Is Monetary Policy Democrat or Republican?

Is Monetary Policy Democrat or Republican?

Neither, just good or bad & sometimes mediocre

As the moment that President Biden has to appoint a Fed Chair approaches, there are pro & con voices with regards to the reappointment of Jay Powell. Some examples:

Alan Cole: “Replacing Powell would be a blunder for Biden”

Maia: “Some have suggested not reappointing the Fed Chairman. I think that's a terrible idea.”

Mathew Yglesias: “Full Employment is the most important thing the Fed can do to fight climate change”

All these are Pro, with Yglesias arguing both sides of the question.

Here I want to concentrate on the very incisive Con:

Bradford Delong: “Will Biden Make a Historic Mistake at the Fed?” and provides a competing name:

The past 30 years should have taught Democrats to put their own economic policy priorities before symbolic gestures of "bipartisanship." If US President Joe Biden does not replace Federal Reserve Chair Jerome Powell with Lael Brainard, he will almost certainly regret it.

I highlight this passage in particular:

When Greenspan retired in January 2006, he was succeeded by Ben Bernanke, a Bush appointee who impressed Democratic President Barack Obama with his willingness to work on a bipartisan basis to push the perceived limits of monetary policy in fighting the Great Recession. In 2009, Obama duly reappointed Bernanke, who held the line by continuing the Fed’s quantitative-easing (QE) policies despite howls of outrage from Republicans.

You cannot be more misleading! In fact, it was the Bernanke Fed´s monetary policy that promoted the Great Recession.

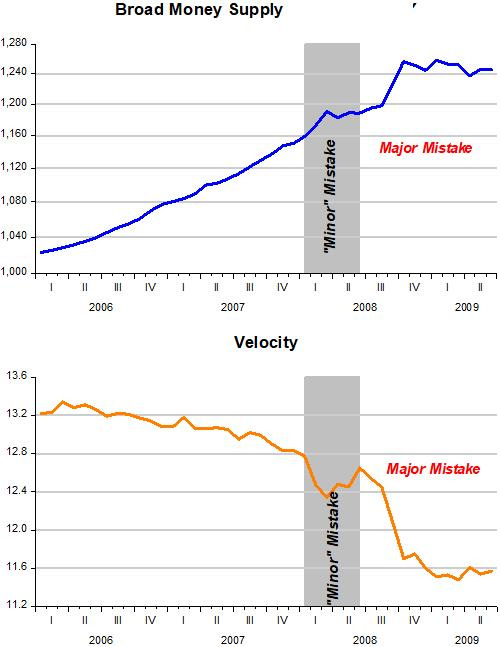

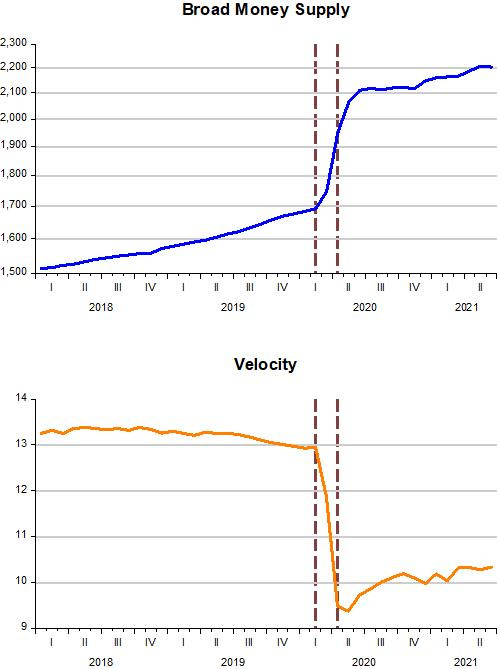

The best monetary policy can do is achieve nominal stability. For that, the central bank has to conduct monetary policy (change the supply of money) so as to offset changes in velocity.

