Commodity Prices, the Fed´s worst enemy

Commodity Prices, the Fed´s worst enemy

and the Fed is wont to fall into the "commodity trap"

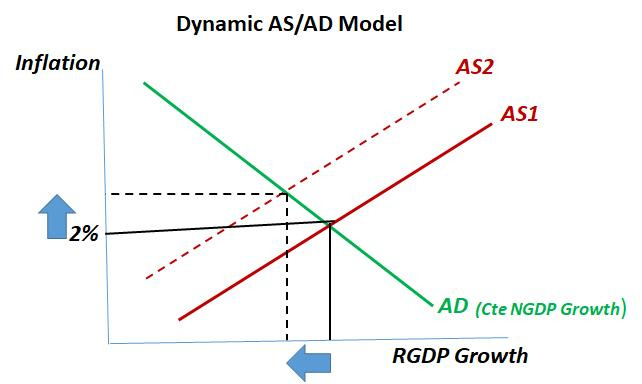

Commodity price shocks, or supply shocks more generally, puts an inflation targeting Central Bank in a bind. The chart below illustrates. When there is a supply shock, the Aggregate Supply (AS) curve shifts up and to the left. Given the growth rate of Aggregate Demand (NGDP), there is a rise in inflation and a fall in real output (RGDP) growth. [The only observation I need to make is that the AD curve was drawn as a straight line for simplicity. It must be interpreted as a “Rectangular Hyperbola”, in which case every point on the curve gives the same AD (or NGDP) growth, say, 5%].

What to do? If the Fed is “radical” about its target, it will tighten monetary policy (contract NGDP growth). That will restrain the rise in inflation, but will enhance the fall in growth (and increase unemployment). If the Fed tries to offset the fall in growth, it will enhance the effect on inflation.

Bottom line, in cases of supply shocks, the best option for the Fed is to keep NGDP growth stable. In other words, the Fed should not try to “offset” a supply shock with a demand shock.

That said, it must be kept in mind that inflation, unlike many think or use for analysis, is NOT a price, or oil, or commodities, or rent, or used car phenomenon. Others believe inflation derives from STRUCTURAL changes, such as globalization or demographics.

None of the above. Inflation (the sustained increase in the overall price level) is a MONETARY phenomenon. Individual, or group, prices will be changing relative to one another all the time. Structural changes will also bring about changes in prices relative to one another. That´s called RELATIVE PRICE change, which is the way a well functioning market economy allocates resources efficiently.

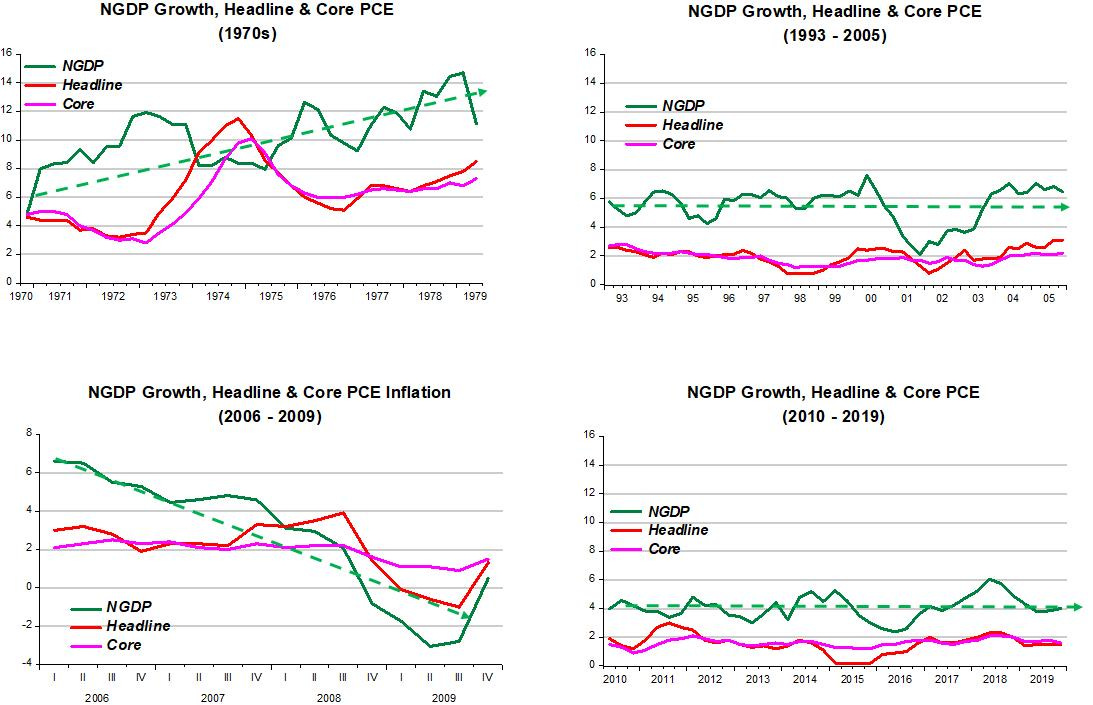

The charts below provide robust evidence that inflation (or disinflation) is a monetary phenomenon. Using Friedman´s “Thermostat Analogy” (see here), an expansionary monetary policy is one where NGDP growth is on a rising trend. A contractionary monetary policy is reflected in a falling NGDP growth trend. A stable monetary policy is one where NGDP is on a stable growth path.

