Inflation mongering is back

Is this time really different?

Just two examples out of hundreds possible. One from now: “Yes, This Time We’ll Have Inflation, and Here’s Why”

After several decades of relatively low rates of inflation, it is easy to think that we will continue to see little change in prices. But the seeds of inflation have been planted.

and one from 10 years ago: “The Great Inflation of the 2010s”

“I can't eat an iPad." This could go down in history as the line that launched the great inflation of the 2010s.

My purpose here is to tell a story showing what drives inflation and then, with that story in hand, identify the factors that could foster inflation going forward.

The story will be told guided by the overriding principle that inflation is a monetary phenomenon. That principle is encapsulated in the equation of exchange which, in growth form, can be written as:

M+V=P+Y

where, M is the growth of the money supply, V the growth rate of the velocity of circulation (the inverse of growth in money demand), P inflation (here represented by the Core PCE) and Y the growth of real output.

Following Milton Friedman´s analysis in “A monetary theory of nominal income”, I “bundle” P+Y as Nominal Gross Domestic Product or, simply, NGDP, from the assumption that the division between prices (P) and quantities (Y) is determined by variables not explicitly contained in the theory.

With that the equation of exchange in growth form is written as:

M+V=NGDP

By “ignoring” the division between prices (P) and quantities (Y), we are only concerned with aggregate nominal spending (or NGDP) growth. In this way, an “appropriate monetary policy” is one that maintains nominal stability (or a stable growth of nominal spending).

In other words, an “appropriate monetary policy” is one in which money supply growth “adequately” offsets changes in velocity to keep NGDP growth stable. (Note: The level path along which the stable growth takes place is very important, and I´ll have something to say about that later).

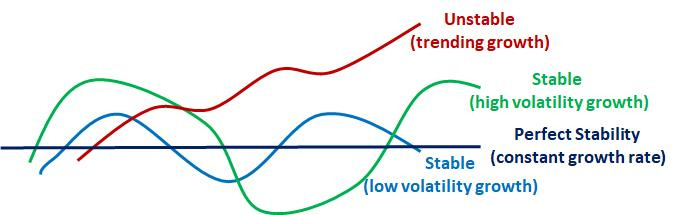

“Stable” is not a precise concept. The figure below illustrates. Perfect stability means that the growth rate of NGDP is constant. But stability can also have different degrees of volatility (or how much it varies around the constant average). If growth is unstable, it means it is trending, in which case the mean growth is not “identifiable”.

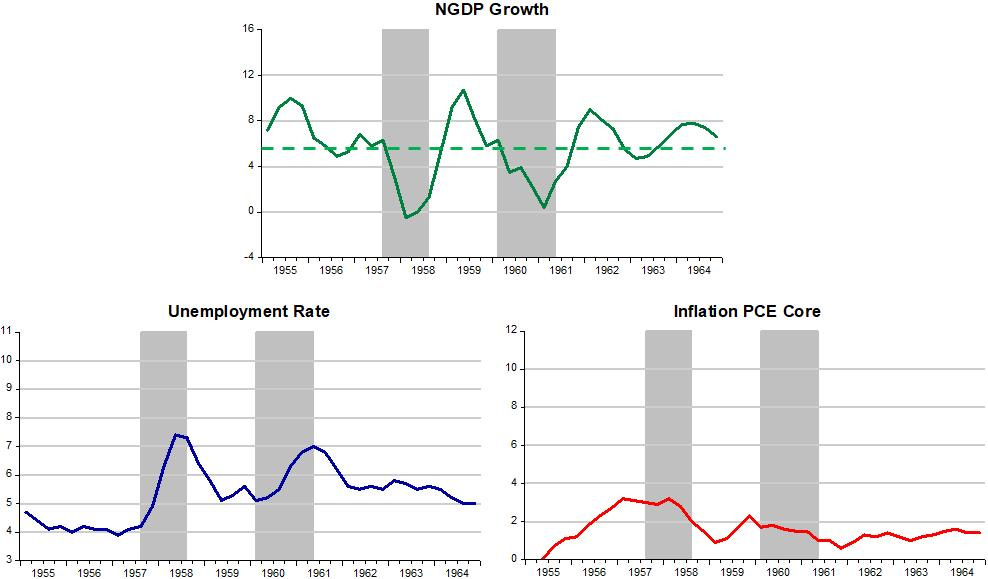

To check the “appropriateness” of monetary policy and how unemployment and inflation were affected, I examine several periods over the last 66 years, beginning in 1954. (Note: In all the examples, each variable has the same scale). The first period analyzed covers 1954 to 1964.

