A monetary policy whodonit

A monetary policy whodonit

"Did the Fed bring inflation down? If so, how?"

This “whodonit mystery” started off earlier this month when David Beckworth did a podcast with Ricardo Reis of the LSE. The last segment is:

Ricardo´s View of the Phillips Curve

Reis: David, let me start by saying that I'm the Phillips professor at the LSE, so I have to defend the Phillips curve.

I can never say it's obsolete otherwise I would fall on the floor since my chair would become obsolete. So it's definitely present. But with that account, let me make three observations. The first one is that, the way I understand monetary policy is, whereby tightening monetary policy, a central bank is able to bring inflation down. In the same way that when I go to the doctor with an infection with a bacteria of some kind, antibiotics are the way to kill the bacteria and cure me from that. However, a side effect, and I emphasize, let me say it slowly, a side effect of raising interest rates is that you also cause a recession. You also lead to an increase in unemployment. In the same way that a side effect of taking antibiotics is that they tend to wreak havoc with your gastrointestinal, digestive system.

Note that it is not a channel. It's not by taking antibiotics and screwing up my intestines that I therefore kill the bacteria. No, no, it’s a side effect. Likewise, raising interest rates lowers inflation and has a side effect of unemployment, but it may not lower unemployment the same way that you may go through a course of antibiotics and be perfectly fine with your gastrointestinal system. So the fact that unemployment has not gone up, does not in any way discredit the way in which monetary policy works, does not pose a puzzle of any kind, because an increase in unemployment following a tightening of monetary policy is not something that has to happen for inflation to fall. It's something that often happens as a side effect.

Olivier Blanchard took issue with that view. In a Twitter thread he concludes:

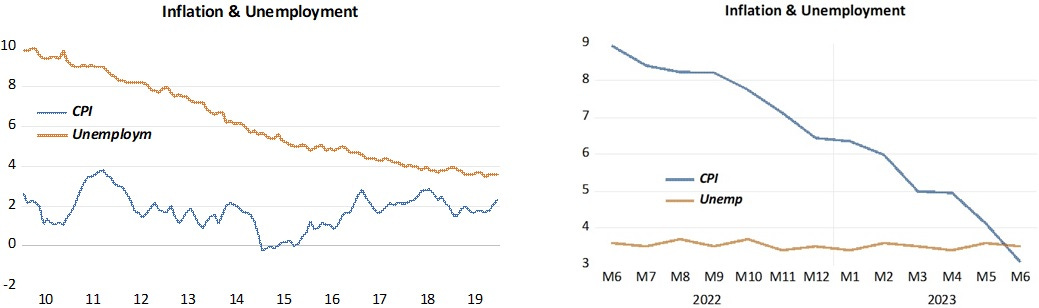

How do you square Blanchard´s “causal” relation with the facts observed in the two pictures below, where in the first unemployment falls a lot and inflation does not budge while in the second inflation falls a lot and unemployment stays low and “quiet”?

There are several other instances over the past several decades where Blanchard´s assertion fails badly:

In 1973 -1974, both unemployment & inflation RISE

In 1977 - 1979, while unemployment FALLS, inflation RISES

In 1980 - 1982, unemployment RISES while inflation FALLS (the “causal” mechanism in action)

In 1982 - 1986, both unemployment & inflation FALL

It is for this reason that Ricardo Reis says:

…as an empirical relation that says that you have a correlation between inflation and employment, or even as a causal relation, that it's through raising unemployment, they lower inflation, is a deeply flawed empirical as well as theoretical claim, precisely because it is a side effect. And when that happens sometimes, but not always, precisely because it's not the causal mechanism, it very often happens that you have inflation going up and down with unemployment not going up and down in that way. That is why when you look at a correlation between inflation and employment, you end up with relatively low values.

Enter Paul Krugman with Jerome Powell, Mind Controller?

Some economists giving the Fed credit for lower inflation have been making a different argument, which I think of as “contactless” monetary policy — the claim that monetary tightening can directly reduce inflation, without having to cause unemployment along the way. For example, Ricardo Reis of the London School of Economics argues that while inflation-reducing rate hikes may sometimes lead to higher unemployment, “that is a side effect, not the causal channel.”

I’m with Blanchard here.

I really don´t know why the Phillips Curve still lives! Maybe it is because, as Ricardo Reis concludes, the PC concept provides a useful “warning signal”:

…But the Phillips curve has a very important trade off as what you can do, is why you have to be careful in controlling inflation, that is absolutely essential for any central bank.

I find that a very weak argument. Maybe he says so just because, as he states, he holds the “Phillips Chair at the LSE”!

So, whodunit?

In short, the Fed and some supply shocks.

The last eighteen months provide the evidence. Keep in mind that a negative supply shock prevails when inflation rises and real output growth falls. A negative demand shock prevails when both inflation and real output growth fall. A positive supply shock prevails when inflation falls and real output growth rise.

Also keep in mind that the stance of monetary policy is given by what is happening to NGDP growth. If it is falling, as it has done for the past 18 months, this means that monetary policy is tightening (or becoming less expansionary).

