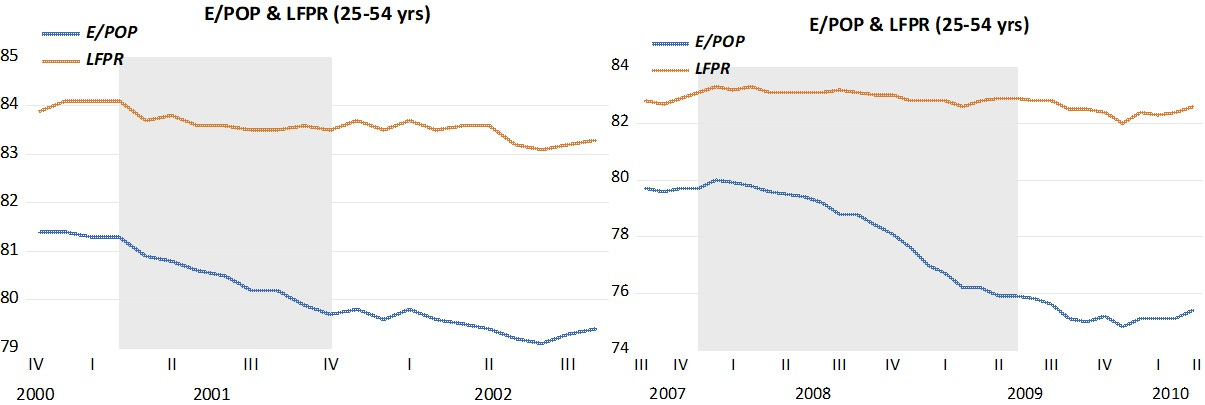

The set of charts below show what was happening to EPOP and LFPR around the post war recessions, beginning 4 months before the recession started and extending to 10 months after the recession ended.

A general feature of these charts is that, while the LFPR does not move much during the period, the EPOP always falls, but with different degrees of intensiveness.

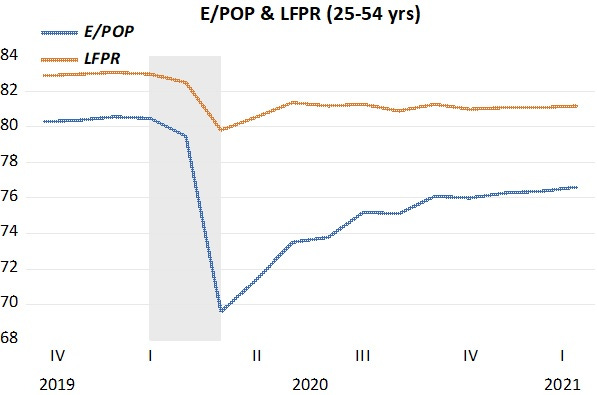

The next chart shows the 2020 (C-19) recession. The pattern is very different, with both LFPR and EPOP falling very quickly and significantly (but the rebound is also quick and significant).

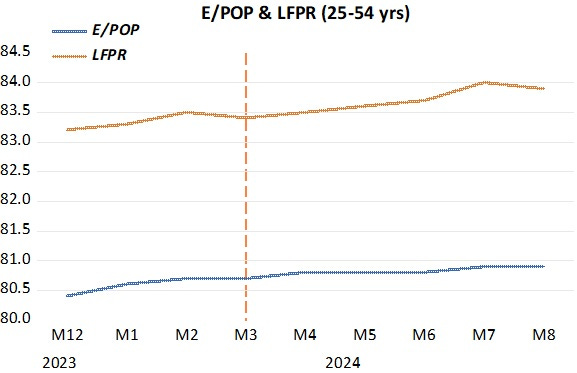

The next chart depicts the last 9 months. It´s very unlikely that the economy is in a recession (the “likely” start in March is marked by the vertical red dotted line). It´s nothing like the pattern observed for all pre C-19 recessions. Both EPOP and LFPR are rising (and when LFPR rises by more than EPOP as observed in July, unemployment rises. But that´s not a sign that the labor market is weakening). Maybe the opposite is true!

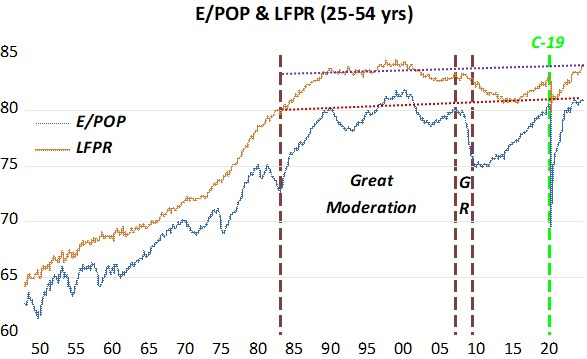

The next chart shows the behavior of EPOP and LFPR for the whole post WWII period. Two things to notice: The increase of women in the labor force in the 1970s and the peaking of both the EPOP and LFPR in the 1990s. Note that at present both EPOP and LFPR are at or very close to the peaks observed in the 1990s (high point of the Great Moderation). In that sense, at present the labor market is healthy!

