A simple illustrated story of the US economy so far in the 2020s

A simple illustrated story of the US economy so far in the 2020s

No DSGE modeling here

I don´t put much credence in the “conventional analysis” as, for example, that in Bernanke & Blanchard.

In June 2023, Bernanke & Blanchard wrote: “What caused the US pandemic-era inflation?”. In the abstract, we read:

We find that, contrary to early concerns that inflation would be spurred by overheated labor markets, most of the inflation surge that began in 2021 was the result of shocks to prices given wages. These shocks included sharp increases in commodity prices, reflecting strong aggregate demand, and sectoral price spikes, resulting from changes in the level and sectoral composition of demand together with constraints on sectoral supply. However, although tight labor markets have thus far not been the primary driver of inflation, we find that the effects of overheated labor markets on nominal wage growth and inflation are more persistent than the effects of product-market shocks. Controlling inflation will thus ultimately require achieving a better balance between labor demand and labor supply.

(Where better balance between labor demand and labor supply is euphemism for higher unemployment!)

DSGE “operators” should skip the rest of this post! Because, as is implicit in B&B:

The DSGE model is a model in which output is determined in the labour market as in New Classical models and in which aggregate demand plays only a very secondary role, even in the short run.

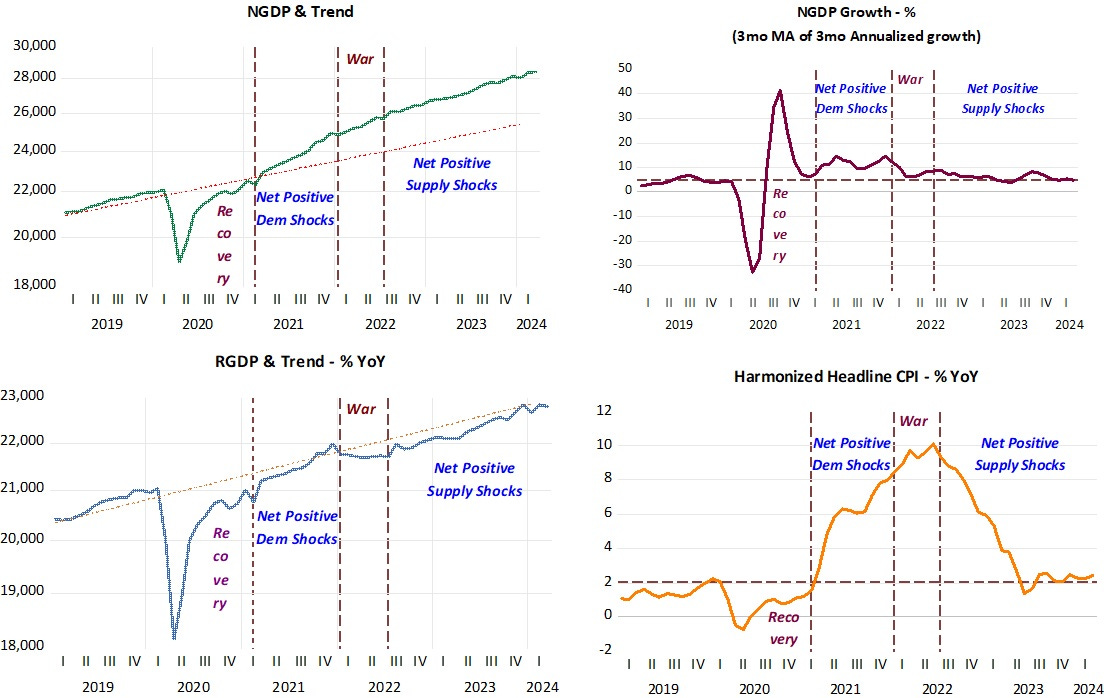

The story is illustrated in 5 (interconnected) charts.

