It is important to understand the "nature of the beast"

It is important to understand the "nature of the beast"

I think Olivier Blanchard is "down in the weeds and can´t see the forest"

Very recently, Olivier Blanchard did a podcast with Soumaya Keynes in the FT entitled “Are we in for a hard landing?”, where he shows, like several others, that he is mostly worried about the “weeds”, thus missing the “beautiful forest” that sprouts all around!

His main points:

I was right in predicting inflation, but I was wrong about the channel. I thought it would happen through the labour market. It happened through commodity markets. But once you put this back in and, you know, when we analysed the ‘70s, we had it in, then there is nothing terribly surprising.

The point about expectations is more about how the price shocks tend to last or not. So in the ‘70s there were price shocks very similar to the ones we had, mostly energy or food and . . . but it happened. And then people said, well, we’re going to have inflation forever. And they started asking for wage increases and so on. So it lasted much more. This time, we didn’t get that because the inflation expectations have been anchored.

Team transitory said, you know, we have these price shocks but expectations are anchored. So they are going to come and go and there is no need to do anything. I thought they were wrong at the time, but they were basically right. The only issue is that shocks kept coming quarter or month after month for the best of three years, so it was not transitory or temporary.

Team permanent, which was Larry [Summers] and me and Jason Furman, I think, and surely other people said, look, you have crazy fiscal policy, which we had and there’s no question. Now where I went wrong, I think Larry might disagree, was that I thought unemployment would go down a lot, so much that there would be enormous wage pressure and the wage pressure would create the inflation. And that did not happen. So I think we were both wrong.

Let me describe I think what happened and why it’s not the full answer, which is, on the way up, inflation was nearly entirely due to the relative price of oil, the relative price of energy, relative price of food, supply chain disruptions. And on the way down, same thing. Just this thing is reversed.

Now, when I describe it this way, it sounds like demand had nothing to do with it. But in fact, you know, why did commodity prices go up? Well, there is Ukraine, but leave Ukraine aside. It happened later. My sense is what happened is that US fiscal policy had an effect on world demand for commodities. So part of the increase in prices clearly came from demand. How much came from Covid shock, supply chain disruptions? How much came from strong fiscal policy or weak or loose monetary policy? I think this hasn’t been established and that remains to be done.

I understood that what had gone up could go down just as easily as it went up. And that’s indeed what happened. And that had nothing to do with the labour market. It’s just that when in the end the energy price goes down, then, you know, inflation comes down.

Now the issue is that behind the scene, the labour market was not irrelevant. The labour market was putting pressure on wages, right. It became tighter. And in nearly all countries, the labour market is tighter today than it was in 2019. So there was some pressure on wages and then there was some response to inflation expectations.

So what happened as the shocks went away and inflation went down, we were left with the unseen part of the iceberg, which is the wage growth, which was too high as a result of the history of the previous three years.

That’s what we have now. So I would say until now, the decline in inflation had nothing to do with monetary policy. The up, didn’t have much to do with monetary policy either. The fact that it was transient had to do with the stability of expectations and the credibility, but with no particular measure being taken at the time.

Now, basically, we got the easy part. And we have in a number of countries wage growth, which is too high to achieve the 2 per cent that central banks dream about. And so, monetary policy may have to be used if the central bank wants to go to 2 and there is no good break, then it implies using monetary policy to slow down the machine.

His tentative conclusion (since when unemployment between 4% and 4.5% is “high unemployment”?)

I would say my best guess is that we probably need a bit higher unemployment to get to 2. But the Fed is not in a hurry to get to 2. It wants to send the signal, but it doesn’t want to do it next quarter. And we could get good breaks. So I still think the probability is that we have to have a high unemployment. I don’t want to give a number, but I’ll give a number — say, between 4 and 4.5 for some time. But maybe we can avoid it altogether. Not sure, but it’s not impossible.

What Blanchard mostly does is “reason from a price change” or, equivalently, thinks inflation is a “price phenomenon”. To him, the most important price, the one that ultimately determines inflation, is wages [“So what happened is that as the shocks went away and inflation went down, we were left with the unseen part of the iceberg, which is the wage growth”]. But he´s willing to concede that oil and commodities in general played a role this time around.

He emphatically claims that monetary policy played no role: “I would say until now, the decline in inflation had nothing to do with monetary policy. The up, didn’t have much to do with monetary policy either”.