NGDP growth was stable, becoming more so towards the end of the sample. Regarding unemployment, it rises when NGDP growth falls significantly below average and remains on a downward trend when NGDP growth remains closer to trend.

Inflation initially rises reflecting initially higher NGDP growth, but as NGDP growth becomes more stable, inflation also remains low and stable.

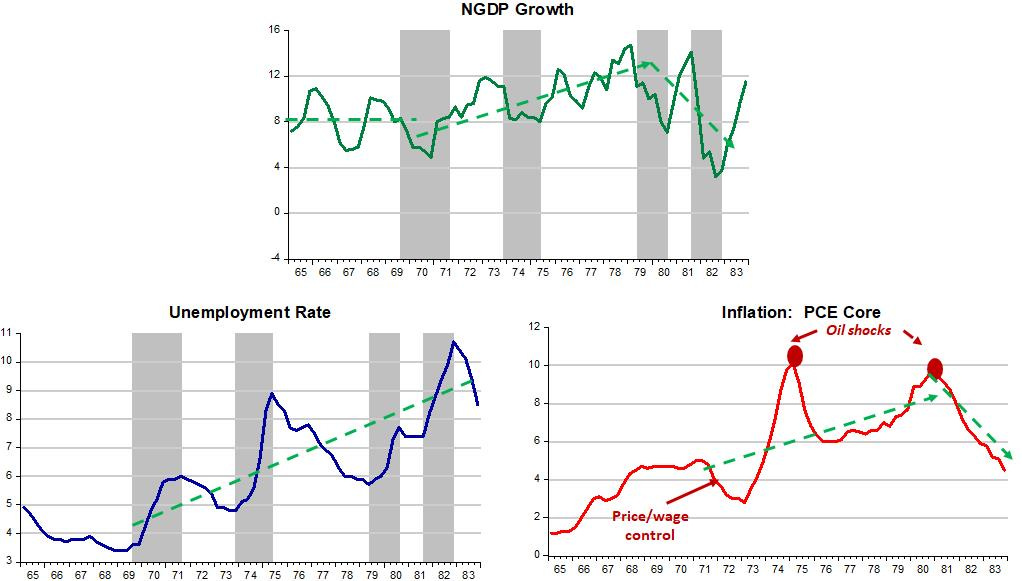

The second period goes from 1965 to 1983. It is a complicated period covering the Great Inflation episode.

Is there a plausible story behind the patterns observed?

Arthur Okun (of “potential” RGDP fame) then member of the Council of Economic Advisers later wrote:

“In 1965 the nation was entering essentially uncharted territory. The economists in government were ready to meet the welcome problems of prosperity. But they recognized that they could not provide a good encore to their success in achieving high-level employment”.

They certainly tried. Observe that from 1965, the stable rate of NGDP growth increased from a bit below 6% to 8%. With that, the unemployment rate continued to fall but inflation expectations (and inflation) rose to a higher but still stable level of close to 5%.

In late 1969, the economy had entered a recession, the first in 10 years. The recession reflected the pull back in NGDP growth. The rise in unemployment was the first victim.

In 1970, Arthur Burns took over as Fed Chair. He did not think inflation was a monetary phenomenon, reflecting, instead, the power of labor unions, oligopolies and, later, oil producers. On the other hand, President Nixon, concerned with his reelection prospects in 1972, felt the increase in unemployment and higher inflation was not a good combination for his chances.

Arthur Burns came to the rescue, with wage and price controls to contain inflation and the introduction of an expansionary monetary policy to decrease unemployment. Initially he was successful. Inflation dropped and unemployment fell, and Nixon was reelected!

Burn´s view that monetary policy was “powerless” to control inflation imparted an upward bias to NGDP growth that came to be known as Go-Stop monetary policy, with the Go phase stronger than the Stop phase.