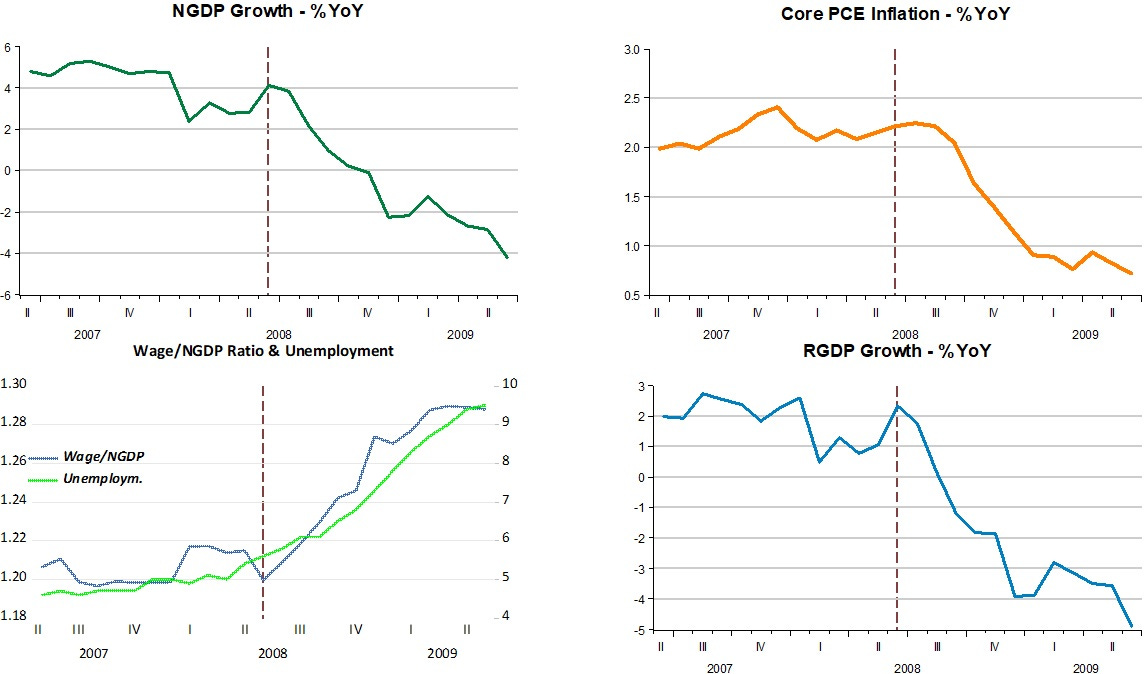

The panel below illustrates. Disregard, for the moment, the bottom right chart that plots the unemployment rate and the wage/ngdp ratio. I´ll talk about it later.

In the first “interval”, the economy experienced the “war shock”, a negative supply shock, where inflation rises and real growth falls. The fact that at the time monetary policy was becoming less expansionary, this likely enhanced the fall in output growth and contained the rise in inflation.

During the second interval, both inflation and output growth fall. This drop in inflation is due to the Fed´s action restricting aggregate demand (NGDP) growth. The large drop in oil prices, that dropped from more than U$ 110 to less than U$ 80, is mostly due to the fall in demand, since real output growth fell along with inflation.

The last interval depicts a positive supply shock, with inflation falling and real growth rising. The fact that monetary policy was tightening is reflected in the continuing fall in NGDP growth. This certainly “helped” with inflation and contained real growth.

Given that during this last interval oil prices barely moved, Krugman is wrong to downplay Fed action to restrain demand but gets it right when he writes in the article linked above that:

What remains is an argument between those who credit the Federal Reserve, which has certainly been trying to reduce inflation by rapidly increasing interest rates, and those who attribute disinflation to Long Transitory — a term I think I coined. That is, they argue that inflation is falling because the economy is finally unsnarling the kinks created by the Covid-19 pandemic and its aftereffects.

To paraphrase Ricardo Reis, I´ll say that a rise in unemployment is a side-effect of bad monetary policy.

It is a generally accepted fact that (for several reasons) wages are sticky. Imagine a situation where unemployment is low and stable, inflation is low and stable and NGDP growth is stable. That´s the “perfect macroeconomic world”. Suddenly, for whatever reason, the Fed strongly tightens monetary policy (indicated by a strong fall in NGDP growth).

With wages sticky, the ratio of wages to NGDP shoots up. With that, unemployment will also shoots up (after all, there will be less spending to “afford” wage payments).

This sort of bad monetary policy is behind the “Great Recession”. The charts illustrate. With core inflation stable and close to target, the Fed, worried about rising oil prices, stepped hard on the monetary brake, sending aggregate nominal spending (NGDP) growth into negative territory very quickly. The result was a steep rise in the wage/NGDP ratio and the ballooning of unemployment.

Contrary to what happened going into the “Great Recession”, monetary policy is now “good”, in the sense that it is correcting for previous mistakes. NGDP growth is falling towards the “desired” ~4.5% rate. Unemployment is also falling and stabilizing because the wage/NGDP ratio is also falling and stabilizing, as observed in the bottom RHS of the second set of charts above.

A “soft landing” in the present case will happen if the Fed successfully brings NGDP growth to ~4.5%. If all goes well. the Fed should get there in the next few months. If that happens, the wage/ngdp ratio will stabilize and unemployment will continue to be low and stable, while inflation will converge to target. If supply “unsnarling” continues, real output growth will also stabilize at a higher rate.

In short a “perfect macroeconomic world”is a distinct possibility!

Marcus, what do you think about the most recent Atlanta Fed GDPNow estimates forecasting 5%+ RGDP growth in Q3? If that were to happen, wouldn't that make the ~ 4.5% target impossible for the next couple of quarters?