But, to get inflation down the last few yards to 2% he says: “monetary policy may(!) have to be used if the central bank wants to go to 2 and there is no good break, then it implies using monetary policy to slow down the machine”.

This sounds funny. Monetary policy is needed to (marginally) bring down inflation when there are no “good breaks”. but rising inflation is mostly due to “bad breaks”, and most of the fall in inflation is due to “good breaks”. Where “good” and “bad” breaks are related to falling or rising prices of a bunch of things!

To show that Blanchard is equivocated in focusing on “weeds”, some preliminaries are necessary.

Just as many think that inflation is a price phenomenon, they also think monetary policy is an interest rate phenomenon. That´s also “reasoning from a price change”, where the “price” here is called interest rate.

Many, however, believe that “inflation is a monetary phenomenon”. When they do, it´s mostly related to money supply, with money demand (or its inverse, velocity) rarely mentioned. That´s likely because the common assumption is that velocity is stable. (However, as Friedman reminded us more than 50 years ago, “velocity can be whatever people want”).

The equation of exchange in growth form is written: m+v=p+y, where p+y=NGDP. Looking at the equation of echange from the perspective of a thermostat, m (money growth) is the amount of “coal in the furnace”, closely controlled by the central bank (fed), v (velocity growth) is the “outside temperature” and NGDP the “inside, or room, temperature”.

Just as a mechanical thermostat works to keep the “room temperature” stable by offseting changes in the ouside temperature, the monetary policy “thermostat” involves the Fed “dialing” m up or down to offest changes in v so as to keep NGDP growth stable.

From that perspective, “appropriate” monetary policy can be described as the “actions” taken by the Fed (moving m) to keep NGDP growth stable”. So, if monetary policy is expansionary, NGDP growth will be rising. If monetary policy is contractionary (or tightening), NGDP growth will be falling. NGDP growth, therefore, is the best indicator of the stance of monetary policy

One implication is that if monetary policy is “adequate” (NGDP growth stable), inflation will most likely (absent concurrent supply shocks) also be stable. As we will see, the level of the stable inflation rate is closely tied to the level of the stable NGDP growth rate.

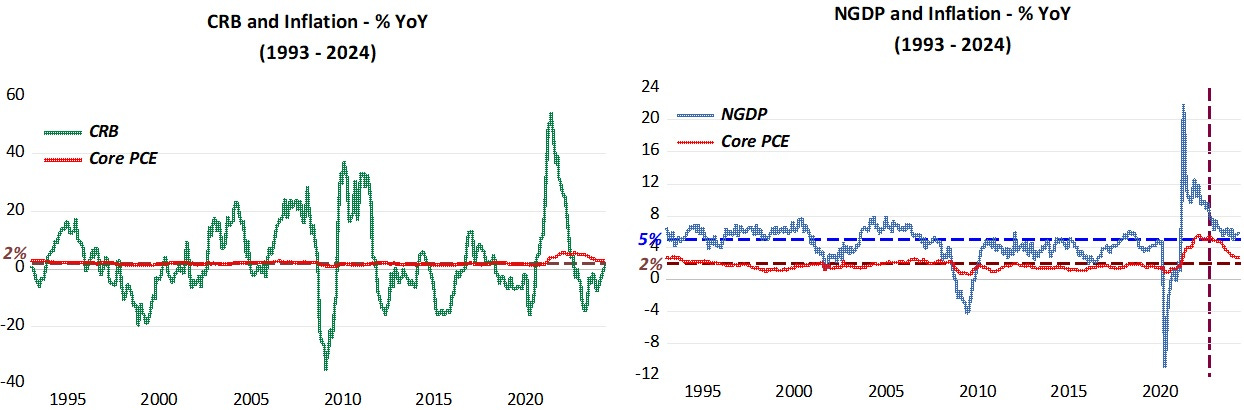

With these preliminaries, we can show that it is not “bad/good breaks” (commodity prices, for example) that give rise to inflation (or desinflation/deflation), but deviations of NGDP growth from its stable rate.

The charts below illustrate. While commodity prices fluctuate widely, inflation remains quite stable. It appears it is deviations of NGDP growth from the stable level that give rise to deviations in inflation from the “target” rate.