The Go-Stop “strategy” for monetary policy imparted an upward bias also to inflation and unemployment that would have been present even without the spikes to those variables from the oil shocks.

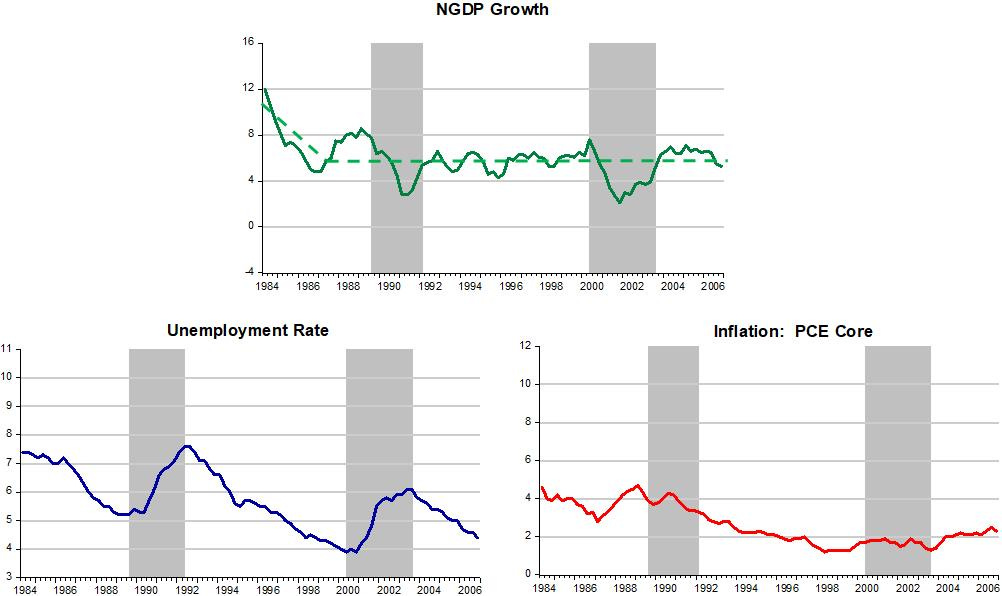

A noticeable change began in mid-79 when Paul Volcker took over at the Fed. Contrary to Burns, Volcker believed inflation was a monetary phenomenon. This fundamentally changed the nature of monetary policy as evidenced in the next period that covers the years from 1984 to 2006, which came to be known as “Great Moderation”.

When Volcker passed on the baton to Greenspan in mid-87, inflation and unemployment were down to levels seen early in the previous decade and NGP growth was just about to embrace” its new stable growth rate (around 5.5%).

Note again the sensitivity of unemployment to drops in NGDP growth below the stable rate and how unemployment falls continuously with NGDP growth remaining close to that rate.

With the adjustments to monetary policy during the Volcker years, which essentially gave up on the Go-Stop “strategy, Fed credibility for maintaining low inflation was attained. Greenspan´s major error occurred in the early 2000s when he allowed monetary policy to bring NGDP growth significantly below the stable growth rate.

At the time, with unemployment falling to rates last seen in the late 1960s, and many at the FOMC still adept to Phillips Curve thinking (that “too low” unemployment would eventually spark inflation), the Fed tightened monetary policy by significantly reducing the rate of NGDP growth.

Just before passing the Fed leadership to Bernanke in January 2006, Greenspan had placed the economy back on track, with the unemployment rate again falling to low levels and inflation low & stable (despite the oil price increases that began in late 2003).

