How do things look in Japan?

How do things look in Japan?

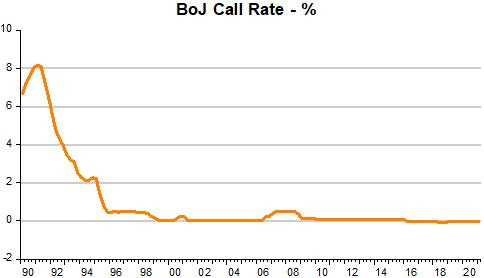

And it is said the BoJ has not tightened for 30 years!

Mervyn King wrote a letter to the Financial Times. This caught my eye:

First, the large monetary and fiscal stimulus injected in the advanced economies is out of all proportion to the magnitude of any plausible gap between aggregate demand and potential supply.

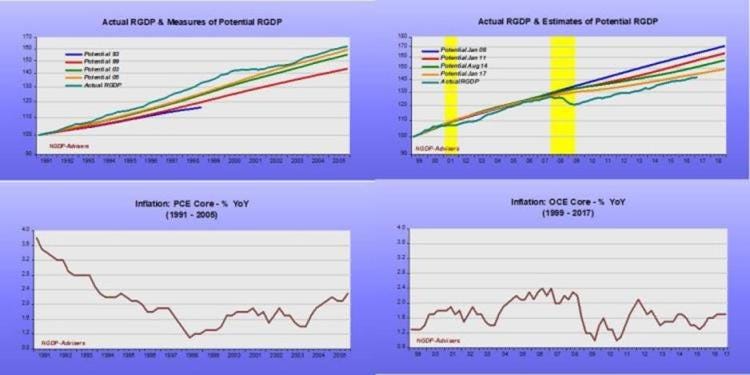

Gap theories have done so much harm! That´s because, no matter where actual output is, the belief is that “potential” output is always inching close to it. These charts from sometime before the pandemic illustrate my point. I call them ‘The hare (“potential” output) is always chasing the fox” (“actual” output).

On the LHS charts you see that even with actual output far above “potential”, inflation remains on a downtrend. On the RHS charts, inflation remains low and stable even when actual output is far below “potential”!

This is also true for other “gaps”. One is the NAIRU (or “natural” rate of unemployment). To show how misleading that has proved to be, more than a quarter century ago, in the FOMC meeting of December 1995, Greenspan noted wryly:

“Saying that the NAIRU has fallen, which is what we tend to do, is not very helpful. That’s because whenever we miss the inflation forecast, we say the NAIRU fell” (p. 39).

Seven months later, in the July 1996 meeting Thomas Melzer, president of the St Louis Fed commented:

“Whenever we get to whatever the NAIRU is, people decide it is not really there and it gets revised lower. We get to what people thought would be the NAIRU, we do not see wage pressures, and we assume that the NAIRU must be lower. So it keeps getting revised down.” (p. 61)

A few years later, in the June 99 FOMC meeting, William Poole, president of the St Louis Fed observed:

I certainly count myself among those who believe that the Phillips curve is an unreliable policy guide. What that means is that the predictive content for the inflation rate – and I’ll emphasize the “predictive” – of the estimated employment gap or GDP gap, however you want to put it, seems to be very low. (pg 106)

But it seems economists love these “imaginary numbers”, and so keep referring to them! It´s like those that still think Chloroquine is effective in treating Covid19!

What I really want is to say something about Japan. Stephen Williamson took Mervyn King´s letter to the FT and wrote a long Tweeter thread that I reproduce below:

1/ You can put Mervyn King (ex Bank of England Governor, 2003-2013) in the "inflation is likely to blow up unless central bankers come to their senses" camp. Why is he worried? (i) He thinks monetary and fiscal policy is about careful management of...

2/ "aggregate demand" relative to "potential supply." So, he seems like a conventional aggregate-demand-management Keynesian policymaker. Like Larry Summers, for example. (ii) He's bothered by high growth in broad monetary aggregates. So maybe he's a monetarist too.

3/In central banks those are hard to find these days, and most of the academic monetarists are deceased or emeritus. But if you look, you can find a few monetarists who aren't so old (https://federalreserve.gov/econres/edward-nelson.htm…). (iii) Mervyn is also worried about "unwise central bank promises not...

4/to tighten too soon. So, I think we can dismiss (i). I know some of you were told when you were undergrads that stimulative monetary and fiscal policies shift the AD curve and prices go up, but that framework is hopeless for the task at hand here. As King recognizes, the...

5/price increases we're seeing could to be temporary. That's what the central bankers are saying, so it seems perfectly reasonable to wait a few months before pulling the fire alarm. Some people have a view that if we let inflation out of the box, we'll never get it back...

6/in there, but I think that's also too alarmist. Monetarist may be dead, in the sense that no central bank wants to apply the idea that controlling monetary aggregates helps us control inflation - because it works poorly. But an important legacy of monetarism is that the...

7/central bank controls inflation. That seems natural now, but it wasn't always like that. But how do they do it? Typical procedure is to peg an overnight interest rate, day-to-day, and then change that interest rate target in response to observables, with a view to meeting...

8/the central bank's goals - typically an inflation target of 2%, but could include other things. But, to get on with it, my favorite part of the "letter" is the first sentence: "Price stability is when people stop talking about inflation." That is, the key evidence for the...

9/success of inflation targeting is that the average person spends more time watching paint dry than thinking about inflation. This survey done by the Bank of Japan is interesting (https://boj.or.jp/en/research/o_survey/ishiki2104.htm/…) So, not only are people in Japan not talking about inflation, they've...