Note:

After the GR, NGDP growth was stable at a rate lower than before. Inflation was also stable at a rate lower than “target” (2%).

At the end of the sample we see a strong, but relatively brief, rise in commodity prices. Blanchard et al ascribe the resulting inflation to that “very bad break”. We observe, however, that the real culprit was the highly expansionary monetary policy reflected in the massive increase in NGDP growth. With NGDP growth coming down more clearly towards its historic stable rate, inflation also turns down towards “target”.

Contrary to what Blanchard thinks, it appears monetary policy was behind both the rise and fall of inflation! “Bad & Good breaks” were no more than “supporting actors” in this “series”.

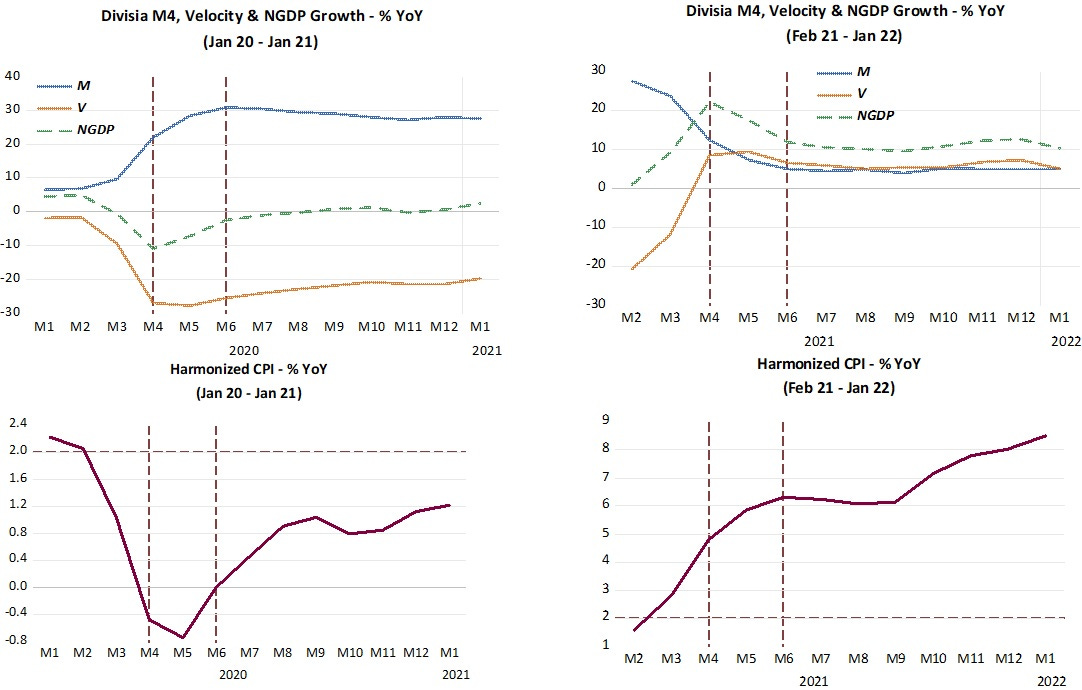

This becomes clear when we watch the “series” “episode by episode”. The first two “episodes” are illustrated below. The first (LHS charts) show the moment C-19 hit and the Fed´s reaction. The second “episode” shows “the route to inflation”.

[Note: The inflation measure I use is the Harmonized CPI. It is a headline (includes food & energy) index, essentially differing from the conventional CPI by excluding the OER component. This is useful because OER is a price no one pays, an inputed number and, to top the distortions it brings about, is a lagging indicator]

C-19 was a surprise that led to a “deep & quick” drop in velocity (the “outside temperature” fell a lot in a short time). Quite unlikely that any thermostat could offset that change “immediately”, so NGDP growth (the “inside temperature”) reacted with a lag. As soon as the “inside temperature” begins to “warm up”, by the Fed pursuing an “appropriate” monetary policy (that required a strong increase in the money supply growth), NGDP growth improves and inflation stops falling and begins to move toward “target”.

To the right of the dotted verical line, NGDP growth stabilizes close to 0% “degrees”. Inflation, however, continues to rise. This was most likely due, not to “bad breaks” but (in the words of Blanchard in a different context), to the “stability (anchoring) of expectations and credibility”.