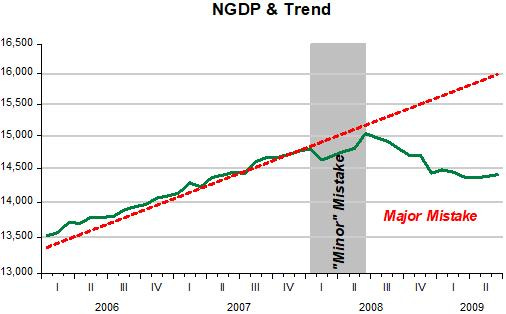

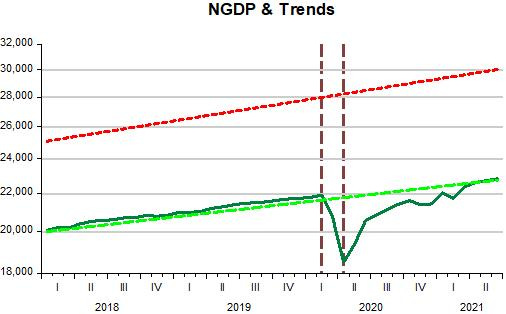

The three charts below illustrate. During the first two years of his tenure, Bernanke conducted monetary policy appropriately offsetting changes in velocity with changes in the supply of money. The result was that NGDP (or aggregate nominal spending) evolved closely along the Great Moderation stable trend level path.

In late 2007, worried about the oil shock effect on inflation, the Fed tightened monetary policy, with NGDP dropping below trend. This was a “minor” mistake that was in the process of being corrected when the Fed “blundered” with a major mistake!

So it´s a bit of a stretch to read that Bernanke was set to “push the perceived limits of monetary policy in fighting the Great Recession” when all the Fed did was implement the worst monetary policy since the Great Depression!

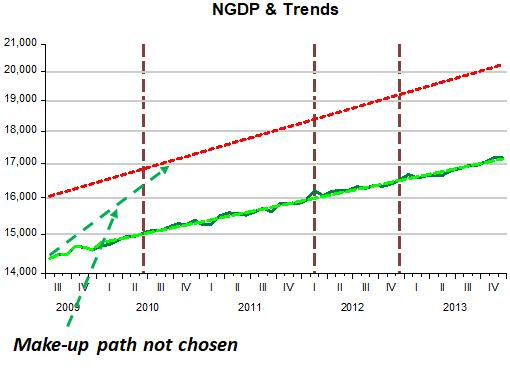

Thereafter, the Fed never tried to compensate for the “blunder”, conducting monetary policy so as to keep the economy evolving stably along a depressed level path.

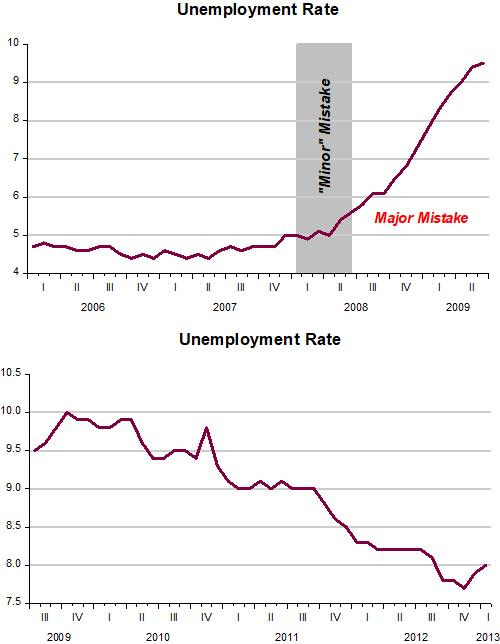

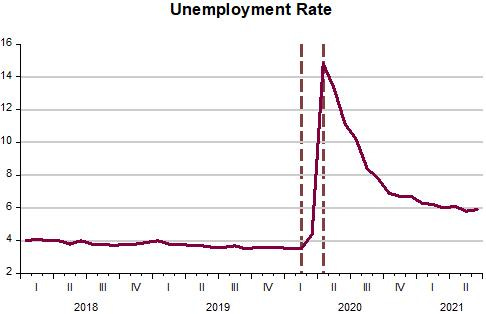

The outcome of those monetary policy decisions was that after rising high & fast, unemployment fell slowly, still clocking 9% more than two years after the end of the Great Recession!

The Powell Fed, different from the Bernanke Fed, did not cause the Covid19 recession. Since it was not Powell´s “fault”, he had “nothing to hide” (see the Appendix), so monetary policy had “free rein”.

The Covid19 was a supply shock with massive demand implications. Velocity tanked (money demand skyrocketed). But we note that monetary policy reacted quickly and soon NGDP was on the way back to the post Great Recession trend path.

