In the 90s, the US economy weathered shocks well

In the 90s, the US economy weathered shocks well

and there were some significant ones. In addition, it showed "compassion"

Jason Furman blames the Fed´s interest rate policy:

In 1998 the Fed did cut rates by 75bp rate in response to financial turmoil. This fueled the bubble and contributed to the 2001 recession. The Fed should be mindful about the banking situation but not overly mindful in a panicky way when it is still far from its macro mandate.

The 1990s was such a “rich” period for evidence that a good monetary policy - one that strives to maintain Nominal Stability - is capable of “defending” the economy from both “foreign & domestic enemies”. As I´ll show, the evidence for that becomes clear exactly when monetary policy “loses its way”!

In 1992 there was the ERM crisis (Europe´s exchange rate mechanism) culminating in the large devaluation of the British Pound. The big winner here was George Soros, who netted 1 billion pounds from his short position. It was mostly a European affair. Then there was the Mexican crisis that erupted in 1994. I won´t bother with that one because the “enemy was weak”.

In 1997 there was a sequence of Asian countries crises, beginning with Thailand in June and quickly followed by Malaysia, Indonesia, Philippines and then, in October, the “big one” in South Korea. Some months later, in 1998, there was the Russia crisis, followed by the demise of the hedge fund LTCM (Long Term Capital Management).

The story of LTCM is one of the great financial stories populated, as it was, mostly by finance geniuses (including Nobel winners Robert Merton & Myron Sholes). You can read a little about it in “The Failure of LTCM and the Russian Crisis”.

Let me not get ahead of myself and start with the Asia crisis. From the Asian perspective the crisis was a classic balance of payments (BP) crisis. The role of the US was to facilitate the adjustments required. To make things clear imagine a 2-country world. One large, the other small. Call them US and Korea.

When the crisis hit, the Korean currency (won) had to depreciate. That, however, was not enough. It also had to reduce absorption. For the Korean economy to adjust, it had to transfer resources from the production of non tradeable goods to the production of tradeable goods. In other words it had to decrease the current account deficit/increase the surplus.

The other economy, the large US economy, had to do the opposite; transfer resources from the production of tradeable goods to the production of non tradeable goods (say, housing). The current account deficit of the US would have to increase. The appreciation of the dollar would reduce the relative prices of tradeable goods and direct spending towards tradeable goods and away from non tradeable goods. In that case, prices of non tradeable goods would decline, over time negating the relative price change induced by the appreciation of the dollar and thus reduce spending on tradeable goods, impairing the adjustment required to “solve” the Korean crisis.

For that not to happen, monetary policy in the US has to strive to maintain Nominal Stability. With that, aggregate nominal spending growth will remain stable. Given the fall in the relative price of tradeable goods, spending on non tradeable goods would increase, likely increasing their prices.

[Note that the US in this example is the “passive” agent. It just has to be “compassionate” and provide the conditions to provide support to the “suffering” economy that, otherwise, would have to endure much greater pain. The more recent example of the Greek Spanish & Italian economies illustrate how Germany showed no “compassion”, leaving those countries to bear the brunt of the adjustment without providing any help. For an illustration, see here]

These things happened. Focusing mostly on the US, we observe, after the strong depreciation of the won, that:

Resources were transferred from the tradeable to the no tradeable (housing) sector. House starts increased.

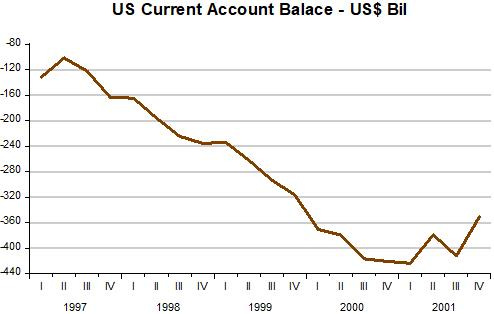

The current account deficit increased substantially. (In Korea, meanwhile, the current account went from a deficit of 4% of GDP in 1996 to a surplus of 10.5% of GDP in 1998).

House price in the US started off a rising trend. (In Korea, they fell).

These adjustments were made possible, and ran “smoothly”, due to the US maintaining Nominal Stability, with aggregate nominal spending (NGDP) hugging a stable level path.

