An Illustrative Panel

An Illustrative Panel

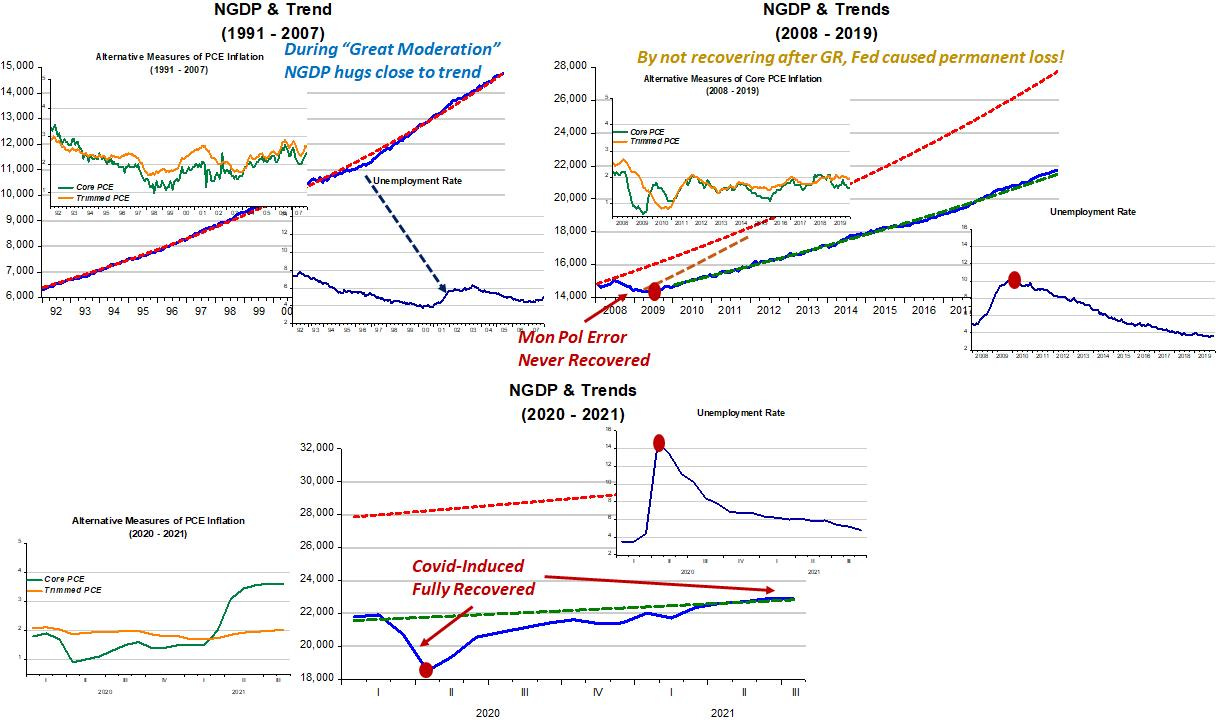

Thirty-year story of nominal output, inflation & unemployment

We are being “overburdened” by the “inflation talk”. Two examples from today:

Ryan Avent writes “Disco Inferno”:

in considering whether we are entering a new and potentially stagflationary era, it’s not enough to point to this or that parallel and say because those things are the same the outcomes are the same.

Claudia Sahm writes “Inflation is not the emergency”:

Inflation is important. Prices at the pump are high which is hurts. The cost of many things like cars, electronics, and home appliances are up too, if you can find them.

But, inflation is not an emergency.

I don´t want to burden readers with several hundred (or more) words. I´ve always believed in the power of images to help us humans who are naturally “pattern-seeking, story-telling animals” to get a grasp of processes.

To help you navigate the panel below, The “main actor” is the trend level path of NGDP (aggregate nominal spending, or AD). If NGDP evolves close to the path, NGDP growth is stable and that fact gives out several “goodies”, in particular a falling/stable rate of inflation and a falling/low rate of unemployment.

During the “Great Moderation” (the period/era from the mid-1980s up to the Great Recession) NGDP growth was quite stable (stayed close to the trend path). Some instability happened, not strong enough to affect inflation but leading to undesirable oscillations in unemployment.

The Great Recession was, from the standpoint of NGDP stability, a gross monetary policy error, and one that persisted because monetary policy never tried to lead the economy back to the Great Moderation trend path, content with putting the economy on a much lower trend path, along which it also kept NGDP stable. Initially employment shoots up and falls relatively slowly because no effort was made to put NGDP back on the original level path. Inflation also initially falls and remains stable once NGDP stability is regained.

Contrast that with what happened during the pandemic. Initially, NGDP takes a dive (this time not due to Fed error), but monetary policy reasonably quickly brings NGDP up and has by now managed to place it back on the trend path it was on post GR. With NGDP reacting quickly, the unemployment rate falls much faster than it did following the GR. And note, the (contained) rise in inflation is not a generalized phenomenon. For example, the Trimmed Mean PCE shows no significant change because it “trims” those prices related to "supply bottlenecks”.

Going forward, 3 things are key:

How the Fed behaves (better it keeps NGDP “hugging” the trend

How quickly the pandemic gets “resolved”, and

How quickly “bottlenecks shrink” (at least somewhat dependent on control of pandemic)