In the Spring/Summer of 2020, many were writing that money supply growth was excessive and would bring about a significant increase in inflation in 2021, with some even predicting inflation as high as 12%!

Supply bottlenecks still persist and new variants of the virus impact labor market supply. That´s one reason for unemployment, after falling fast, to still remain relatively elevated.

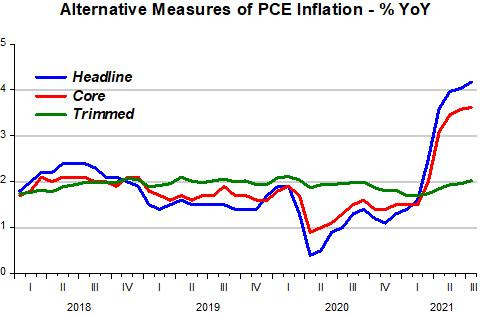

The “inflation problem” is still more of a “specific prices” problem”. The increases are associated with the lingering supply bottlenecks which are expected to dissipate. The trimmed mean PCE, a “super core” measure remains very well behaved.

Powell´s stated objective (when he shows concern with the labor market and redefines the concept of “maximum employment”), is to take NGDP to a higher trend level path. He also seems to understand that this has to be done with care, given the distortions from the pandemic still present. So there is no evidence that, according to Delong´s conclusion:

Without Trump in office, and without the fear that tight money will erode vote margins in the short run, Republicans are about to unite overwhelmingly behind the talking point that monetary policy needs to be substantially tightened immediately. Powell, being a Republican worthy, will listen and toe this line.

Appendix

For a deeper understanding of the “major mistake” period, the musings from the following FOMC Meetings are instructional. It is a good example of “bad monetary policy”, having nothing to do with the Chair being Republican or Democrat.

In the August 5 2008 FOMC meeting, Mishkin´s last, the inflation worry was alive and well, maybe more so than ever!

There were two options on the table regarding policy. In the first (Alternative B), the Committee would maintain its current policy stance but would underscore its concern about inflation. In the second (Alternative C) the Committee would firm policy by 25 bp.

Janet Yellen was the only participant that wanted to downplay risks to inflation. Most thought that monetary policy was accommodative.

Charles Evans (of Evans-rule fame) would feel comfortable with Alternative C and thought an increase of 50 to 75 basis points in a reasonably short period of time would be needed!

Richard Fisher and Thomas Hoenig favored C (but only Fisher dissented).

James Bullard wanted to “prepare markets for a rate increase in September”. Charles Plosser shared his feelings.

Mishkin and Rosengren leaned towards Yellen´s language.

The charts show the information – on inflation, inflation expectations and oil prices– available to the FOMC at the time of the meeting.

Oil prices had peaked a few weeks earlier and then dropped significantly. Inflation expectations both at the shorter and longer horizon had also fallen.

In particular, the close correlation between shorter (5yrs) inflation expectations and oil prices had “broken” two weeks earlier, pointing to other influencing factors in addition to the fall in oil prices. Maybe that´s associated with the perception that the Fed was on the brink of tightening (remember that the June Meeting Minutes said that “the next interest rate move will likely be up”).

Two speeches by voting Regional Fed presidents certainly helped perceptions along:

Plosner (July 22): Keeping policy too accommodative for too long worsens our inflation problem. Inflation is already too high and inconsistent with our goal of — and responsibility to ensure — price stability.We will need to reverse course — the exact timing depends on how the economy evolves, but I anticipate the reversal will need to be started sooner rather than later. And I believe it will likely need to begin before either the labor market or the financial markets have completely turned around.

Hoenig (July 16): “While the comparison to the ´70s can be useful(!), the present economic situation is also different…

However, like the 1970s, monetary policy is currently accommodative(!)…In this environment there is a significant risk that inflation and inflation expectations could move higher in coming months.

Thus, it will be important for the Federal Reserve to monitor inflation developments and inflation expectations closely, and to move to a less accommodative stance in a timely fashion”.

I think the high point of the August 5 meeting was Mishkin´s “farewell speech”:

What I’d like to spend some time on—because I feel this is sort of my swan song, but maybe because I’m a classy guy, I’ll call this my “valedictory remarks”—are three concerns that I have for this Committee going forward. I’m not going to be able to participate, but I have a chance now to lay them out.