This helped Korea show a quick recovery. While in mid-98 RGDP growth in Korea hit -7.3% (yoy), by the end of 1999 it grew 13.7% (yoy). From then until the GFC growth averaged a healthy 5.5%.

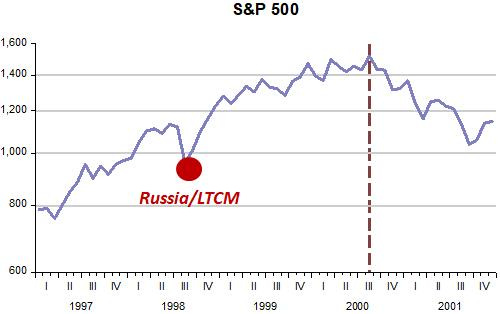

Following closely on the heals of the Asia Crisis, the economy was hit by the Russia Crisis and LTCM. If you had no idea those shocks took place, you wouldn´t believe they did from looking at the economy. Actually there was one clue, the stock market.

Maybe looking at this performance and to house prices, Jason Furman comes to the conclusion that the Fed, by cutting 50 bp, “fueled the bubble and contributed to the 2001 recession.”

There´s no “bubble” in house prices. It´s an example of the price system at work to allow the “optimal adjustments” (which work much better in an environment of Nominal Stability). The same for the stock market, which had been on an upward trend since the Volcker adjustment in the early 1980s allowed people to “imagine” a nominally stable economy going forward!

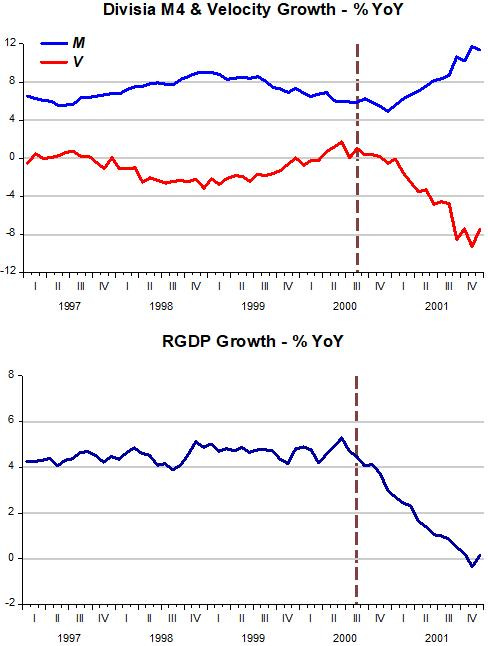

The panel below is very clear on the importance of Nominal Stability (NS). With NS, required adjustments are much easier and proceed rather smoothly. We easily pinpoint the moment nominal stability was lost (due to “inadequate” monetary policy.)

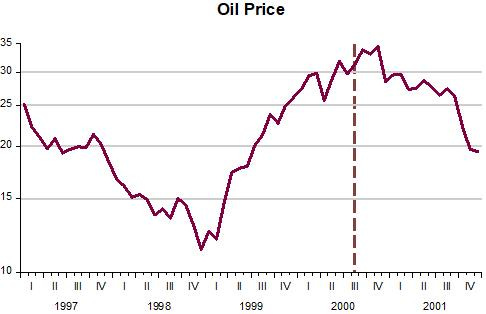

If you read the 2000 Fed Transcripts, you notice two major worries from several FOMC members. The “too low” rate of unemployment and the rise in oil prices that followed the “resolution” of the Asia and Russia crises.

Very likely, “Fed talk” led to increased risk perceptions and a fall in velocity (rise in money demand). The chart below shows that after mid-2000, money supply did not adequately offset the change in velocity, resulting in a significant drop in NGDP growth, which led to an increase in unemployment and a drop in RGDP growth, i.e. Recession!

The Fed corrected this mistake in 2003, so that by the time Greenspan left the Fed (Jan 06), nominal stability had been recouped. Soon, however, Bernanke would “mess-up” again and reap the GFC (a.k.a. Great Recession), another instance of failed monetary policy!

Greenspan never tightened and Bernanke never eased.

re: "money supply did not adequately offset the change in velocity"

Velocity fell because there was an increased volume of saved deposits in the banking system.