Frozen, Not Cracking

The May jobs report beat every forecast. Read past the headline and it describes a stranger, more brittle labor market than the number suggests.

The May employment report, released June 5, did something no one expected: it came in strong, and not by a little.

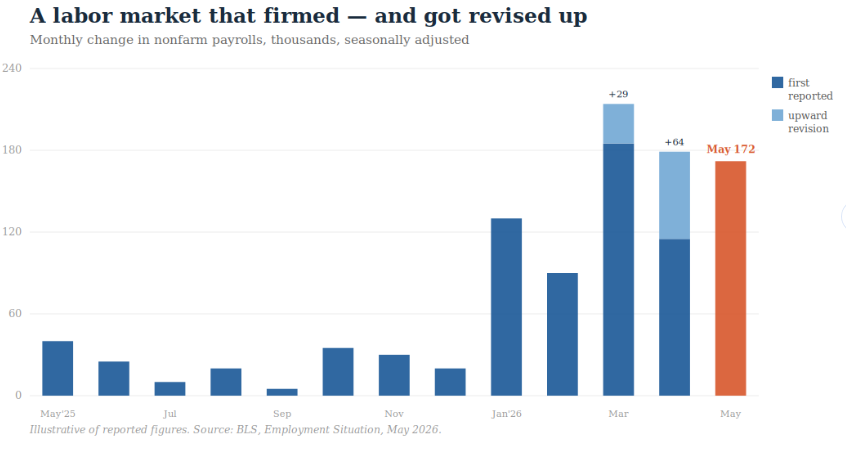

Nonfarm payrolls rose 172,000, against a consensus near 80,000. The unemployment rate held at 4.3 percent. And the months behind it were revised up — March and April together added 93,000 more jobs than first reported, making the three-month stretch the strongest in over two years.

That last detail matters more than the headline. Upward revisions are the opposite of what you see when an economy is quietly rolling over. A market sliding toward recession tends to get revised down as late survey responses trickle in. This one firmed up. So the first thing to say is that the labor market is more resilient than the gloom of recent months implied.

But a single month flatters and misleads in equal measure, and this one requires and rewards a closer look. Three things complicate the strong headline.

The first is that the gains were narrow. The hiring was concentrated in leisure and hospitality — mostly food service — local government, and health care. Manufacturing was barely positive; financial activities shed jobs. A report carried by two or three sectors is not the same as broad-based demand for labor. It is a thinner foundation than 172,000 makes it sound.

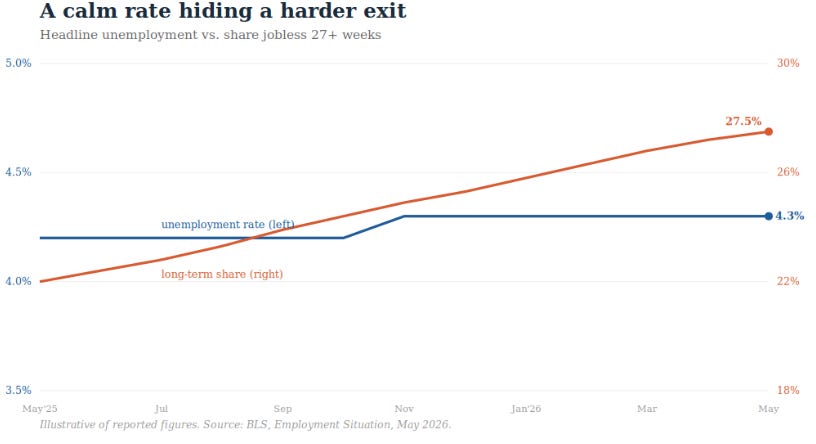

The second is more important, and it hides inside the calm 4.3 percent unemployment rate. That rate is steady not because opportunity is abundant but because firing is scarce. Almost no one is being let go — the number of people newly unemployed actually fell. But the people who are out of work are stuck there.

