An inflation chart-book

An inflation chart-book

Where it´s coming from and where it´s going

(Note: The “Chart-book” name was borrowed from Adam Tooze´s “Chartbook Newsletter”)

The recent takes on inflation have reminded me of this 1975 top 10 song (You´ve blown it up sky high).

Two very recent takes have “blown me”.

Art Laffer (of Laffer Curve fame) says:

'While Reagan healed the sick, Biden has infected the healthy. While Reagan cured inflation, Biden is creating inflation,'

And Desmond Lachman of the AEI writes:

The predicament in which the Fed finds itself would seem to be very much of its own making. Never before has the Fed engaged in as rapid a bond-buying spree as it did under Jerome Powell’s leadership. Indeed, whereas it took six years for Ben Bernanke’s Fed to increase the size of its balance sheet by $ 4 ½ trillion, it took the Powell Fed less than a year to do the same thing in 2020.

There´s nothing interesting or useful in Laffer´s piece, apart from this tweet comment I received:

Replying to @NGDP_Advice and @Claudia_Sahm

Art Laffer needs to remember the tens of thousands of people who died of AIDS because of Reagan .

Lachman doesn´t realize that his argument in the quote above is the reason why outcomes differed so wildly between JP´s Fed and BB´s Fed!

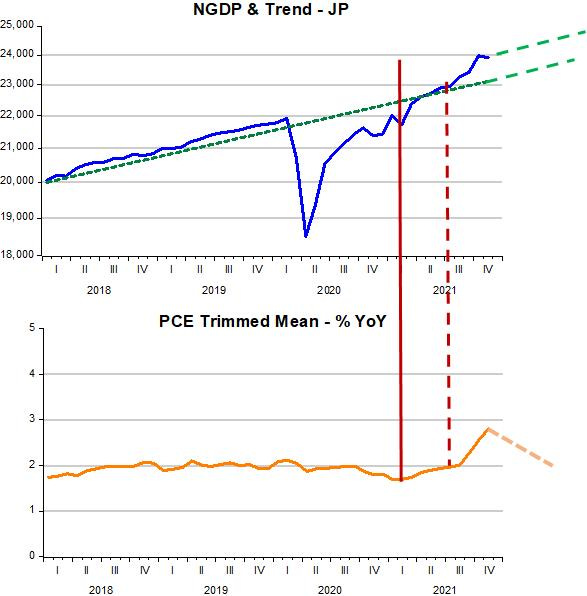

The panel below illustrates with a chart that I´ll explore in more detail later.

In the next chart, I use the increase in the Trimmed Mean PCE as the proxy for “Covid19-free” (or “super core”) inflation. Why will become clear soon.

The period between the solid and dotted bars show the time when NGDP made its final sprint to the trend path from 2010 and remained there. More recently, NGDP “took-off” again, and it was only then that Covid19-free prices rose above target.

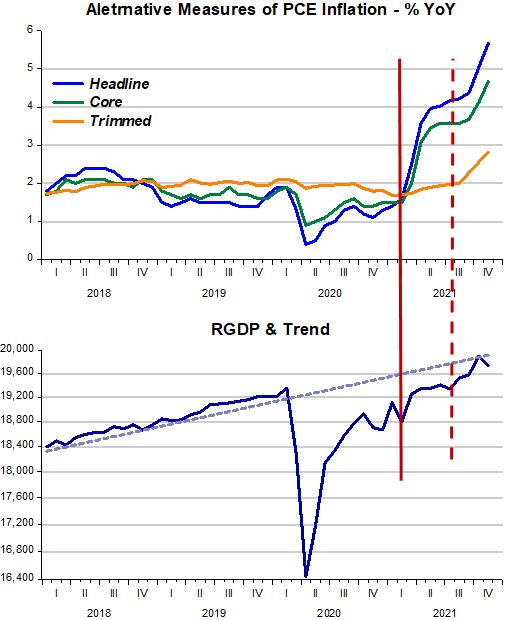

The next chart “confirms” that the NGDP sprint to trend hit supply-side constraints. RGDP flattens out quickly, resulting in an increase in Covid19-Related prices (Headline & Core measures of PCE). As NGDP stays on the trend path, those price increases flatten out, but as soon as NGDP “takes-off”, going above the trend path, both Covid19-free and Covid19-related prices climb. This final leg reflects “true inflation”, when ALL prices rise and is due to expansionary monetary policy.

During the final NGDP increase, RGDP was taken to the trend path (in other words, a full recovery). The supply constraints (or bottlenecks) pressured ALL prices, with inflation increasing.

We know (at least I do) that inflation cannot persistently rise if monetary policy obtains Nominal Stability (a stable aggregate nominal spending (NGDP)) growth. If the Fed is successful in keeping NGDP rising at the post GR trend rate (~4%) from this point on, the likely outcome is that Covi19-free price inflation will turn down to the 2% target. Covid19-related inflation will initially flatten out and then fall as Covid19-related supply constraints and bottlenecks wane.

However, if the Fed decides to seriously pursue its new AIT target (something it has not done in more than 10 years, and when it did in 2008, with Headline inflation rising to 4% in the wake of oil shocks, a deep recession ensued), it will try to force NGDP back to the post 2010 trend level path.

This implies that NGDP growth will be negative for a period, risking bringing about a recession, with inflation dropping below 2% and unemployment rising. Is that the sort of price we´re willing to pay for the sake of an “average”?

Interestingly, in 2009 Ben Bernanke´s Fed was not willing to take NGDP back to the then trend level path (which had been in place since 1987) afraid of the transitory effects on inflation (that would likely increase during the period of adjustment). The result was that inflation (both the Core and Trimmed PCE) remained far below target (averaging 1.5%) during the remaining years of his tenure.

One takeaway is that it makes no sense to compare the present “state of inflation” to the late 1970s, post-war years, or any other. And I have not mentioned “fiscal policy” because it is not pertinent to the “inflation question”.

So we don’t like NGDPLT anymore? Sounds like the preferred policy is “NDGPLT - but we change the level if it turns out we missed our target, but only if we missed to the upside”. Gonna need a longer acronym.

Unexpected inflation (or deflation) is zero-sum but it creates unanticipated winners and losers. By allowing a permanent deviation from the targeted level you simply make these gains & losses permanent. This strikes me as highly politically destabilizing over time. (For example, many of the 35% who don’t own homes in the US are likely permanently priced out now if we follow your policy).