10/mostly lost interest in the Bank of Japan, what it does, and whether they should be confident in its performance. Only 18% of people in the survey actually "know about" the BoJ's 2% inflation target. The background is that average inflation in Japan has been about zero...

11/since the mid-1990s. If you looked at the time series you might think the BoJ was shooting for 0% inflation since 1995. But, they have had a 2% inflation target since 2013, and have consistently undershot inflation since then. By their own job performance standards, they...

12/get a "D." But the Japanese public doesn't care if its central bankers think they are failing. Apparently they're fine with it. And, it seems Mervyn King would be fine with it too. The Japanese people have stopped thinking about inflation. But the BoJ has never "tightened"...

13/over that whole period since 1995. So why does King think it's so unwise for a central bank to promise not to tighten too soon?

I´ve highlighted several passages, but I want to concentrate on “But the BoJ has never tightened since 1995”.

That ties in with the view that to conduct monetary policy, the “Typical procedure is to peg an overnight interest rate”.

The last time the BoJ increased the call rate (its Fed Fund rate), was in 1990. Thereafter it reduced the call rate all the way to zero by 1995, where it has stayed since. For seven years (2008 - 2015), the Fed kept the FF rate at zero and never lost the chance to remark that monetary policy was extremely accommodative. What to say, then, of the BoJ monetary policy, which has kept rates at zero for over 25 years?

The clearly shows that interest rates DO NOT define the stance of monetary policy. Worse, if you think it does, a lot of damage can (and has) been done!

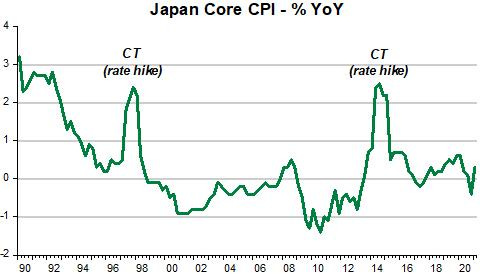

The next chart shows that CPI core inflation reached zero in 1995 and has remained there expect for periodical consumption tax rate hikes (even with those tax hikes, since 1995 inflation has averaged all of 0.03% per year).

The “funny fact” is that when rates reached zero in 1995, deflation set in! (that is Steve Williamson´s New Monetarist “prediction”, which is only valid if monetary policy (not to be confused with interest rates, allows).

And deflation only stopped when “Abenomics” was introduced when Shinzo Abe became prime minister in December 2012. “Abenomics” is based upon "three arrows": monetary easing from the Bank of Japan, fiscal stimulus through government spending, and structural reforms. While Abenomics” never came close to satisfying its objectives, it was enough to stop deflation.

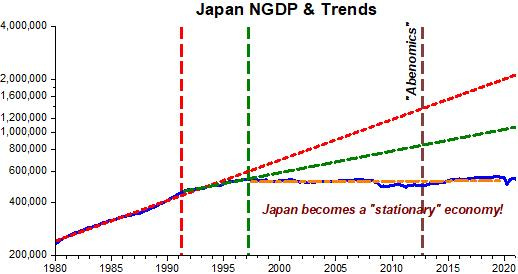

The next chart shows how monetary policy tightened in the early 1990s, remaining very tight for most of the past 30 years. It appears “Abenomics” was only successful in bringing aggregate nominal spending (NGDP) back to the (flat) trend it had deviated from during the “Great Recession”. The Japanese economy has in fact become a (nominal) “stationary” economy!

Since monetary policy is able to keep NGDP growth at any rate (stable or not) it wishes, monetary policy is responsible for the Japanese economy becoming a nominal “stationary” economy. Two examples illustrate. During the 1980s, monetary policy “dictated” NGDP growth averaging a stable 6% rate. From the late 1990s, the “chosen” rate was 0%.

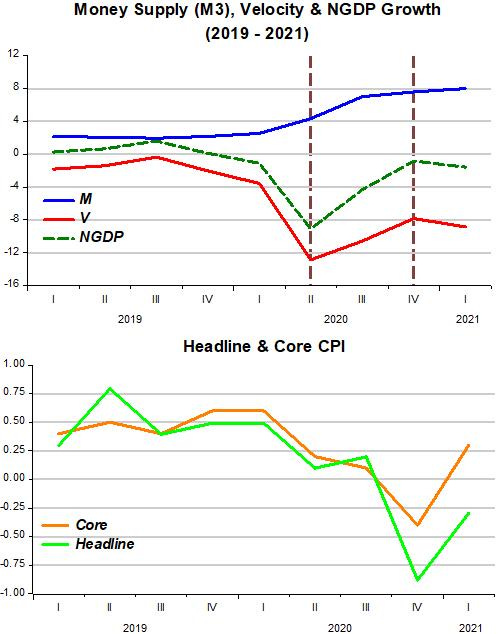

And at present, the picture is dire. In contrast with the Fed (see here), the BoJ has been “stingy” with monetary policy. So nominal spending has fallen more and reversed more slowly. Even so, inflation has increased, but remains below the pre pandemic level. Supply bottlenecks affect every country, but if monetary policy is appropriate, just like in the Japanese example of consumption tax hikes, the resulting inflation will be temporary.

A lot of economists in the late 1950's knew that banks didn't loan deposits. Today there is 15 trillion dollars impounded in the payment's system. In Japan, the Japanese save more and keep more of their savings in their payment's system. That destroys money velocity. That requires increasing infusions of Reserve Bank Credit just to maintain existing real dollar amounts of GDP.