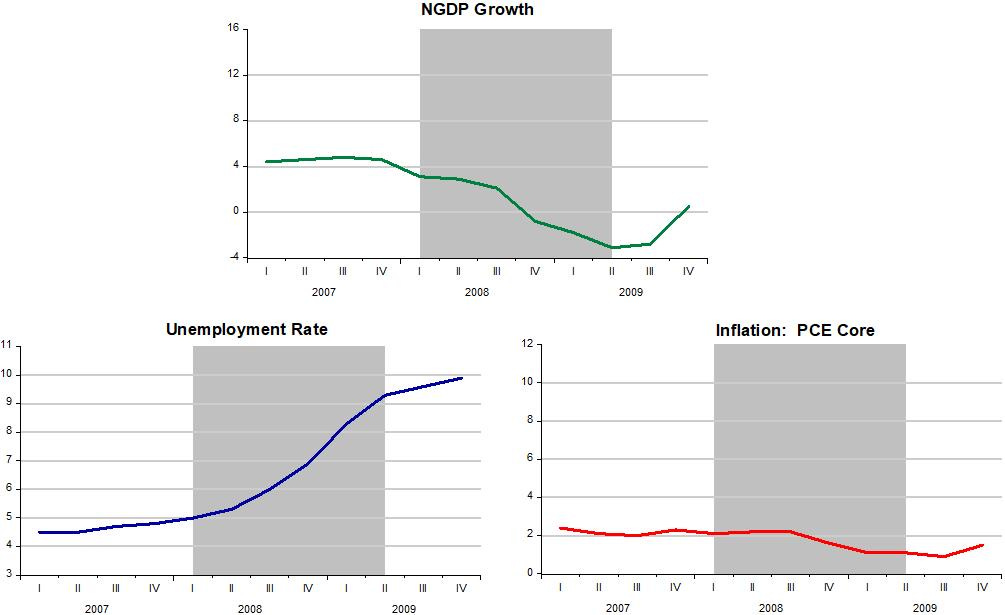

As the pictures relating to 2007 - 09, also known as the “Great Recession” show, the hard won nominal stability of the Volcker Greenspan years was lost in the blink of an eye.

The degree of monetary mismanagement behind this outcome is baffling! And worse, this gross mismanaging of monetary policy is still not adequately recognized.

This old post provides ample evidence that the mistakes came from the Fed´s laser-focus on headline inflation. And Bernanke´s “Credit View” of monetary policy only made things worse as Tim Congdon argues in the closing paragraphs of chapter 18 - “The Role of Creditism in the Great Recession of his book “Money in a Free Society”:

To summarize, the monetary (or monetarist) view of banking policy is in sharp contrast to the credit (or Creditist, to recall Bernanke´s term) view. Contrary to the plethora of misguided academic papers, the monetary view contained – and of course still contains – a clear account of how money affects spending and jobs…

The debate about quantitative easing, and the larger debate between creditism and monetarism to which it is related, will rage for years to come. Much will depend on events and personalities, as well as on ideas and journal articles. But there is at least an argument that Bernanke´s creditism was the mistaken theory which, by a remorseless logic of citation, repetition and emulation, spread around the world´s universities, think tanks, finance ministries and central banks and led to the Bedlam of late 2008…

The academic prestige attached to the lending-determines-spending doctrine and other credit-based macroeconomic theories is puzzling. [As noted earlier], Bernanke and Gertler include in their 1995 article the observation that comparison of actual credit magnitudes with macroeconomic variables was not a valid test of their theory. One has to wonder why.

They claimed that bank lending was determined within the economy and so was “not a primitive force”…Bernanke and Gertler must have known that the relationship between credit flows and other macroeconomic variables were weak or non-existent, casting doubt on their whole approach.