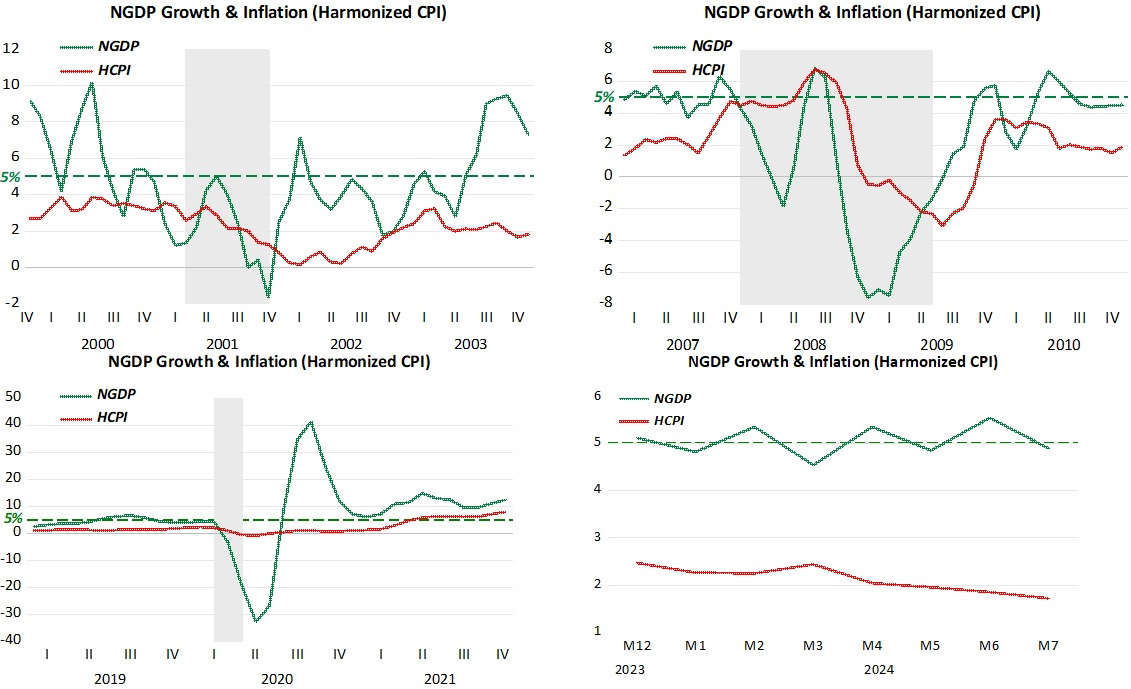

For those still in doubt about the economy being in or close to a recession, the next charts tackle the question from a Market Monetarist perspective. For market monetarists the best indicator of the stance of monetary policy is not the interest rate but the behavior of aggregate nominal spending (NGDP) growth.

A recession, from this perspective will only happen if NGDP growth falls, either significantly, strongly or massively. All the other post war recessions (not shown) satisfy this condition.

It is quite clear that at present this condition is not satisfyied at all! After dropping strongly from “wuthering heights”, obtained to compensate the massive drop in NGDP growth when C-19 hit, NGDP growth has stabilized close to 5%. Inflation (excluding OER) has remained stable and close to target (with monetary policy remaining stable, headline inflation will also continue to fall. By positively affecting the housing market, that´s where a drop in interest rates will have the most impact).

People say that “to reduce inflation, unemployment has to rise”. However, it is the Fed, through its control of NGDP growth that affects inflation and unemployment.

That´s the best argument for having the Fed ditch its interest rate targeting procedure and concentrate instead on stabilizing NGDP growth! Participants will quickly realize that “operating the market” has become much less stressful!

The increase in MMMFs is an increase in the supply of loanable funds, but not the supply of money. I.e., it is a velocity relationship. Consequently, the demand for money is falling / velocity rising.

https://www.zerohedge.com/markets/money-market-fund-assets-hit-another-new-record-high-domestic-bank-depos-surge-pre-svb

EPOP and LFPR are affected by immigration. With the recent large influx, there might be some inconsistencies?

Long-term money flows, the volume and velocity of money, are decelerating. Short-term money flows, the proxy for the real output of goods and services, doesn't show much deceleration now until the 1st qtr. of 2025.