The share of the unemployed who have been jobless for 27 weeks or more has climbed to 27.5 percent, the highest of this cycle, up by more than half a million over the year. That is the signature of a low-hire, low-fire market: comfortable if you have a job, and very hard to climb back into if you lose one.

The third complication is a lesson in reading these reports. April’s household survey had shown a spike in fresh joblessness, and much of the coverage ran with it as evidence the market was breaking.

In May that spike reversed. The April alarm was largely noise — the dramatic single-month move that wasn’t real. The quieter signal underneath, the steady rise in long-term unemployment, is the one that is. It is a useful reminder that the loudest number in any given month is often the least reliable.

On wages, the report offers the one strand that argues for easier policy. Average hourly earnings rose 3.4 percent over the year, cooling from 3.6 percent the month before. But workers are not feeling a raise: with inflation running warm, real hourly earnings have been slipping, so paychecks are growing in dollars while losing ground to prices.

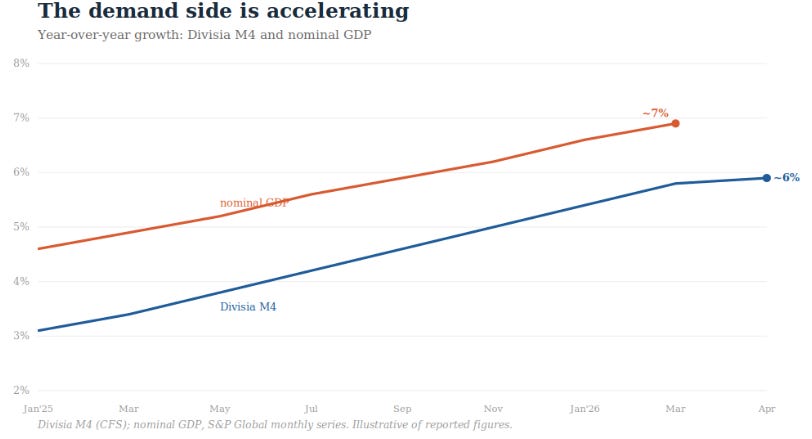

And there is a demand-side signal the payroll figures don’t capture. Inflation has been drifting up, and while part of that is supply shocks, part of it looks like money.

Divisia M4 has been on a clear upward trend — from around 3 percent in early 2025 to near 6 percent this April. Nominal GDP growth is climbing alongside it, approaching 7 percent in March on S&P Global’s monthly series.

Seven percent nominal GDP growth is not the arithmetic of 2 percent inflation. With real growth running around 2 percent, it is the arithmetic of something closer to 5 — an economy being pushed, not merely holding steady. A frozen labor market and accelerating nominal spending are an uncomfortable pair.

For the Federal Reserve, that pair is the real puzzle. The labor market’s apparent calm gives a cautious central bank cover to wait, and the cooling wage figure offers an excuse to pull if it wants to ease.

But the monetary aggregates point the other way. Money and nominal GDP accelerating while inflation drifts up is not the profile of an economy that needs a rate cut.

It is the profile of one that indicates the Fed may already be running too loose — watching the labor market for permission to ease while the demand side quietly argues it should be doing the opposite.

So what does the month actually tell us, in the proper perspective?

Not that the economy is accelerating — the gains are too narrow for that. Not that it is cracking — the upward revisions and the three-month run rule that out.

What it describes is something in between, and more peculiar: a labor market that has frozen in place. Hiring is steady but concentrated. Unemployment is low mostly because layoffs are rare. And the cost of that stillness falls on whoever happens to be on the wrong side of it — the unemployed who can no longer find the door back in.

Frozen is not the same as failing. But it is not health, either. It is an economy holding its breath — and one month, however strong its headline, is not enough to tell you when it will exhale.

A marker for the calendar: the June report lands July 2, and a large benchmark revision is in the pipeline. Even the ground we are standing on is still being redrawn.

The flight to liquidity is propelling the economy. As TDs fall relative to DDs, AD rises.