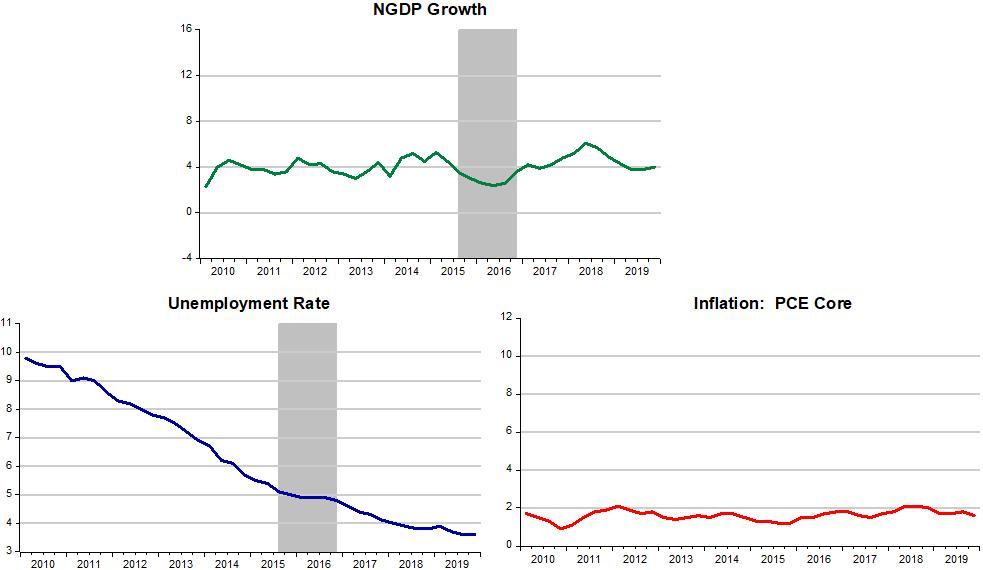

How did Bernanke and the Fed get out from “underneath the bus”? As the pictures for the 2010s show, they did so by reinstating Nominal Stability!

Note once again the sensitivity of the unemployment rate to drops in NGDP growth. When NGDP growth drops below the stable growth rate, the fall in unemployment takes a break.

At that time, the Fed was led by Janet Yellen, an “avid adept” of Phillips Curve thinking, so with unemployment falling to 5%, a level thought to be very close to the “natural” rate, all the talk was about the “lift off” of interest rates.

What´s the takeaway so far?

The economy does significantly better when the Fed manages to keep NGDP growing at a stable rate. Inflation remains low & stable and unemployment falls.

The fact that the unemployment rate falls from previous higher levels during the periods when NGDP growth is very stable, while inflation remains low, was never well understood by the Fed, where the belief in the existence of a Phillips Curve is ingrained. So, whenever unemployment fell to rates that were viewed as being close to the NAIRU, or natural rate, the Fed tightened policy.

The “solution” to the “mystery” was spelled-out more than 20 years ago by William Poole, at the time President of the St Louis Fed, in the June 2000 FOMC Meeting:

The traditional NAIRU formulation views the wage/price process as running off a gap–a gap measured somehow as the GDP gap or the labor market gap. And the direction of causation goes pretty much from something that happens to change the gap that feeds through to alter the course of wage and price changes.

I think there is an alternative model that views this process from an angle that is 180 degrees around. It says that in an earlier conception, either through a determination of a monetary aggregate or through a federal funds rate policy, monetary policy pins down the price level or the rate of inflation and, therefore, expectations of the rate of inflation. Then the labor market settles, as it must, at some equilibrium rate of unemployment. Where the labor market settles is what Milton Friedman called the natural rate of unemployment.

But the causation goes fundamentally from monetary policy to price determination and then back to the labor market rather than from the labor market forward into the price determination. I certainly view the causation in that second sense.

I think it is the willingness of the Federal Reserve to stamp out signs of rising inflation that ultimately pins down expectations of the price level and the inflation rate. Now, the labor market has been clearing at a level that all of us have found surprising. But I don’t think that necessarily has any particular implication for the rate of inflation, provided we make sure that we are willing to act when necessary. (pg 61).

There is, however, something missing. While the 20 plus years of the Great Moderation and the 2010s were periods of high NGDP growth stability, falling unemployment (except when the Fed got “scared” of the low unemployment rate and tightened policy) and low and stable inflation, they are different in one important dimension.

While the post 1984 years were called “Great Moderation”, the 2010s got called, alternatively, Secular Stagnation, Lesser Depression, Long Depression, among other unflattering monikers!

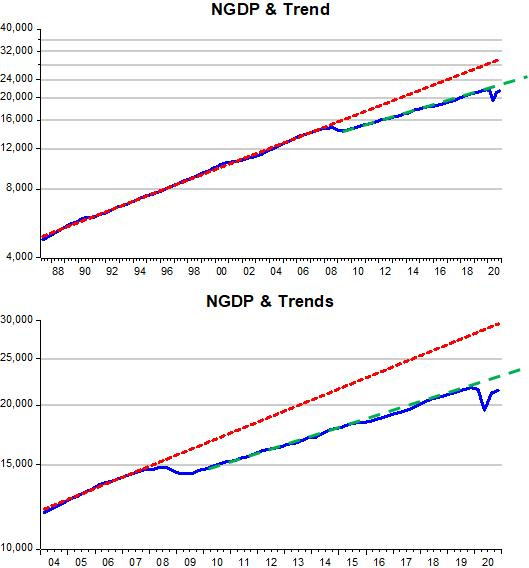

As the charts below clearly show (the second chart is just a zoom-in of the first), the LEVEL path of aggregate nominal spending (NGDP) was significantly lower in the 2010s.