The 1970s clearly show that monetary policy was expansionary. The outcome is rising inflation (both of the headline & Core varieties). Between 2006 and 2009, monetary policy was strongly contractionary so that, despite the Fed´s “promise” of 2% inflation, we observe disinflation. During most of the 1990s and first half of the 2000s, and again during the 2010s, monetary policy was stable, so inflation was also stable.

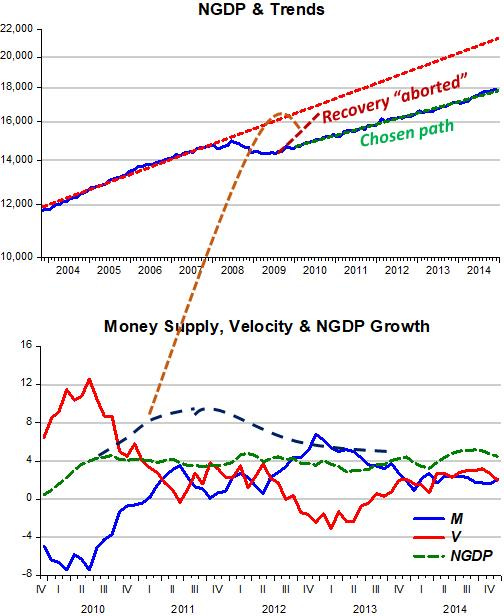

The next charts clearly show that my contention earlier on that if the Fed tried to “offset” a negative price (or supply) shock with contractionary monetary policy, real growth would be heavily penalized. In this instance the monetary contraction was so strong that the result was the “Great Recession”, with real growth turning strongly negative and inflation even falling well below target!

There´s no doubt, therefore, that the “Great Recession” was “Fed made”. Trying to put the blame on house prices (that´s supposed to have given rise to the “Financial Crisis”) is just shifting blame to make the Fed “look good”.

Did the Fed learn anything from that experience? Bernanke himself did not have to learn anything. The problem was that he had forgotten what he knew! Here´s what Bernanke knew long before becoming Fed chairman:

Bernanke (with Gertler & Watson) 1997 (on oil shocks)

Substantively, our results suggest that an important part of the effect of oil price shocks on the economy results not from the change in oil prices, per se, but from the resulting tightening of monetary policy. This finding may help to explain the apparently large effects of oil price changes found by Hamilton and many others.

It appears he continued to “forget”. When in late 2009, both nominal and real growth were just breaching the “zero line”, another oil/commodity shock ensued. This time, instead of contracting monetary policy, risking throwing the economy in a deep depression, the Fed chose to stop the monetary expansion, quickly settling the economy on a lower than before level path and lower nominal growth rate.

As the bottom chart indicates, it should have allowed monetary expansion (NGDP growth trend) go on for longer to get back somewhere closer to the previous level NGDP path. Thereafter it would reduce the rate of monetary expansion to allow NGDP to grow at a rate closer to the pre GR rate (the red dotted line).

In 2012, musing about the “anemic” recovery, Bernanke said:

As background for our monetary policy decision making, we at the Federal Reserve have spent a good deal of effort attempting to understand the reasons why the economic recovery has not been stronger. Studies of previous financial crises provide one helpful place to start. This literature has found that severe financial crises--particularly those associated with housing booms and busts--have often been associated with many years of subsequent weak performance. While this result allows for many interpretations, one possibility is that financial crises, or the deep recessions that typically accompany them, may reduce an economy's potential growth rate, at least for a time.

The word “cover-up” came to my mind. One of the “many interpretations”, maybe the most important, is that, as the charts above indicate, monetary policy was still “too tight”!

The Fed has “covered-up” before.

An interesting story is told by Athanasios Orphanides. In March 1937, just before the final leg of the increase in required reserves was implemented, Marriner Eccles, the Fed Chairman said:

Recovery is now under way, but if it were permitted to become a runaway boom it would be followed by another disastrous crash (referring to the GD).

Several months later, halfway through the recession, at the November 1937 meeting John Williams, a Harvard professor, member of the Fed board and its chief-economist said:

We all know how it developed. There was a feeling last spring that things were going pretty fast … we had about six months of incipient boom conditions with rapid rise of prices, price and wage spirals and forward buying and you will recall that last spring there were dangers of a run-away situation which would bring the recovery prematurely to a close. We all felt, as a result of that, that some recession was desirable … We have had continued ease of money all through the depression. We have never had a recovery like that. It follows from that that we can’t count upon a policy of monetary ease as a major corrective. … In response to an inquiry by Mr. Davis as to how the increase in reserve requirements has been in the picture, Mr. Williams stated that it was not the cause but rather the occasion for the change. … It is a coincidence in time. … If action is taken now it will be rationalized that, in the event of recovery, the action was what was needed and the System was the cause of the downturn. It makes a bad record and confused thinking. I am convinced that the thing is primarily non-monetary and I would like to see it through on that ground.

