Is inflation stubborn?

Is inflation stubborn?

Only if you include badly conceived "guesstimates" into the fray

The NYT has a piece authored by two of its best known economic writers;

Stubborn Inflation Could Prod Fed to Keep Rates High for Longer

Toward the end, we get a clue to the title:

Many economists think that inflation is still likely to slow further, in part because cooler new rent prices are still slowly feeding into official inflation data.

The Fed has “adopted” the “stubborn view”:

Michelle Bowman, a Fed governor, has already said that while it was not her “base line outlook,” she saw “the risk that at a future meeting we may need to increase the policy rate further.”

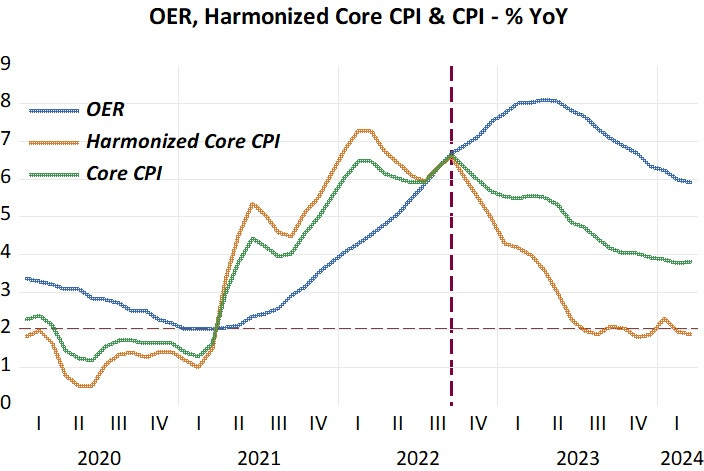

I put up two charts that very clearly reflect what´s going on with inflation. The first chart shows the harmonized index of consumer prices. It differs from the “traditional” CPI essentially due to the fact it excludes Owner Equivalent Rent (OER), which weighs 34% in the CPI.

Note that when OER takes off after September 2022, the difference between CPI inflation and the harmonized version increases. Since mid-2023, the Core CPI has flutuated narrowly around 2%, the Fed´s target for inflation. Given the still high (even if falling) increase in OER, the difference between the CPI and the Harmonized version remains high.

It is clear that the “stubbornness” of inflation is all due to OER (a “made-up” component).

The next chart illustrates the story for the PCE. In the PCE, OER has a much lower weight (13%), which explains why PCE inflation is significantly lower than CPI inflation. If OER inflation continues to fall (very likely), PCE inflation will soon hit the 2% target. (Unfortunately, there is no harmonized version of the PCE)

I have a hard time trying to understand why the Fed (and many analysts) are so “worked-up” about the “stubbornness” of inflation. And we should never forget that Fed errors can have major consequences (just look at 2008).

All those points are mentioned (I wish there was harmonized version of the PCE). From "first principles" the Fed should not target any inflation measure! Target NGDP-LT

Y-o-y doesn't cut it.