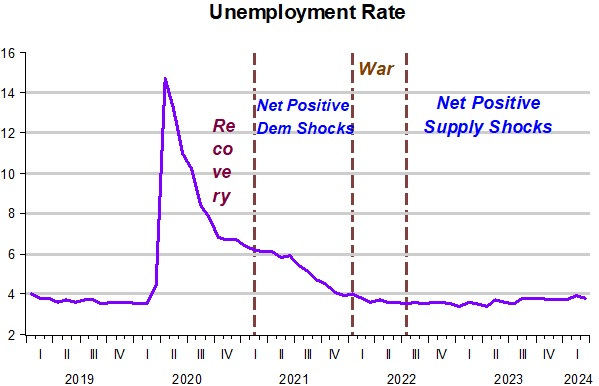

First (unlabeled) was the recession, deep and short. This was followed by a quick and strong receovery. By January 2021, the recovery was “complete”, with NGDP back on the post Great Recession trend path. Note that RGDP fell short of the trendline. This was due to the “supply constraints” resulting from C-19. Inflation had “recovered” back to target and unemployment had fallen from more than 14%! to 6%.

From that moment, inflation begins (“unexpectedly”, because few predicted it) to rise. According to B&B: “most of the inflation surge that began in 2021 was the result of shocks to prices given wages.” In other words, according to B&B inflation was due to a variety of supply shocks.

That´s very unlikely. If true, you would observe rising inflation going hand in hand with falling output. Clearly, that is not what happens, because real output rises and reaches the post GR trend path!

The Fed was the culprit for the rise in inflation with monetary policy becoming expansionary as observed by the rise in aggregate nominal spending (NGDP). That likely happened because the Fed turned its attention to the labor market (while unemployment had fallen drastically, it seemed to be “hesitating” in falling more).

In February 2021, Powell gave a “we are the champions-type speech”: Getting back to a strong labor market. At the next FOMC Meeting, in March, we read:

The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.

He got more than he “wished” because monetary policy was excessively expansionary, with inflation more than “moderately” exceeding 2%! He was, however, quite successful in bringing unemployment below 4%!

During that period, therefore, the inflation experienced cannot be due (mostly) to supply shocks. It was the result of a positive net demand shock caused by the Fed focusing on the labor market.

Then, Russia invades the Ukraine. Inflation rises and output falls. This is the only moment in the history of the period that, contrary to conventional views, negative supply shocks are responsible for the increase in inflation.

That effect, however is short-lived. Despite monetary policy being more contained (see the drop in NGDP growth), inflation is on a falling trend and real output rises back to the post GR trend path. A very clear example of net positive supply shocks, mostly due to waning supply restrictions.

Understanding what has happened, and why, is important for the design of monetary policy going forward. Just as in early 2021 Powell was not “confident” that the labor market would continue to improve, now he is not “confident” that inflation will continue to come down to target.

Its worse, because inflation (excluding the “made-up” OER, not shelter, mind you) has been on target for some time, indicating that additional “restrictions” could have negative consequences. Just like in 2021 additional “incentives” gave rise to unwanted inflation!

PS The “contrarian view”:

"Policy is not restrictive," said David Zervos, Jefferies' chief market strategist, at the Atlanta Fed's Financial Markets Conference this morning. "Demand was not crushed."

"The main reason inflation did what it did had almost nothing to do with the demand cycle," Zervos said.

"The big picture story in this whole economic cycle was a massive supply shock following by the unwinding of that supply shock, and a little bit of aggregate demand tinkering," he said.

“Bitter thoughts” by Gov Waller, who for long has remained in denial! He certainly doesn´t look happy.

Inflation is the Ill-defined economic bogeyman. There is no such thing as the “wage-price spiral”; the “price-wage spiral”; or the “cost-push spiral”; in the sense that increases in wages, prices, or costs are causes of inflation.

Unless effective demands (money times transactions’ velocity) are adequate to prevent a cutback in sales, or a diversion of purchasing power to the price raisers, any administered increase in prices will result in less sales, smaller outputs, less employment, lower payrolls and less demand for products—in other words, depression and deflation in due course.

Convenient. Just the right data to support the narrative. It ironic. Inflation increases. The only way to contain it is to give smaller than inflation raises to the working stiffs. In other words to lower the living standard of the working class.