And Tim Geithner in October 08 (pg 144), just as the economy was plunging:

The argument that makes me most uncomfortable here around the table today is the suggestion several of you have made—I’m not sure you meant it this way—which is that the actions by this Committee contributed to the erosion of confidence—a deeply unfair suggestion.

… But please be very careful, certainly outside this room, about adding to the perception that the actions by this body were a substantial contributor to the erosion in confidence.

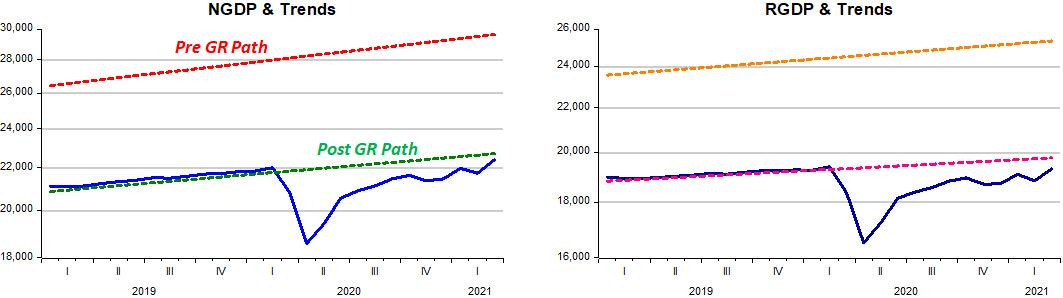

Things are very different now. The Covid19 recession was not, as the name indicates, Fed-made. The Fed, therefore had nothing to “cover-up”, so acted forcefully, having already placed the economy (as I write) back on the level nominal and real paths it was on before the Covid19 shock.

Recovery, placing the economy on the level path it was on before the shock, is, therefore, (almost) complete. Will the Fed follow up on Powell´s “teachings” that we have to do better?

For that, the Fed will have to “calibrate” monetary policy (the “thermostat”) to allow a rising trend in NGDP growth until it places NGDP at the desired level (somewhere between the post and pre GR level path).

That´s not a trivial job. First, we don´t know how a rising trend for NGDP growth is divided up between inflation and RGDP growth. Second, we face, at present, another commodity price shock.

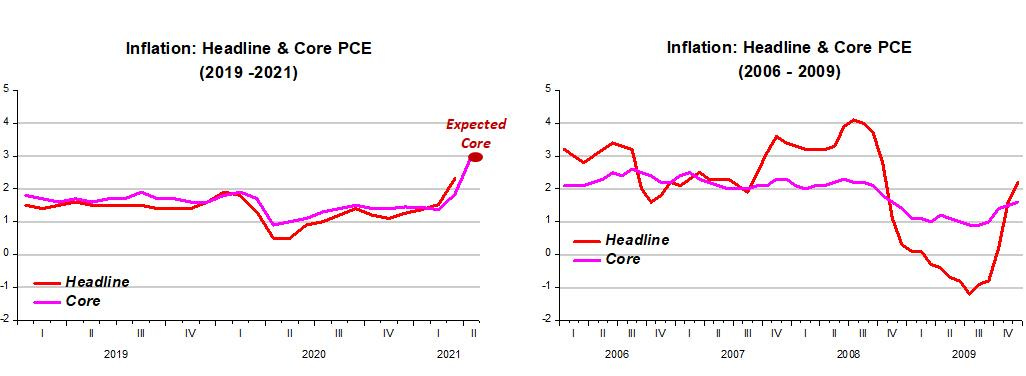

The chart below compares the behavior of inflation (also during a commodity price shock) going into the GR with the behavior of inflation now (commodity prices have risen almost 70% YoY in April).

In the recent period, inflation has been more subdued than before. Also, differently from then, the Fed is less “uptight” about the 2% “hard target”, having adopted the Average Inflation Target (AIT) framework last August.

AIT, however, still requires the Fed to communicate about make-up policy regarding inflation, something the public has a hard time understanding after almost four decades of “inflation bashing” by the Fed.

For example, recently Powell said that “allowing” inflation to temporarily rise above 2% doesn´t mean allowing it to go as high as 6%! What about 5.5%? Certainly not a smart thing to say.

I´ve been critical of AIT, but now we´re stuck with it and it will certainly make the Fed´s communication harder to comprehend.

Since Covid19 was both a supply and demand shock, the Fed will have to to be patient to get nominal spending to the desired level. The quicker it tries to reach it, the more important will be the supply constraints that exist in stocking inflation.

If it can gear the public´s expectations to a more gradual increase in nominal aggregate demand, the better planned adjustment of supply will alleviate price pressures. That´s an indication that having a NGDP Level Target framework is better than some form of inflation targeting.

The next few months will certainly be interesting to observe.

Bernanke drained legal reserves for 29 contiguous months, turning asset prices upside down or underwater. Then the lag in short-term money flows hit in the last half of 2008.

The problem with Bernanke et. al., is that there is no fool in the shower. Monetary lags are mathematical constants. Because Volcker didn't know that he created two back-to-back recessions.