This sounds reasonable because inflation was still far below “target”.

The “second episode” in the “series” begins with the Fed, by not offsetting the rise in the “outside temperature (v), allowing the “room temperature” (NGDP growth) to increase significantly.

In short order, v stops rising while m continues to fall, reducing NGDP growth. Shortly thereafter, monetary policy stabilizes NGDP growth at a high rate. Inflation is also stabilized at a high rate for a time. Then, “bad breaks” hit (remember the Russian build-up for war with the consequent impact on commodity prices) and inflation begins to rise.

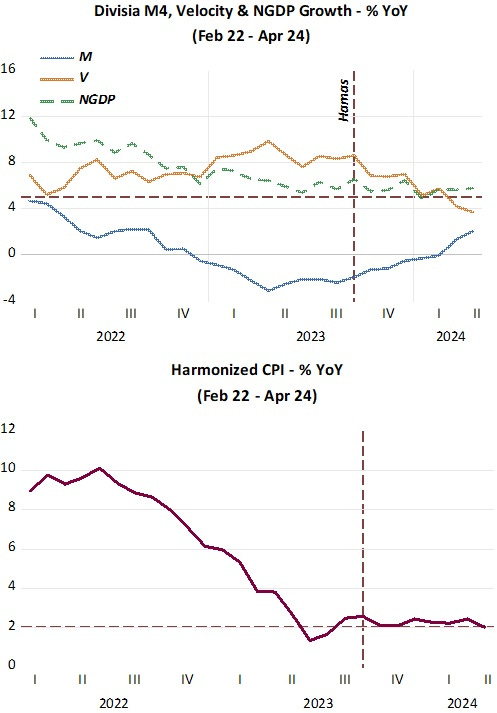

The third and last “episode” in the “series” is illustrated below.

In early 2022, monetary policy becomes more restrictive, so NGDP growth begins to fall. Not long after, having “absorbed” the “bad breaks” of previous months, inflation begins to fall. “Good breaks” (fall in commodity prices, for example) certainly helped, but the “main actor” was still the Fed´s monetary policy.

The Hamas terrorist attack in early October 2023 (and the expected geopolitical events that would follow) decreased the “outside temperature”, v. The accompanying rise in m at that point avoided an “undesired” fall in NGDP growth, which remains relatively stable at a rate not much above the “historical” 5% rate.

Since then, the HCPI measure of inflation has remained stable and very close to “target”.

So it´s terribly worrying to read Blanchards take that “monetary policy may have to be used if the central bank wants to go to 2 and there is no good break, then it implies using monetary policy to slow down the machine”.

Is he implying that monetary policy has to tighten (in his mind an increase in interest rates) if there are no “good brakes”?

That would be a terrible mistake. I just hope that the Fed is not in denial about the power of monetary policy (even though it expresses a lack of “confidence”).

Only price increases generated by demand, irrespective of changes in supply, provide evidence of monetary inflation. There must be an increase in aggregate monetary purchasing power, AD, which can come about only as a consequence of an increase in the volume and/or transactions' velocity of money.

The odd thing is that Blanchard explains very well the origin of the shocks that correctly led the Fed to crank up inflation (or NGDP growth if that's what you think it is, or should be, targeting). And when the relative price adjustments were made, to crank inflation/NGDP growth back down. [As a matter of fact, I think it did not start cranking down soon enough and so has had to crank down from higher and for longer than it otherwise would have needed to.] But then he comes out with the bizarre idea that the entire episode of over-target inflation/NGDP just happened -- popped into existence like a quantum fluctuation from the vacuum state -- immaculately untouched by the Fed instrument settings. But that to further reduce inflation from almost at target to target WILL require active tightening?

Now going forward, is it necessary to leave the EFFR (a synecdoche for the vector of monetary policy instruments the Fed might use) "higher for longer" to get PCE inflation down to 2% as Blachard thinks.? If so, is it because real wages have overshot their full employment equilibrium (which could be the implication of labor market tightness measurements, except that is not what they show)? It is hard to see why for the reasons Marcus Nunes points out here (and has been consistently pointing out!). In addition, TIPS expectations are marginally under target.

Could be that Blanchard shares the Fed’s view that once it begins to reduce the EFFR, it must continue, that reversing course (and then re-reversing if necessary) is inconceivable?