"Kernels of Truth"

"Kernels of Truth"

Those instances when inflation remains low & stable and unemployment falls

More than 60 years ago, A .W. Phillips, a New Zealand economist working out of the London School of Economics, “established” an empirical relationship between the rate of unemployment and the rate of change of money wages. The paper, “The Relation between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861-1957”, was published in the journal Economica in 1957.

Based on the pricing assumption of a constant mark-up over wage costs, the Phillips Curve was transformed into a relationship between unemployment and inflation…and began doing its damage!

So the reader has an idea about the importance of the Phillips Curve concept in the Fed´s policy making apparatus, this is from one of the first speeches made by Laurence Meyer in April 1997, shortly after being made Fed Governor (the FOMC had increased the FF rate by 25 basis points in March, after rates having been left unchanged for a little over one year):

…So let me be specific about the causal structure of the model that underpins my judgment with respect to appropriate monetary policy action.

I am a strong and unapologetic proponent of the Phillips Curve and the NAIRU concept. Fundamentally, the NAIRU framework involves two principles.

First, the proximate source of an increase in inflation is excess demand in labor and/or product markets. In the labor market, this excess demand gap is often expressed in this model as the difference between the prevailing unemployment rate and NAIRU, the non-accelerating inflation rate of unemployment.

Second, once an excess demand gap opens up, inflation increases indefinitely and progressively until the excess demand gap is closed, and then stabilizes at the higher level until cumulative excess supply gaps reverse the process.

And he goes on to say (my bold):

There is a third principle that I subscribe to, which, though not as fundamental as the first two, also plays a role in my forecast and in my judgment about the appropriate posture of monetary policy today.

Utilization rates in the labor market play a special role in the inflation process. That is, inflation is often initially transmitted from labor market excess demand to wage change and then to price change.

This third principle may be especially important today because, in my view, there is an important disparity between the balance between supply and demand in the labor and product markets, with at least a hint of excess demand in labor markets, but very little to suggest such imbalance in product markets.

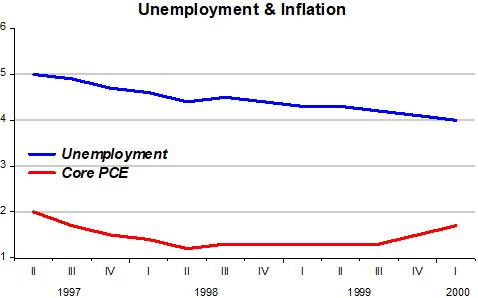

And the chart shows what happened to unemployment and inflation in the three years following Meyer´s speech.

At least one FOMC member, William Poole, President of the St Louis Fed learned something from that period. In the June 2000 FOMC Meeting he made what is to me, one of the most insightful comments in FOMC Meetings history:

The traditional NAIRU formulation views the wage/price process as running off a gap–a gap measured somehow as the GDP gap or the labor market gap. And the direction of causation goes pretty much from something that happens to change the gap that feeds through to alter the course of wage and price changes.

I think there is an alternative model that views this process from an angle that is 180 degrees around. It says that in an earlier conception, monetary policy pins down the price level or the rate of inflation and, therefore, expectations of the rate of inflation.

Then the labor market settles, as it must, at some equilibrium rate of unemployment. Where the labor market settles is what Milton Friedman called the natural rate of unemployment.

But the causation goes fundamentally from monetary policy to price determination and then back to the labor market rather than from the labor market forward into the price determination. I certainly view the causation in that second sense.

Now, the labor market has been clearing at a level that all of us have found surprising. But I don’t think that necessarily has any particular implication for the rate of inflation, provided we make sure that we are willing to act when necessary. (pg 61).

While to Meyer, the labor market plays an “active role” in the inflation process:

Utilization rates in the labor market play a special role in the inflation process. That is, inflation is often initially transmitted from labor market excess demand to wage change and then to price change.

To Poole, the labor market plays a “passive role”, dependent on the “quality” of the monetary policy being pursued by the Fed:

Then the labor market settles, as it must, at some equilibrium rate of unemployment. Where the labor market settles is what Milton Friedman called the natural rate of unemployment.