The first is the real danger of focusing too much on the federal funds rate as reflecting the stance of monetary policy. This is very dangerous. I want to talk about that…

I´ll transcribe from the first concern:

First of all, let me talk about the issue of focusing too much on the federal funds rate as indicating the stance of monetary policy. This is something that’s very dear to my heart. I have a chapter in my textbook that deals with this whole issue and talks about the very deep mistakes that have been made in monetary policy because of exactly that focus on the short-term interest rate as indicating the stance of monetary policy. In particular, when you think about the stance of monetary policy, you should look at all asset prices, which means look at all interest rates.

All asset prices have a very important effect on aggregate demand. Also you should look at credit market conditions because some things are actually not reflected in market prices but are still very important. If you don’t do that, you can make horrendous mistakes. The Great Depression is a classic example of when they made two mistakes in looking at the policy interest rate. One is that they didn’t understand the difference between real and nominal interest rates. That mistake I’m not worried about here. People fully understand that. But it is an example when nominal rates went down, but only on default-free Treasury securities; in fact, they skyrocketed on other ones.

The stance of monetary policy was incredibly tight during the Great Depression, and we had a disaster.

The Japanese made the same mistake, and I just very much hope that this Committee does not make this mistake because I have to tell you that the situation is scary to me. I’m holding two houses right now. I’m very nervous. [Laughter].

Bernanke said on the September 16 FOMC meeting (just 24 hours after Lehman) and apparently oblivious to Mishkin´s warnings from the previous month:

As I said, I think our aggressive(!) approach earlier in the year is looking pretty good(!), particularly as inflation pressures have seemed to moderate.

Overall I believe that our current funds rate setting is appropriate, and I don’t really see any reason to change.

On the one hand, I think it would be inappropriate to increase rates at this point. It is simply premature. We don’t have enough information. There is not enough pressure on inflation at this juncture to do that.

On the other hand, cutting rates would be a very big step that would send a very strong signal about our views on the economy and about our intentions going forward, and I think we should view that step as a very discrete thing rather than as a 25 basis point kind of thing. We should be very certain about that change before we undertake it because I would be concerned, for example, about the implications for the dollar, commodity prices, and the like. So it is a step we should take only if we are very confident that that is the direction in which we want to go.

And this is the information on inflation expectations and oil prices that the FOMC had at the time of the meeting!

Note that not even oil prices resisted the (now ‘certain’) expected steep fall in aggregate demand! Not surprisingly, it materialized!

For the rest of the year, in regular and unscheduled FOMC meetings, what we perceive from the transcripts is a frantic and disorganized search for the “horses that bolted”.

As usual, the Fed never wants to accept responsibility for its actions!

There´s one passage in the October 08 meeting that is reminiscent of a November 1937 FOMC meeting.

An interesting story of the time is told by Anasthasios Orphanides. In March 1937, just before the final leg of the increase in required reserves was implemented, Marriner Eccles, the Fed Chairman said:

Recovery is now under way, but if it were permitted to become a runaway boom it would be followed by another disastrous crash.

Several months later, halfway through the recession, at the November 1937 meeting John Williams, a Harvard professor, member of the Fed board and its chief-economist said:

We all know how it developed. There was a feeling last spring that things were going pretty fast … we had about six months of incipient boom conditions with rapid rise of prices, price and wage spirals and forward buying and you will recall that last spring there were dangers of a run-away situation which would bring the recovery prematurely to a close.

We all felt, as a result of that, that some recession was desirable …

We have had continued ease of money all through the depression. We have never had a recovery like that. It follows from that that we can’t count upon a policy of monetary ease as a major corrective.

… In response to an inquiry by Mr. Davis as to how the increase in reserve requirements has been in the picture, Mr. Williams stated that it was not the cause but rather the occasion for the change. … It is a coincidence in time. … If action is taken now it will be rationalized that, in the event of recovery, the action was what was needed and the System was the cause of the downturn.

It makes a bad record and confused thinking. I am convinced that the thing is primarily non-monetary and I would like to see it through on that ground.

And Tim Geithner in 2008:

The argument that makes me most uncomfortable here around the table today is the suggestion several of you have made—I’m not sure you meant it this way—which is that the actions by this Committee contributed to the erosion of confidence—a deeply unfair suggestion.

… But please be very careful, certainly outside this room, about adding to the perception that the actions by this body were a substantial contributor to the erosion in confidence.