That happened because the Fed never pursued a recovery, as it did after other recessions (even from the Great Depression), but was “content” to provide nominal stability starting from the lower LEVEL the economy reached during the Great Recession.

It appears the Fed has belatedly recognized the importance of the LEVEL of economic activity. In a recent speech, Fed Governor Lael Brainard says:

For nearly four decades, monetary policy was guided by a strong presumption that accommodation should be reduced preemptively when the unemployment rate nears its normal rate in anticipation that high inflation would otherwise soon follow.

But changes in economic relationships over the past decade have led trend inflation to run persistently somewhat below target and inflation to be relatively insensitive to resource utilization.

With these changes, our new monetary policy framework recognizes that removing accommodation preemptively as headline unemployment reaches low levels in anticipation of inflationary pressures that may not materialize may result in an unwarranted loss of opportunity for many Americans. It may curtail progress for racial and ethnic groups that have faced systemic challenges in the labor force, which is particularly salient in light of recent research indicating that additional labor market tightening is especially beneficial for these groups when it occurs in already tight labor markets, compared with earlier in the labor market cycle.

Instead, the shortfalls approach means that the labor market will be able to continue to improve absent high inflationary pressures or an unmooring of inflation expectations to the upside.

So, what conclusions can we draw from this high-level overview of a variety of labor market indicators, their current readings, and their performance in the previous expansion?

First, the headline unemployment rate by itself can obscure important dimensions of labor market slack, so it is important to heed Dr. Palmer's dictum and consult a broad set of aggregated and disaggregated measures.

Second, groups that have faced the greatest challenges often make important labor market gains late in an expansion, consistent with Augustus Hawkins's emphasis on the importance of full employment for all Americans.

Brainard´s speech reminds me of a talk given by Gardner Ackley, then President of the Council of Economic Advisers, in 1965:

“…The plain fact is that economists simply don´t know as much as we would like to know about the terms of trade between price increases and employment gains (i.e, the shape and stability of the Phillips Curve).

We would all like the economy to tread the narrow path of balanced, parallel growth of demand and capacity utilization as is consistent with reasonable price stability, and without creating imbalances that could make continuing advance unsustainable.

But the macroeconomics of a high employment economy is insufficiently known to allow us to map that path with a high degree of reliability…It is easy to prescribe expansionary policies in a period of slack. Managing high-level prosperity is a vastly more difficult business and requires vastly superior knowledge.

The prestige that our profession has built up in the Government and around the country in recent years could suffer if economists give incorrect policy advice based on inadequate knowledge. We need to improve that knowledge”.

I think the Fed´s focus on the labor market to “establish” the appropriate LEVEL of nominal spending is a risky proposition, just as it proved to be a risky proposition in the 1960s, which ended up stocking the rise in inflation that marked the 1970s. As I´ll argue later, the Fed will have a better chance of achieving a “noninflationary success” if it focuses on defining an “appropriate” LEVEL of NGDP and a well announced plan to get there.