Falling/“Low” unemployment, then, is not a harbinger of rising inflation but a testimony to high quality monetary policy.

How can we define “high quality monetary policy” (HQMP)? Many would say it is one that keeps inflation low & stable. But the Fed is also concerned about “full employment”. In that case, a HQMP would be one that kept both inflation and unemployment low. Since the Fed can only influence nominal quantities, the best it can achieve is overall nominal stability (or stable NGDP growth).

Can we infer from the data when the Fed was practicing HQMP (those instances when unemployment came down & down without any manifestation of rising inflation)?

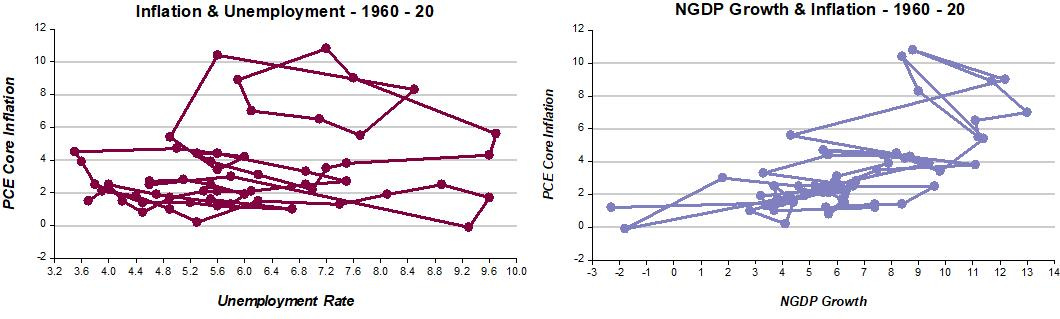

Given the “cobweb” nature of both the Phillips Curve and NGDP growth - Inflation relationship shown in the charts below, this is not evident. That means that overall, during the last 60 years, monetary policy left much to be desired.

Note that while no significant correlation can be discerned between inflation and unemployment, there appears to be a significant positive correlation between NGDP growth (which is the better gauge of the stance of monetary policy) and inflation. This would be expected if you subscribe to the view that inflation is a monetary phenomenon.

"Diving inside the webs” above, I find two relative long periods (1992 - 00 & 2010 - 19) when unemployment was falling to historically low levels while inflation remained low & stable. That implies that during those times, monetary policy was ‘high quality”. In other words, NGDP growth was stable.

In between those two periods, you see what happens when monetary policy goes far astray. When NGDP growth tanks (goes negative), unemployment skyrockets while inflation falls much less. That´s because inflation expectations around 2% had been “solidified”.

Note that, with negative growth, the level of NGDP fell. When stable NGDP growth resumed in 2010, it did so a a lower rate than during the previous 20 years, implying that the original level of NGDP was never recovered.

The importance of the NGDP Level (in addition to the stable growth rate) becomes clear when you read the recent comments from Board Members such as Lael Brainard:

…I will be looking for indicators that show the progress on employment is broad based and inclusive rather than focusing solely on the aggregate headline unemployment rate…

In other words, the “quality” of the labor market depends on the Level Path along which NGDP growth is stable.

In 2019, Powell and the “gang at the Fed” “discovered” that the Phillips curve was flat! After all, unemployment was at rates last seen 50 years ago without any inducement for inflation to rise.

As a friend recently put to me:

“He [Powell] does not have confidence in Board staff forecasts of inflation based on the Phillips curve. He does have confidence in his ability to control inflation based on the assumption of a flat Phillips curve with an upward sloping section starting at a very low rate of unemployment. Keynesian hubris”

Which leads to “creative poems” on Tweeter following yesterday´s FOMC Meeting results:

“Will you hike if yields rise?”

“We will not hike if yields rise.

We will not catch you by surprise.

We will not hike on Phillips Curve

We will not hike if prices swerve.

Not when inflation gets to 2,

Not when U3 hits NAIRU.

Do not ask me any more! Full employment, not before!”

What Powell and the Fed don´t get is that a flat Phillips Curve is not an assumption but the outcome of a HQMP. They have important choices to make, but the answers will not come from studying the problem from a unemployment/inflation perspective, but from, as I argued here, an NGDP Level & growth perspective.