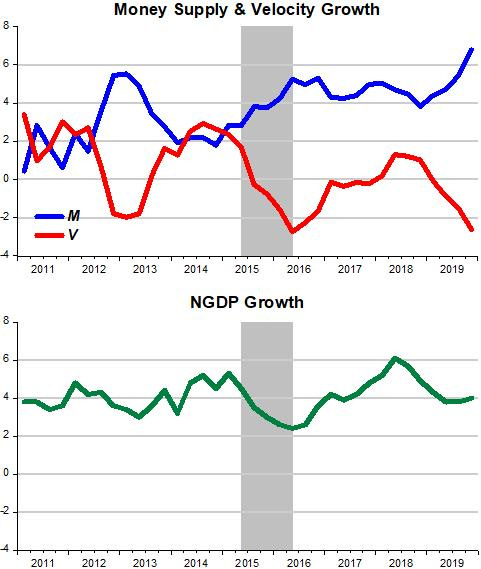

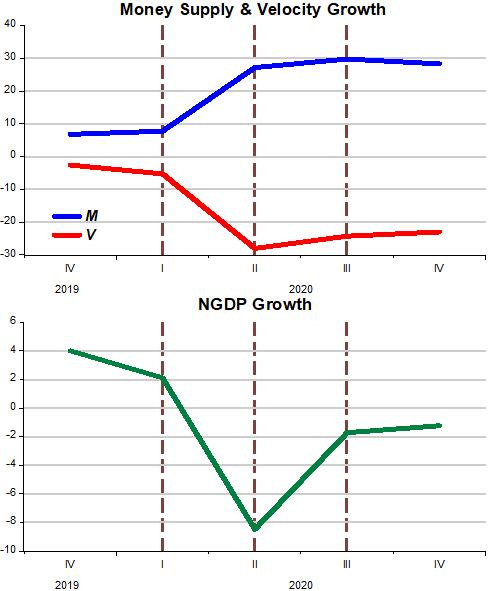

To better understand what happened in 2020, with the advent of Covid19, the next chart shows how monetary policy pinned down the stable growth rate of NGDP during the 2010s.

Where it is observed that over the decade, money supply growth closely offset changes in the growth of money demand (the inverse of Velocity).

In 2011, to counter the inflation mongers of the day, Kurt Schuler put it clearly:

To talk intelligently about the money supply, you must also consider the demand for money [1/velocity]. Starting from a situation where supply and demand are in balance, the supply can triple, but if demand quadruples, money is tight. Similarly, the supply can fall in half, but if demand is only one-quarter its previous level, money is loose.

The charts for 2020 below clearly show that commenters like Steve Hanke miss the point:

Since February 2020, the quantity of money in the U.S. economy, measured by M2, has increased by an astonishing $4 trillion. That's a one-year increase of 26%--the largest annual percentage increase since 1943.

Where we observe that despite all the money supply growth, NGDP growth is still negative and far below the 4% rate of growth that defined the stable NGDP growth of the 2010s, meaning that the level of spending is still far below the level that prevailed in the 2010s.

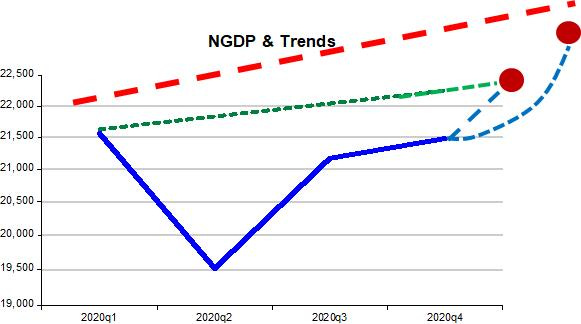

The LEVELS chart below may serve as a “decision map” for the Fed. The red dotted line represents the LEVEL trend path of the Great Moderation, while the green dotted line the LEVEL trend path that defined the 2010s. The blue line is actual NGDP.

Will the Fed be content in bringing NGDP back to the more recent trend level path, or will it strive to get somewhere nearer to the GM trend level path? (And practice Nominal Stability at a specified stable growth rate from then on).

I believe that´s a much better way to frame the problem, with monetary policy focusing on offsetting changes in velocity (which will likely be rising with the waning of the pandemic) in such a way as to guide NGDP to its “desired” destination.

That strategy (as opposed to “looking at the labor market”) will help keep any rise in inflation a temporary phenomenon and keep inflation expectations anchored.

You say:

"M+V=P+Y

where, M is the growth of the money supply, V the growth rate of the velocity of circulation (the inverse of growth in money demand), P inflation (here represented by the Core PCE) and Y the growth of real output."

"the growth rate of velocity of circulation..."

That's all a bit thick to decipher; could you provide the Units for each of the variables?

Presumably the combination of Dollars, Time, or whatever.

(in physics, we always have the units available to ensure we are adding like quanities, and see what is the sense of the various divisions/ratios)

Thanks!